Northrop Grumman (NOC) Stock Could Be 25.2% Undervalued After Record Backlog Update

Northrop Grumman Corp. NOC | 0.00 |

Backlog, DARPA Project, and What They Mean for Northrop Grumman Stock

Northrop Grumman (NOC) is drawing attention after reporting a record backlog of US$95.61b and highlighting its role in DARPA’s Rads to Watts program, giving investors fresh context for the stock’s recent performance.

The backlog is tied in part to an expanded B-21 production agreement. It sits alongside full year 2026 guidance calling for sales between US$43.5b and US$44.0b and MTM adjusted EPS of US$27.40 to US$27.90.

At the same time, the company is working with Morgan State University and others on DARPA’s radiovoltaic Rads to Watts effort, which focuses on long duration, high density nuclear micro power systems for harsh environments.

Despite the record backlog and DARPA partnership, Northrop Grumman’s recent share price momentum has been weak, with the stock down 26.23% on a 90 day share price return basis. At the same time, the 1 year total shareholder return sits at 6.42%, which points to shorter term pressure alongside a still positive multi year outcome.

If this kind of defense and advanced energy work has your attention, it could be a good moment to look beyond a single contractor and review 89 nuclear energy infrastructure stocks

So with Northrop Grumman stock under pressure over the past quarter, but backed by a record US$95.61b backlog and DARPA-linked projects, should investors see a valuation gap here, or has the market already priced in future growth?

Most Popular Narrative: 25.2% Undervalued

Compared with the last close of $521.50, the most widely followed narrative for Northrop Grumman points to a fair value of $696.95, framing the recent pullback as a potential discount to modeled long term outcomes.

The ramp-up of advanced autonomous and integrated systems such as Beacon and IBCS, combined with ongoing investments in solid rocket motor capacity (targeting a near-doubling by 2029), positions the company to focus on high-growth, higher-margin market segments, which may affect future operating margins and underlying cash flow.

Want to see what sits behind that kind of confidence in future margins and cash flow, and how Northrop Grumman’s projected revenue path and earnings profile relate to a higher implied valuation multiple? The full narrative sets out the growth mix, profitability assumptions, and time horizon that underpin the $696.95 fair value and the view that today’s price reflects a sizeable discount.

Result: Fair Value of $696.95 (UNDERVALUED)

However, Northrop Grumman’s heavy reliance on large U.S. defense programs and rising capex toward about 4.5% of sales could challenge the underpriced narrative if budgets or costs shift.

Another View: Northrop Grumman Through a Cash Flow Lens

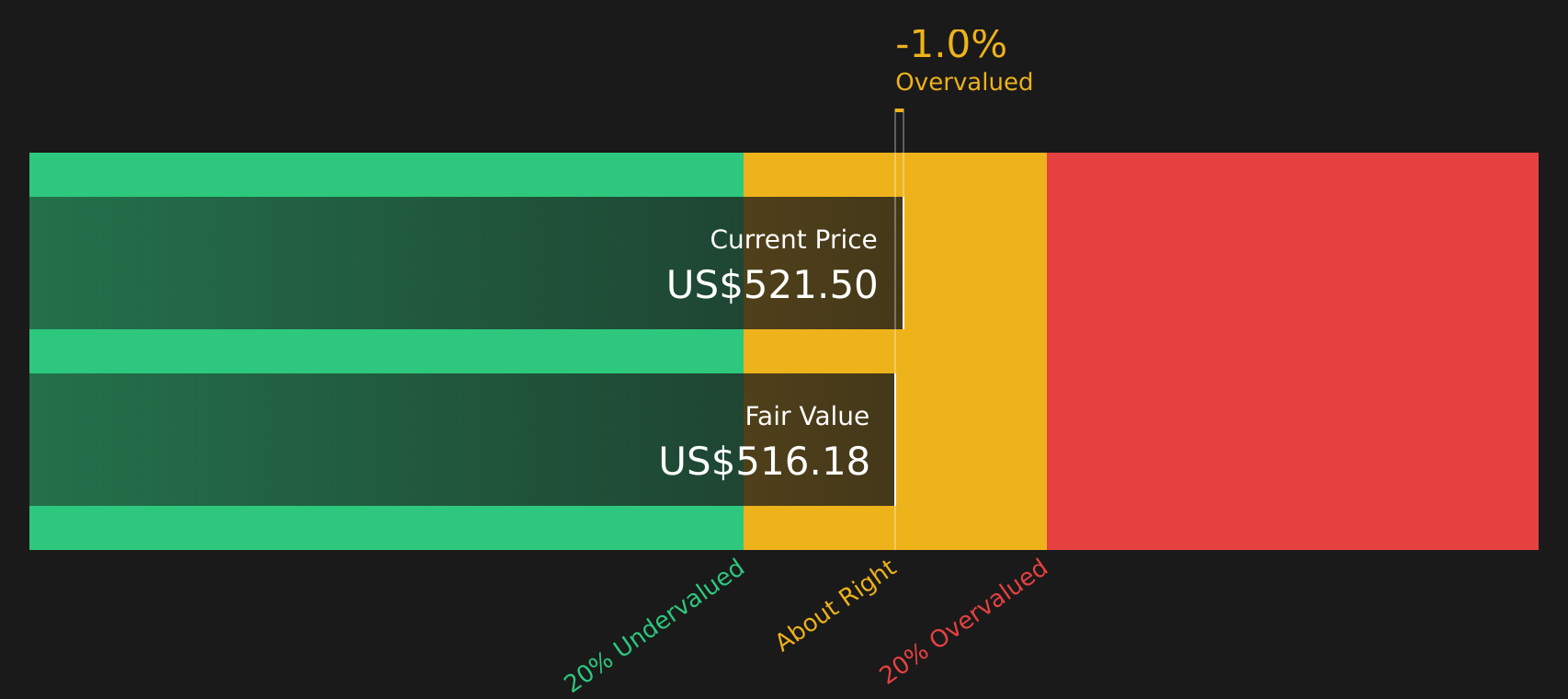

The first narrative around Northrop Grumman hinges on analyst targets and earnings multiples pointing to a fair value of $696.95. Our DCF model offers a cooler take, with an estimated future cash flow value of $516.18, slightly below the current $521.50 share price and implying limited upside from cash flows alone.

For readers who prefer to see how a cash based model stacks up against earnings multiples for the same stock, it is worth looking closely at the SWS DCF model and understanding the trade off between growth expectations and cash flow assumptions in the current price: Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Northrop Grumman for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around Northrop Grumman’s valuation and outlook, this is a good time to move quickly and ground your own assessment in the underlying data, including the 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Northrop Grumman?

If Northrop Grumman has sharpened your focus on quality, do not stop here. The right mix of stocks can reshape your portfolio faster than you expect.

- Target potential value opportunities by scanning 45 high quality undervalued stocks that combine strong fundamentals with prices that may not fully reflect their underlying business strength.

- Strengthen your income stream by reviewing 8 dividend fortresses that aim to pair higher yields with resilient business models and consistent shareholder returns.

- Reduce portfolio stress by focusing on 66 resilient stocks with low risk scores built around companies with steadier profiles that can help balance out more volatile positions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.