NovoCure (NVCR) Stock Could Be 31.5% Undervalued After TRIDENT Trial Result

NovoCure Ltd. NVCR | 0.00 |

TRIDENT trial outcome and what it means for NovoCure stock

NovoCure (NVCR) shares are reacting to topline data from the Phase 3 TRIDENT trial, where starting Tumor Treating Fields therapy during chemoradiation did not improve overall survival versus starting in the maintenance phase.

For investors watching NovoCure stock, the result keeps attention on how the company uses these data to refine the clinical positioning of TTFields in glioblastoma while maintaining the reported safety and tolerability profile.

At a share price of $17.85, NovoCure has a 1-day share price return of 2.06%, a 7-day share price return of 7.21% and a 90-day share price return of 46.91%, while the 5-year total shareholder return is down 92.09%. This highlights recent momentum against a much weaker longer term record as investors weigh the TRIDENT outcome alongside ongoing trials and recent board changes.

If this kind of clinical news flow has your attention, it can be useful to see how other healthcare-focused AI companies are trading, so take a look at 40 healthcare AI stocks

With NovoCure stock up 36.1% year to date and the TRIDENT result removing one potential upside lever, a key question for investors is whether the recent rebound leaves the shares undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 31.5% Undervalued

At $17.85, the most followed NovoCure narrative pegs fair value at $26.07, suggesting the TRIDENT outcome sits alongside a much broader multi year thesis.

Validation of TTFields therapy in multiple new indications, such as pancreatic cancer (PANOVA-3) and brain metastases from non-small cell lung cancer (METIS), positions NovoCure for potential regulatory approvals and large market expansion beginning in 2026, likely driving topline revenue growth as global cancer incidence rises in the aging population.

Curious what underpins that fair value gap for NovoCure stock? The narrative leans on projected revenue traction, improving margins and a future earnings multiple that implies real confidence in execution.

Result: Fair Value of $26.07 (UNDERVALUED)

However, NovoCure stock still faces meaningful risks, including ongoing losses, with net income at a loss of US$173.0 million, and heavy reliance on TTFields remaining clinically and commercially relevant.

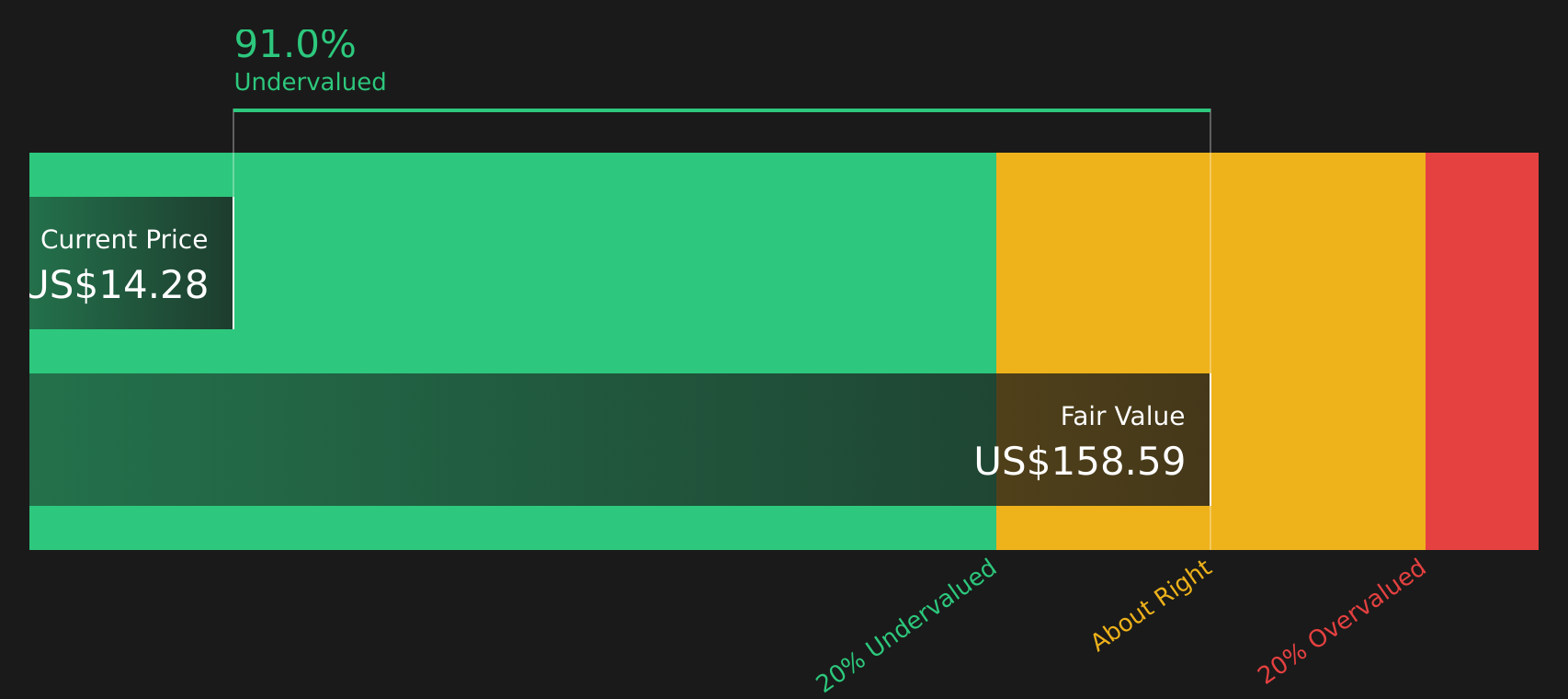

Another View on NovoCure stock valuation

The Simply Wall St DCF model paints a very different picture for NovoCure. At a share price of $17.85, the stock is described as trading 89.7% below an estimated future cash flow value of $172.49. This frames a much larger potential upside than the $26.07 fair value narrative.

That gap raises a key question for you as an investor: is the DCF being too generous about long term cash generation, or are shorter term narratives anchored too tightly to recent clinical and earnings headlines?

Next Steps

With sentiment clearly mixed after the TRIDENT result, now is a good time to review the data for NovoCure and decide where you stand, including the balance of 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond NovoCure stock?

If NovoCure has sharpened your focus on risk, reward and timing, do not stop here. Broaden your watchlist with other clear, data driven stock ideas today.

- Spot potential turnaround stories early by scanning 24 elite penny stocks with strong financials that pair small size with stronger fundamentals than many investors expect.

- Zero in on quality at a reasonable price by reviewing the 48 high quality undervalued stocks that combine solid finances with attractive valuations.

- Prioritize resilience and capital preservation by focusing on the 65 resilient stocks with low risk scores that stand out for steadier earnings and lower overall risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.