Nike (NKE) Valuation Check As Win Now Layoffs Target Profitability Reset

NIKE, Inc. Class B NKE | 0.00 |

Nike (NKE) is back in focus after announcing a second round of layoffs in 2026, cutting about 1,400 roles in technology and global operations as part of its ongoing Win Now turnaround plan.

At a share price of US$45.03, Nike’s 30-day share price return of 12.34% and year to date share price decline of 28.84% sit alongside a 1-year total shareholder return decline of 19.78%, which points to pressure that has been building rather than building momentum.

If you are weighing Nike’s reset and thinking about where else change could create opportunity, this is a useful moment to scan 18 top founder-led companies

With Nike shares at US$45.03 and recent returns under pressure, the key question is whether current weakness already reflects its challenges, or whether you are looking at an entry point before any future growth is recognized by the market.

Most Popular Narrative: 48.8% Undervalued

According to Unike, the most followed narrative sees Nike’s fair value at $87.90, almost double the last close of $45.03, which creates a clear valuation gap for investors to assess.

Mid-Term Growth (3 to 5 Years) • Emerging Market Expansion, Nike is increasing focus on India, Latin America, and Southeast Asia, where the middle class is growing. • Sustainability Initiatives, Eco-friendly materials and circular design programs can appeal to younger consumers. • Connected Fitness & Digital Innovation, Nike’s investments in apps, digital memberships, and tech-driven apparel could increase engagement.

Want to see what kind of revenue path, profit margins, and future earnings multiple are baked into that near double fair value? The tension between slower forecast revenue growth, higher expected earnings growth, and a richer profit margin profile sits at the heart of this narrative, along with a specific future valuation multiple that assumes Nike still commands premium pricing in the sector.

Result: Fair Value of $87.90 (UNDERVALUED)

However, this hinges on Nike defending share against rising rivals and managing cost pressures, either of which could quickly challenge that near double fair value case.

Another View: Market Multiple Sends A Different Signal

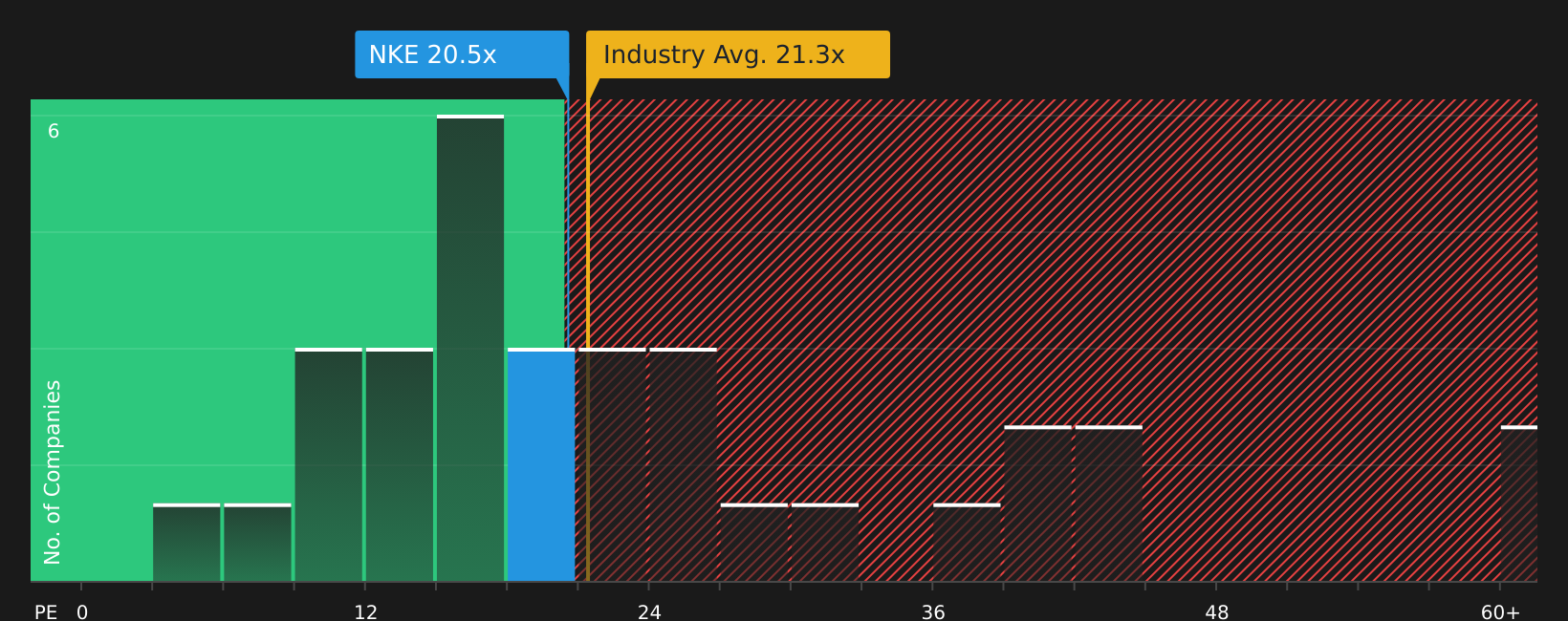

Unike’s fair value of $87.90 paints Nike as undervalued, but the current P/E of 29.6x sits well above the US Luxury industry average of 19.8x and only slightly below a fair ratio of 29.9x. That points to limited cushion at today’s price, so where does that leave the margin of safety?

Next Steps

With sentiment clearly split between opportunity and concern, this is the kind of setup where it can help to review the details yourself and decide quickly where you stand based on the 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If Nike’s story has you thinking about what else might be hiding in plain sight, now is the time to widen your search with a few focused stock ideas.

- Target resilience by reviewing companies with 72 resilient stocks with low risk scores that may suit investors who want to keep volatility in check.

- Spot value by scanning 53 high quality undervalued stocks that combine quality fundamentals with share prices that lag underlying business strength.

- Unearth tomorrow’s potential leaders by checking the screener containing 25 high quality undiscovered gems before the crowd pays attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.