Northrop Grumman (NOC) EPS Beat And 10% Margin Reinforce Earnings Resilience Narrative

Northrop Grumman Corp. NOC | 702.50 | +0.79% |

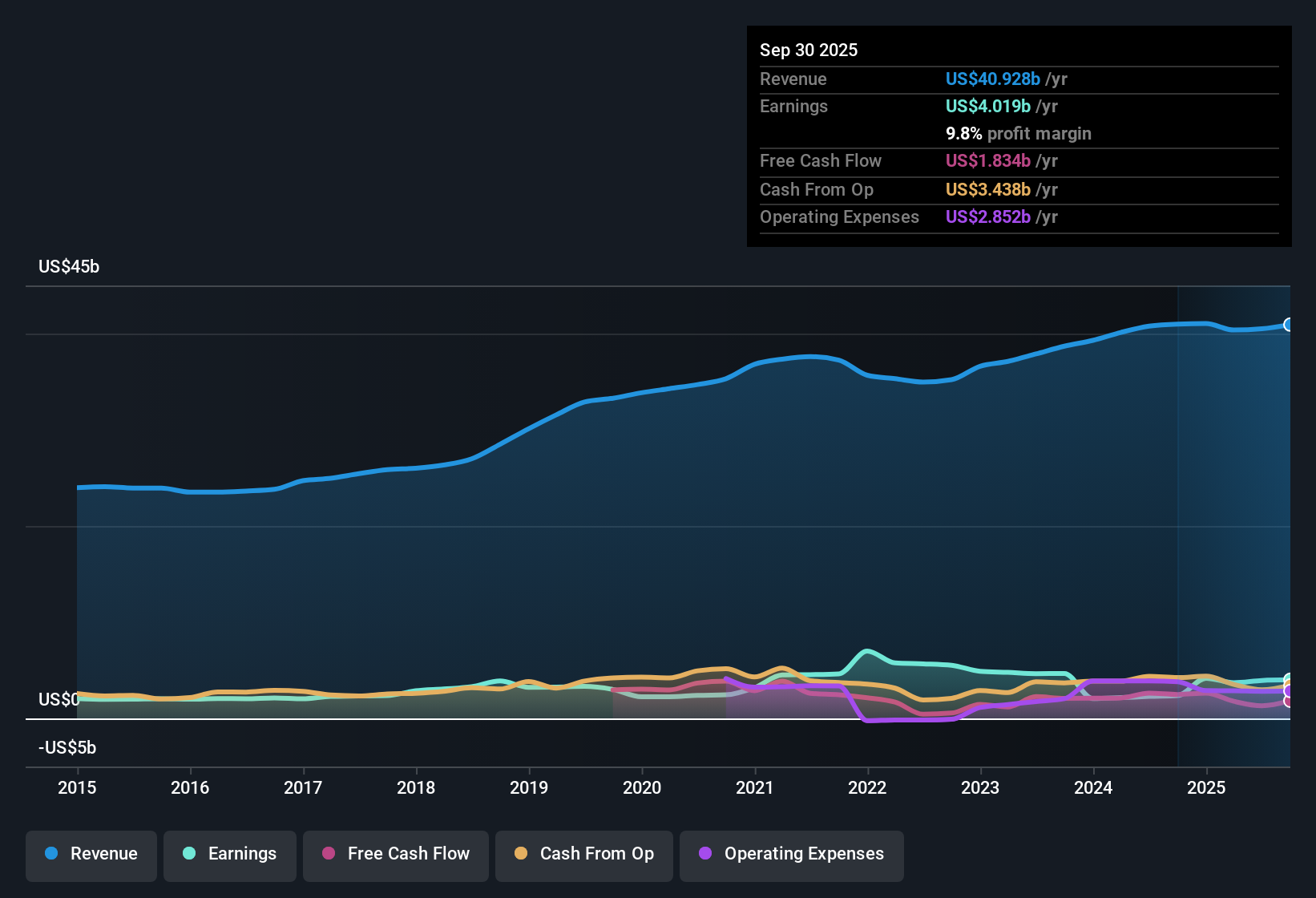

Northrop Grumman (NOC) closed FY 2025 with fourth quarter revenue of US$11.7b and basic EPS of US$9.99, alongside net income of US$1,427m, setting a clear marker for how the year wrapped up operationally. Over recent periods, quarterly revenue has ranged from US$9.5b to US$11.7b while EPS has moved between US$3.33 and US$9.99. This gives investors a solid run of data points to judge consistency and the latest step up in earnings power. With trailing twelve month EPS of US$29.14 and a net margin around 10%, the headline is that profitability held up, which frames the rest of the release around how durable those margins look.

See our full analysis for Northrop Grumman.With the numbers on the table, the next step is to set them against the most widely held narratives about Northrop Grumman to see which stories the latest results support and which ones they push back on.

TTM earnings barely edge higher at 0.2%

- Trailing twelve month earnings growth sits at 0.2%, compared with a five year average decline of 8.5% per year. This puts the latest US$4.2b of net income into context as a small move against a weaker longer trend.

- What stands out for the bullish view is that this slight uptick in earnings comes alongside a roughly 10% net margin and US$41.95b of trailing twelve month revenue. This supports the idea of a large, contract driven business, but also shows that recent growth has been modest rather than rapid.

- Bulls pointing to earnings resilience can reference the US$29.14 trailing EPS. However, the 0.2% growth rate keeps expectations grounded when compared with the much stronger figures that might be seen in faster growing sectors.

- Supporters who focus on long running defense programs may see the flat but positive earnings trend as a sign of stability. At the same time, the 8.5% average annual decline over five years reminds you that longer history has been less favorable than the latest twelve month snapshot.

10% net margin pairs with slower expected growth

- Net profit margin over the last year is about 10%, slightly below the prior year’s 10.2%. Analysts are expecting earnings growth of about 3.6% a year with revenue around 4.8% a year, which together point to steady but not rapid expansion on current forecasts.

