Nuvation Bio (NUVB): Valuation in Focus as Earnings Anticipation and Revenue Forecasts Drive Analyst Optimism

NUVATION BIO INC NUVB | 4.41 | -2.22% |

Investors are keeping a close watch on Nuvation Bio (NUVB) as the company prepares to announce its Q3 2025 earnings. Expectations have shifted upward, and higher revenue estimates for 2025 and 2026 are contributing to the recent buzz around the stock.

Anticipation ahead of Nuvation Bio’s earnings update and rising revenue forecasts have sparked fresh enthusiasm. The share price has climbed 125.97% over the last 90 days and the total shareholder return for the past year reached 126.96%. Momentum has accelerated notably in recent months, signaling renewed investor confidence amid improving growth expectations.

If this strong momentum has you wondering what else might be taking off, now’s a great time to explore See the full list for free.

With bullish analyst sentiment and surging estimates fueling the run, investors are left to consider if Nuvation Bio’s rally still has room to grow or if the market has already priced in the next phase of growth.

Price-to-Book Ratio of 4.8x: Is it justified?

Nuvation Bio's shares are currently trading at a price-to-book ratio of 4.8x, compared to the US pharmaceuticals industry average of 2.4x. This signals a premium relative to sector peers.

The price-to-book ratio captures how much investors are paying for each dollar of company net assets. For biotech firms, this multiple often reflects confidence in future drug pipelines and growth prospects rather than current profitability.

At 4.8x, Nuvation Bio’s valuation sits well above the industry average, suggesting the market is pricing in significant future upside. However, according to available data, its price-to-book ratio is still below the peer average of 11.6x. This means it is relatively less expensive when compared with a select group of similar companies. This highlights a split view: the valuation is high versus the broader sector, but not as high as closest rivals.

Result: Price-to-Book Ratio of 4.8x (OVERVALUED)

However, slower-than-expected revenue growth or setbacks in drug development could temper current optimism and lead to a reassessment of Nuvation Bio’s lofty valuation.

Another View: Discounted Cash Flow Perspective

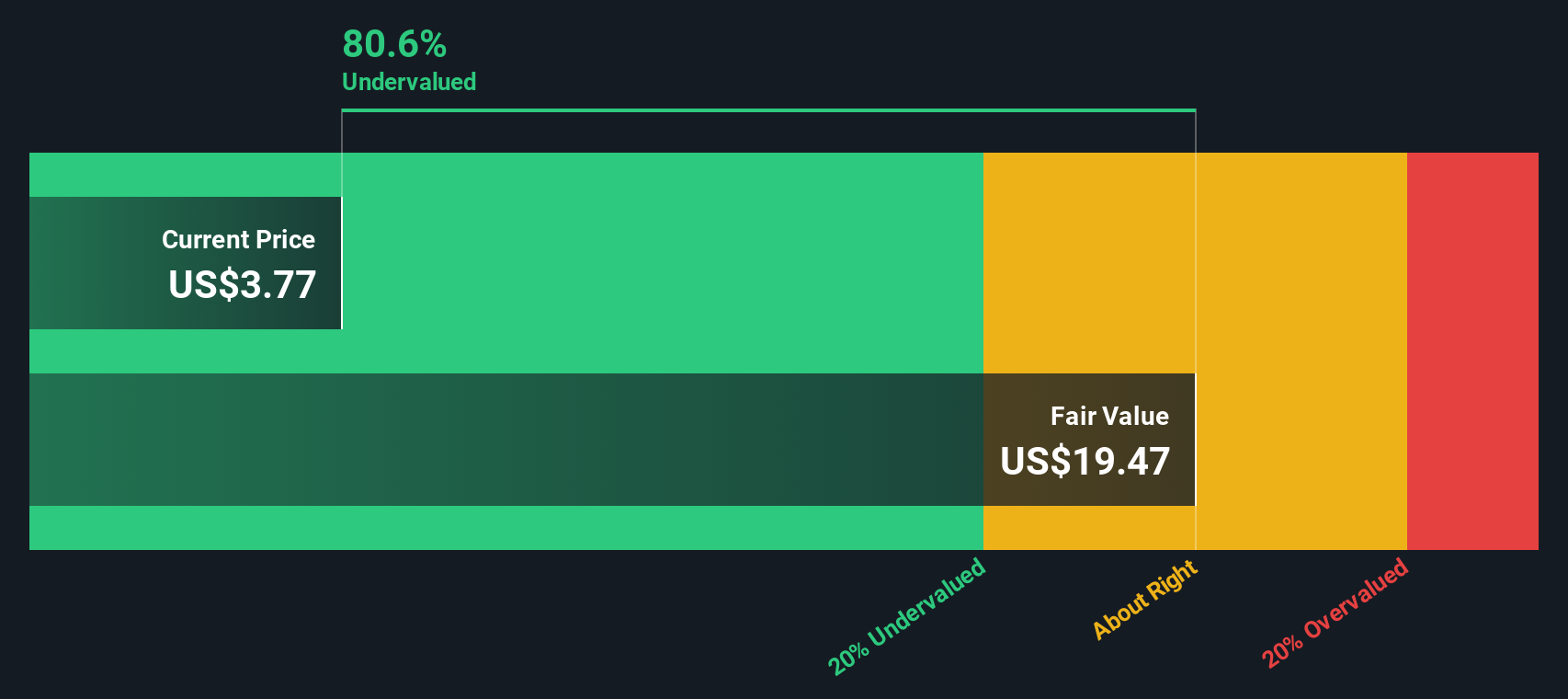

While the price-to-book ratio suggests Nuvation Bio may look expensive compared to sector averages, our DCF model presents a very different perspective. The SWS DCF model estimates fair value at $19.47 per share, indicating the stock appears undervalued by a wide margin at current prices. Could the market be overlooking long-term potential, or is this discount justified?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Nuvation Bio for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 840 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Nuvation Bio Narrative

If you have a different perspective or like to dig into the details yourself, it’s easy to build your own view in just a few minutes. Do it your way

A great starting point for your Nuvation Bio research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Set yourself up for smarter decisions by checking out unique investment themes that could deliver your next winning stock. Don't let standout opportunities pass you by.

- Tap into market-shaking momentum with these 3590 penny stocks with strong financials, offering surprising growth and financial resilience.

- Catch the AI wave and unlock potential gains by reviewing these 26 AI penny stocks, making headlines in artificial intelligence innovation.

- Pursue reliable income with these 22 dividend stocks with yields > 3%, which consistently deliver strong yields above 3% for your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.