NovoCure (NVCR) Is Up 8.1% After TRIDENT Shows No Survival Gain From Earlier TTFields Start

NovoCure Ltd. NVCR | 0.00 |

- In June 2026, Novocure reported topline Phase 3 TRIDENT results showing that starting Tumor Treating Fields (TTFields) at the beginning of chemoradiation for newly diagnosed glioblastoma did not significantly improve overall survival versus starting during the maintenance phase.

- While the Early Start and Maintenance Start arms delivered similar survival outcomes, TTFields remained well-tolerated with no new safety signals, clarifying that timing rather than feasibility is the main question for integrating this therapy into standard GBM care.

- We’ll now examine how TRIDENT’s lack of added survival benefit from earlier TTFields initiation affects NovoCure’s broader investment narrative and future opportunities.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

NovoCure Investment Narrative Recap

To own NovoCure, you need to believe TTFields can still expand into new cancers and lines of therapy, turning today’s losses into a durable device-based oncology franchise. TRIDENT’s result looks more like a refinement than a reset: it narrows upside in earlier GBM use but leaves the core GBM franchise and the near term lung and pancreatic catalysts essentially intact, while reinforcing the key risk around heavy dependence on a single technology platform and ongoing trial success.

In this context, the February 2026 FDA approval of Optune Pax for locally advanced pancreatic cancer stands out. It provides NovoCure with a fresh commercial indication in a very hard to treat tumor type, supporting the near term growth story even as TRIDENT caps expectations for incremental GBM benefit from earlier use. How well Optune Pax is adopted and reimbursed will be central to offsetting any sentiment drag from the GBM timing setback and to testing the broader TTFields expansion thesis.

Yet beneath the appeal of multiple cancer indications, investors should be aware that the heavy reliance on TTFields technology means...

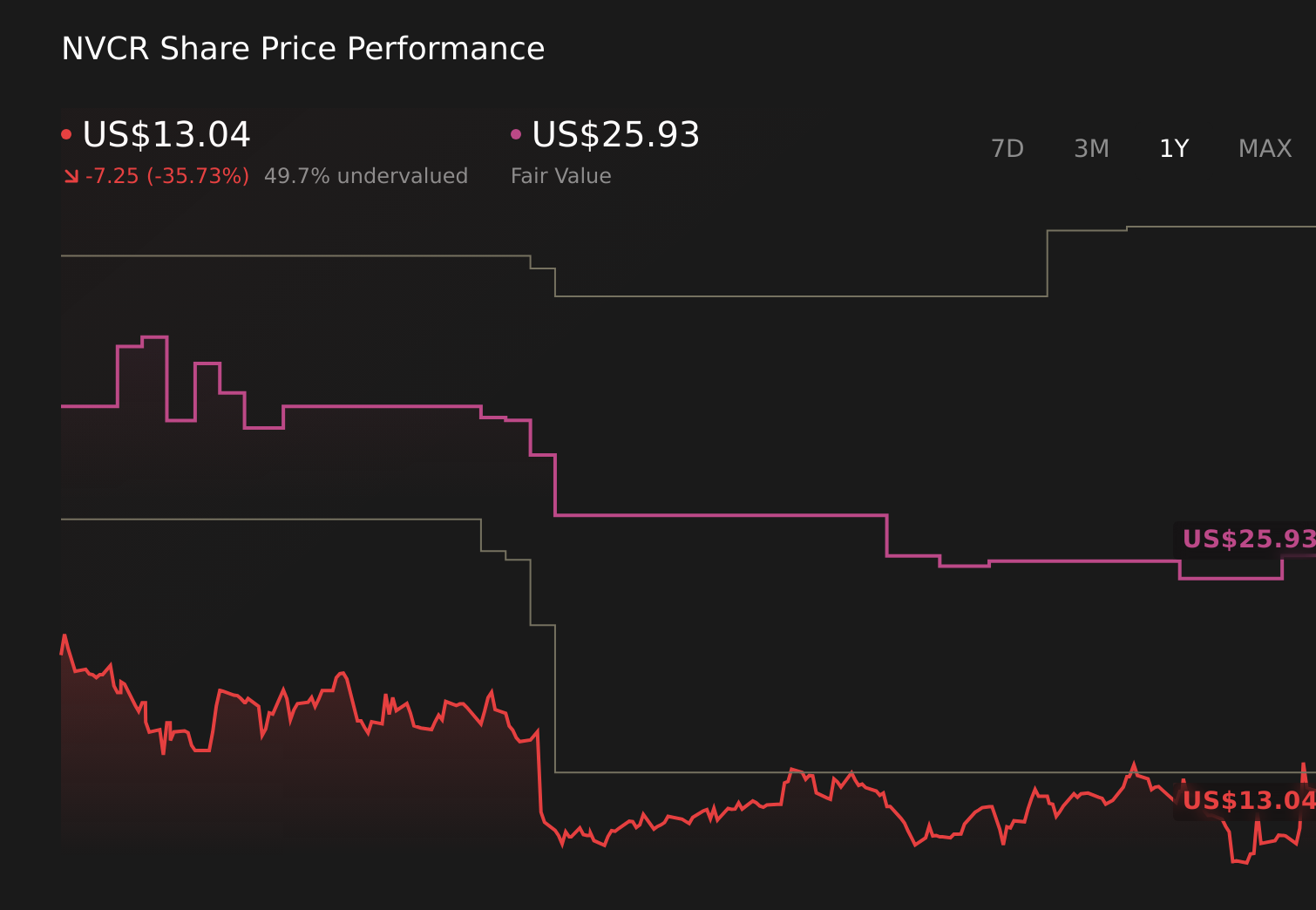

NovoCure's narrative projects $915.6 million revenue and $119.8 million earnings by 2029. This requires 11.8% yearly revenue growth and a $256.0 million earnings increase from -$136.2 million today.

Uncover how NovoCure's forecasts yield a $26.07 fair value, a 69% upside to its current price.

Exploring Other Perspectives

Before TRIDENT, the most bullish analysts were counting on about US$1.2 billion of revenue and a US$21.9 million profit by 2029, so if you worry about slow adoption and payer pushback you may see this GBM disappointment very differently from those who expect rapid TTFields uptake and faster reimbursement progress.

Explore 4 other fair value estimates on NovoCure - why the stock might be worth just $26.00!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your NovoCure research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free NovoCure research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NovoCure's overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.