nVent Electric (NVT) Is Up 12.1% After Raising 2026 Outlook On Record Data Center Demand – Has The Bull Case Changed?

nVent Electric plc NVT | 0.00 |

- In the first quarter of 2026, nVent Electric plc reported record sales of US$1,242 million, up from US$809.3 million a year earlier, with earnings per share from continuing operations rising despite total net income being lower than the prior year.

- The results were powered by surging data center and infrastructure demand, prompting nVent to raise its full-year sales and earnings guidance while ramping capacity, including a new Blaine, Minnesota facility.

- We’ll now examine how this guidance increase, fueled by record data center-driven orders and backlog, may reshape nVent’s investment narrative.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

nVent Electric Investment Narrative Recap

To own nVent, you need to believe that its record US$1,242 million Q1 sales, data center momentum and US$2.6 billion backlog can support continued growth while the business manages tariff headwinds and margin pressure. The raised 2026 sales and EPS guidance reinforces the data center and infrastructure story in the near term, but also amplifies the key risk that any slowdown in AI data center or infrastructure spending could quickly filter through to orders and earnings.

Among recent announcements, the most relevant is nVent’s decision to lift its full year 2026 outlook to 26% to 28% reported sales growth and US$4.45 to US$4.55 adjusted EPS. That guidance, grounded in Q1 strength and record infrastructure and data center orders, directly ties the investment case to successful execution on capacity expansions such as the Blaine, Minnesota facility and on integrating acquisitions like EPG, all while absorbing an expected US$80 million tariff headwind.

Yet against this strong backdrop, investors should be aware that concentrated exposure to AI data center spending means a sudden pause in hyperscaler CapEx could...

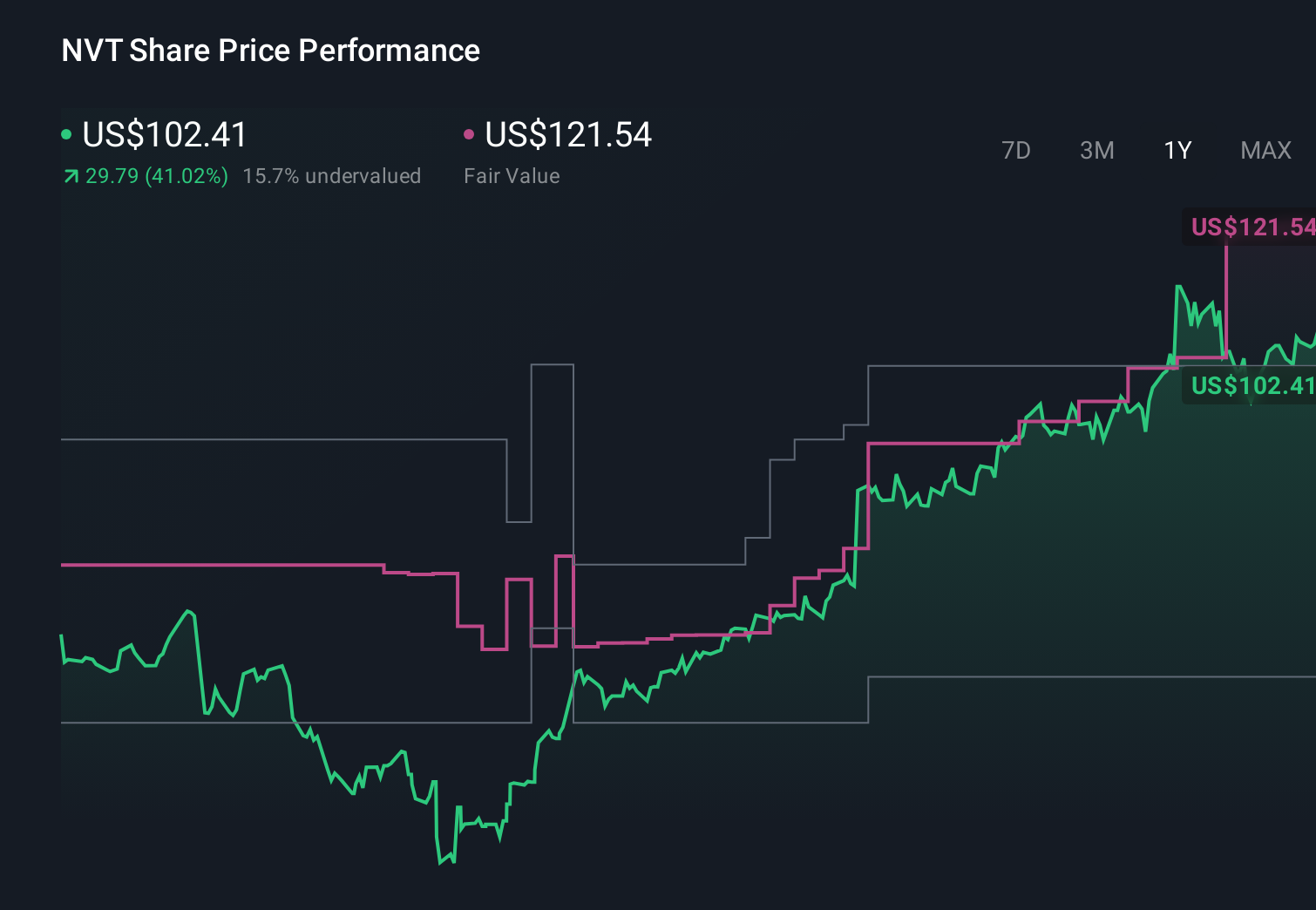

nVent Electric’s narrative projects $4.5 billion revenue and $651.5 million earnings by 2028. This requires 10.4% yearly revenue growth and about a $395 million earnings increase from $256.1 million today.

Uncover how nVent Electric's forecasts yield a $127.39 fair value, a 20% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts, who were already assuming revenue could reach about US$6.1 billion and earnings roughly US$863 million by 2029, paint a far more bullish catalyst story than consensus, while others focus more on risks like legacy product exposure and limited geographic diversity; as this latest record quarter lands, you can see how views on nVent’s future may widen further and it is worth comparing these very different expectations yourself.

Explore 5 other fair value estimates on nVent Electric - why the stock might be worth as much as $157.54!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your nVent Electric research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free nVent Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate nVent Electric's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.