- For a bullish take, the combination of a roughly 10% margin and modest forecast growth often supports the idea of a mature defense business with solid profitability. However, the relatively modest 3.6% earnings growth expectation and 4.8% revenue growth estimate limit how aggressive that optimism can be.

- Supporters might argue that keeping margins near 10% on roughly US$41.95b of trailing twelve month revenue is a positive, especially versus the earlier five year earnings decline of 8.5% a year.

- At the same time, the fact that both earnings and revenue growth forecasts sit below broader US market expectations means the bullish story leans more on stability and contract visibility than on high growth potential.

P/E discount offsets DCF fair value gap

- The trailing P/E multiple of 23.2x sits well below the Aerospace & Defense industry average of 42.2x and the peer average of 39.8x. The current share price of US$678.74 compares to a DCF fair value of about US$428.37, so the stock trades above that DCF estimate despite its lower P/E.

- Critics often point to valuation risk, and the US$678.74 price versus the US$428.37 DCF fair value backs that up. At the same time, the sizeable P/E discount to both sector and peer averages pulls the conversation in the other direction and makes the risk reward trade off more balanced than a simple premium or discount label would suggest.

- The P/E gap relative to the 42.2x industry level and 39.8x peers aligns with the idea that investors are not paying top tier multiples for the roughly 3.6% expected earnings growth and 10% margin profile.

- On the other hand, with the share price above the DCF fair value and a high level of debt cited as a risk, valuation focused bears have clear numbers to point to when they question how much safety is built into today’s price.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Northrop Grumman's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Northrop Grumman’s modest 0.2% TTM earnings growth, slower 3.6% forecast earnings growth, and premium to its DCF estimate all highlight valuation concerns despite stable margins.

If paying above a DCF fair value for modest growth makes you uneasy, use these 879 undervalued stocks based on cash flows to quickly focus on companies where pricing looks more compelling against their cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.