nVent Electric (NVT) Is Up 5.7% After Earnings Beat And Upbeat 2026 Guidance - What's Changed

nVent Electric plc NVT | 118.92 | +1.29% |

- nVent Electric recently reported a strong quarterly earnings beat, with revenue rising 42% year over year, earnings per share topping analyst expectations, and record free cash flow supported by new liquid cooling solutions and robust demand in key infrastructure markets.

- This combination of earnings strength, optimistic guidance for full-year 2026 adjusted EPS, and portfolio expansion in liquid cooling underpins increased confidence in nVent’s positioning within high-growth infrastructure sectors.

- We’ll now examine how nVent’s robust earnings beat and upbeat 2026 guidance may influence its investment narrative and risk-reward balance.

Outshine the giants: these 21 early-stage AI stocks could fund your retirement.

nVent Electric Investment Narrative Recap

To own nVent, you need to believe that electrification, AI data centers and infrastructure upgrades will keep driving demand for its electrical and cooling solutions, and that management can execute on acquisitions without eroding margins. The latest earnings beat and record free cash flow reinforce the near term catalyst around AI data center build outs, while also heightening the key risk that any slowdown in AI or data center capital spending could quickly pressure that growth engine.

The most relevant recent announcement here is nVent’s expansion into liquid cooling, backed by new manufacturing capacity and updated data center cooling products. This directly ties into the company’s biggest current catalyst, as AI heavy data centers increasingly require advanced thermal management, and positions nVent to compete for larger, more complex projects where performance, reliability and integration matter to customers evaluating long term suppliers.

Yet against this strong story, investors should still pay close attention to the risk that AI data center demand or capital spending could suddenly...

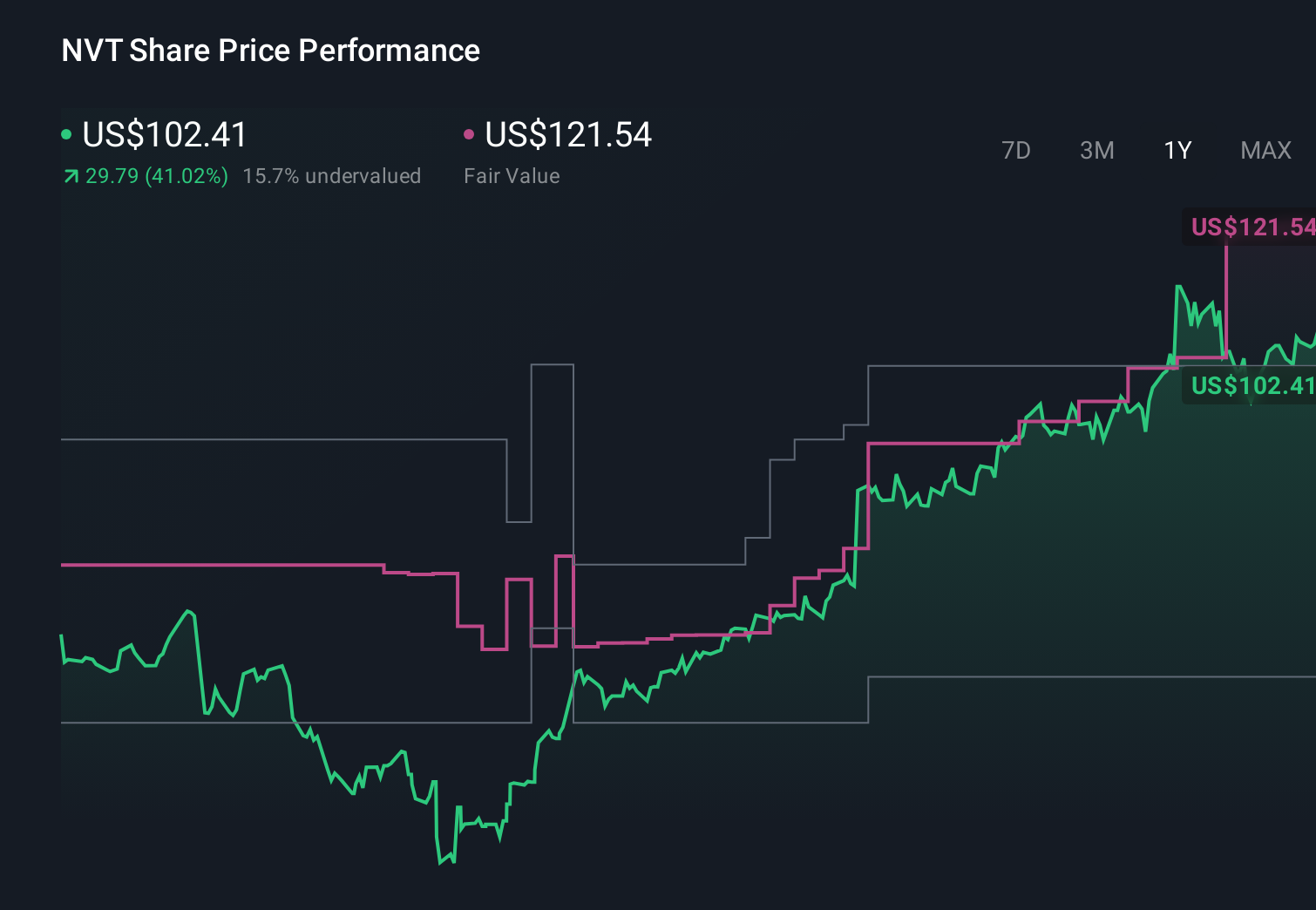

nVent Electric's narrative projects $4.5 billion revenue and $651.5 million earnings by 2028.

Uncover how nVent Electric's forecasts yield a $127.39 fair value, a 11% upside to its current price.

Exploring Other Perspectives

While consensus sees steady growth, the most optimistic analysts were already projecting revenue near US$4.8 billion and earnings around US$690 million by 2028, which is a far more bullish narrative than the baseline and could shift again as the latest AI driven cooling momentum and dependence on legacy products are reassessed.

Explore 5 other fair value estimates on nVent Electric - why the stock might be worth as much as 27% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your nVent Electric research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free nVent Electric research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate nVent Electric's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 33 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 87 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.