Northern Trust (NTRS) Margin Decline Tests Bullish Views After FY 2025 Earnings

Northern Trust Corporation NTRS | 142.25 | +0.59% |

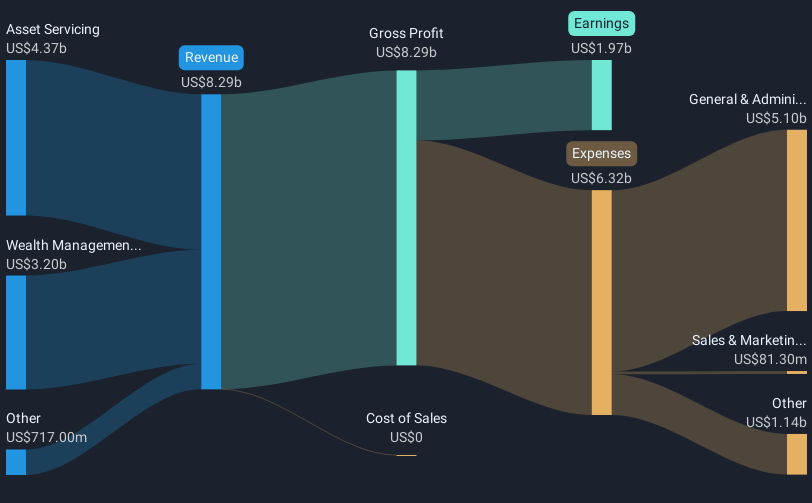

Northern Trust FY 2025 Earnings Snapshot

Northern Trust (NTRS) just wrapped up FY 2025 with fourth quarter total revenue of US$2,131.1 million and basic EPS of US$2.41, alongside net income excluding extra items of US$452.3 million. The company has seen quarterly revenue move from US$1,970.1 million in Q4 2024 to US$2,131.1 million in Q4 2025. Over that same period, basic EPS shifted from US$2.27 to US$2.41 on a quarterly basis and from US$9.80 to US$8.78 on a trailing twelve month basis, setting up a mixed picture for earnings power. With trailing net profit margin easing from 23.8% to 20.7%, the latest print leaves investors weighing headline growth in the top line against some pressure on profitability.

See our full analysis for Northern Trust.With the headline numbers on the table, the next step is to see how this earnings profile lines up with the widely followed narratives around Northern Trust's growth, income appeal, and margin resilience, and where the fresh data starts to challenge those views.

AUM Climbs Above US$1.7b Through 2025

- Across FY 2025, assets under management moved from US$1,610.4b at the start of Q1 to US$1,772.7b at the end of Q3, with quarterly net flows ranging from US$700m to US$11,600m.

- Bulls often point to sticky institutional and wealth clients as a strength, and the AUM path in 2025 supports that idea while also showing some noise:

- Net inflows of US$11,600m in Q1, US$700m in Q2 and US$5,500m in Q3 suggest clients kept adding money overall, even as flows slowed after Q1.

- Across the last twelve months of reported data, total revenue sat between US$7.9b and US$8.6b, which lines up with the view that fee based businesses can keep revenue relatively steady as long as AUM stays high.

Margins Ease To 20.7% As FY 2025 Progresses

- On a trailing basis, net profit margin moved from 23.8% a year earlier to 20.7%, while trailing net income excluding extra items went from US$1,972.4m at FY 2024 Q4 to US$1,679.2m at FY 2025 Q4.

- Bears often focus on pressure in fee businesses, and the margin shift gives that view some backing but not a one sided story:

- Trailing total revenue stayed in a relatively tight band, from US$7,857.6m in FY 2024 Q3 to US$8,577.1m at FY 2025 Q1 and US$8,093.9m at FY 2025 Q4, so the change in margin reflects profit moving more than revenue.

- Basic EPS on a trailing basis went from US$9.80 at FY 2024 Q4 to US$8.78 at FY 2025 Q4, which lines up with the idea of some earnings pressure even while the business continues to produce sizeable profits.

P/E Of 16.5x And 2.15% Yield Set The Trade Off

- At a share price of US$148.63, Northern Trust is on a 16.5x trailing P/E, below the US Capital Markets industry at 25.9x and peer average at 53.2x, while the DCF fair value of US$140.65 sits below the current price and the dividend yield stands at 2.15%.

- What stands out to many investors is the mix of modest growth with a relatively lower P/E and a regular payout:

- Earnings and revenue are each forecast to grow in the mid single digits per year, at about 4.8% and 3.7% respectively, which is slower than the broader US market forecasts but paired with trailing earnings described as high quality.

- The DCF fair value being under the market price, while the P/E is under market and industry levels, sets up a valuation picture where some metrics look conservative and others point to a more fully used price, leaving investors to decide which lens they trust more.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Northern Trust's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Explore Alternatives

Northern Trust's softer net profit margin, lower trailing EPS and a DCF fair value below the current share price highlight pressure on earnings quality and valuation support.

If that mix of earnings strain and a fully used price worries you, shift your focus to these 864 undervalued stocks based on cash flows to find companies where cash flow based value looks more compelling right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.