Northrop Grumman (NOC): Taking Stock of Valuation After a Strong Year-to-Date Share Price Run

Northrop Grumman Corp. NOC | 703.84 | +0.98% |

Northrop Grumman (NOC) has quietly kept investors interested this year, with the stock up about 21% year to date and roughly 23% over the past year, outpacing many defense peers.

At a share price of $568.46, Northrop Grumman has seen steady upward momentum this year, with a strong year to date share price return contributing to a robust one year total shareholder return as investors warm to its growth pipeline and perceived resilience.

If Northrop Grumman's run has caught your attention, it could be a good moment to explore other opportunities across aerospace and defense stocks and see which names are building similar momentum.

With shares near record highs, solid mid single digit earnings growth, and a healthy discount to analyst targets, investors face a key question: Is Northrop Grumman still undervalued or is future growth already fully priced in?

Most Popular Narrative Narrative: 14.2% Undervalued

With Northrop Grumman last closing at $568.46 against a narrative fair value near $663, the prevailing view leans toward meaningful upside if its long term thesis plays out.

The ramp up of advanced autonomous and integrated systems such as Beacon and IBCS, combined with ongoing investments in solid rocket motor capacity (targeting a near doubling by 2029), positions the company to capitalize on high growth, higher margin market segments, thereby enhancing future operating margins and underlying cash flow.

Curious how modest growth assumptions, steady margins, and a higher future earnings multiple combine to justify that premium fair value target? The full narrative unpacks the exact revenue runway, earnings trajectory, and valuation bridge that support this upside case, step by step.

Result: Fair Value of $662.68 (UNDERVALUED)

However, that upside depends on flawless execution, with any major setbacks on B 21 or Sentinel contracts, or shifting U S budget priorities, threatening the thesis.

Another View on Valuation

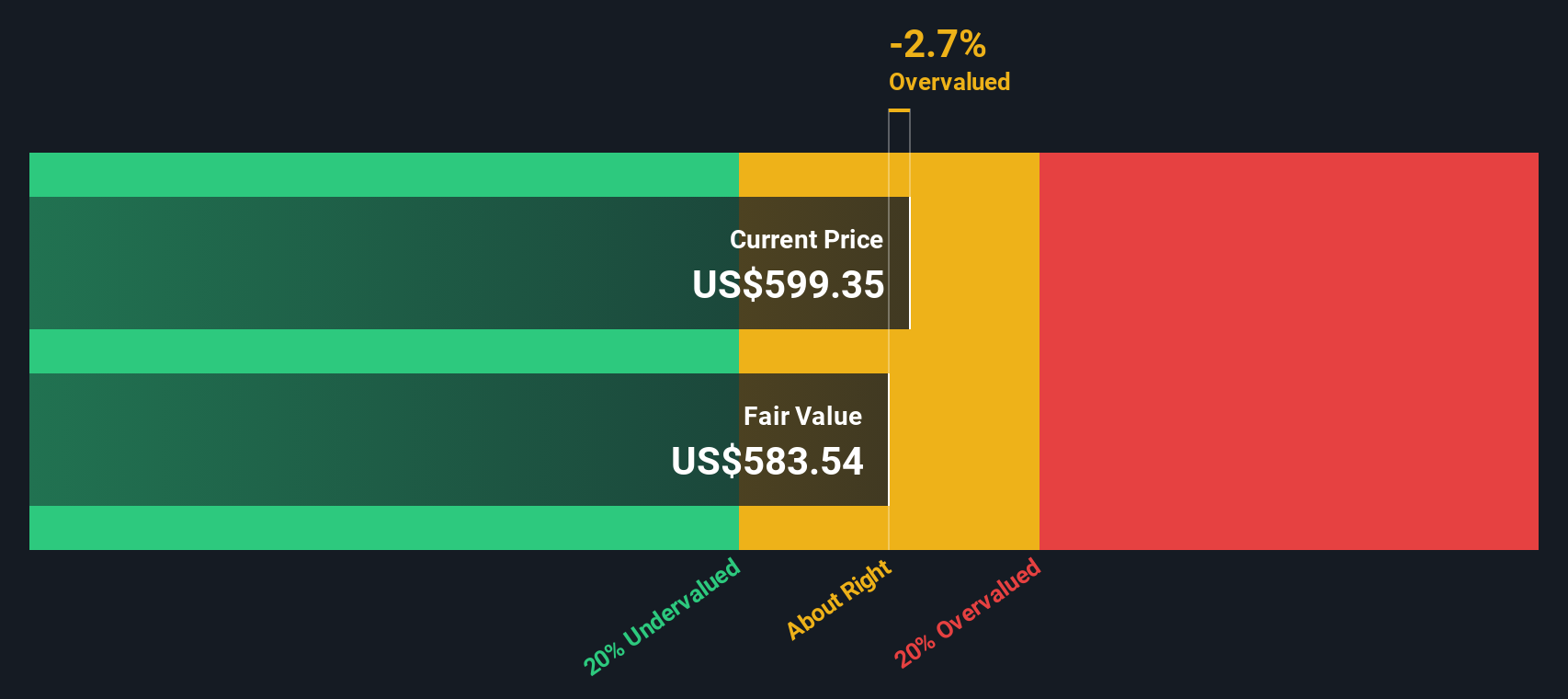

Our SWS DCF model presents a more cautious view, indicating that Northrop Grumman is trading above its estimated fair value of about $515 per share. This suggests the stock may be slightly overvalued rather than undervalued. Which perspective do you find more compelling: the narrative premium or the cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Northrop Grumman for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 914 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Northrop Grumman Narrative

If you are not fully aligned with this view or would rather dig into the numbers yourself, you can build a custom narrative in just a few minutes: Do it your way.

A great starting point for your Northrop Grumman research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more high conviction opportunities?

Before you move on, put Simply Wall Street to work finding your next edge. These tailored screeners can surface ideas you will not want to miss.

- Capture potential mispricings by scanning these 914 undervalued stocks based on cash flows that pair solid cash flows with attractive entry points.

- Position ahead of the next innovation wave by targeting these 25 AI penny stocks with compelling growth stories in artificial intelligence.

- Lock in dependable income streams by focusing on these 13 dividend stocks with yields > 3% backed by sustainable payouts and proven track records.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.