NVIDIA Stock And 2 Cash Flow Picks Worth A Closer Look

Mobileye Global, Inc. Class A MBLY | 0.00 |

With central banks managing currencies carefully, bond yields adjusting, and growth signals mixed across regions, many investors are looking for assets that are grounded in actual cash being generated by businesses rather than just sentiment. The Undervalued Stocks Based On Cash Flows screener focuses on companies where discounted cash flow estimates from SWS suggest a gap between current share prices and fair value. That can appeal if you want potential value opportunities supported by underlying cash flow assumptions instead of short term headlines. This article highlights three stocks from that screener that may be worth a closer look.

NVIDIA (NVDA)

Overview: NVIDIA is a US-based technology company that designs GPUs and full AI computing platforms used in data centers, gaming PCs, professional graphics workstations, and automotive systems, selling primarily to hardware manufacturers, cloud providers, and car makers around the world.

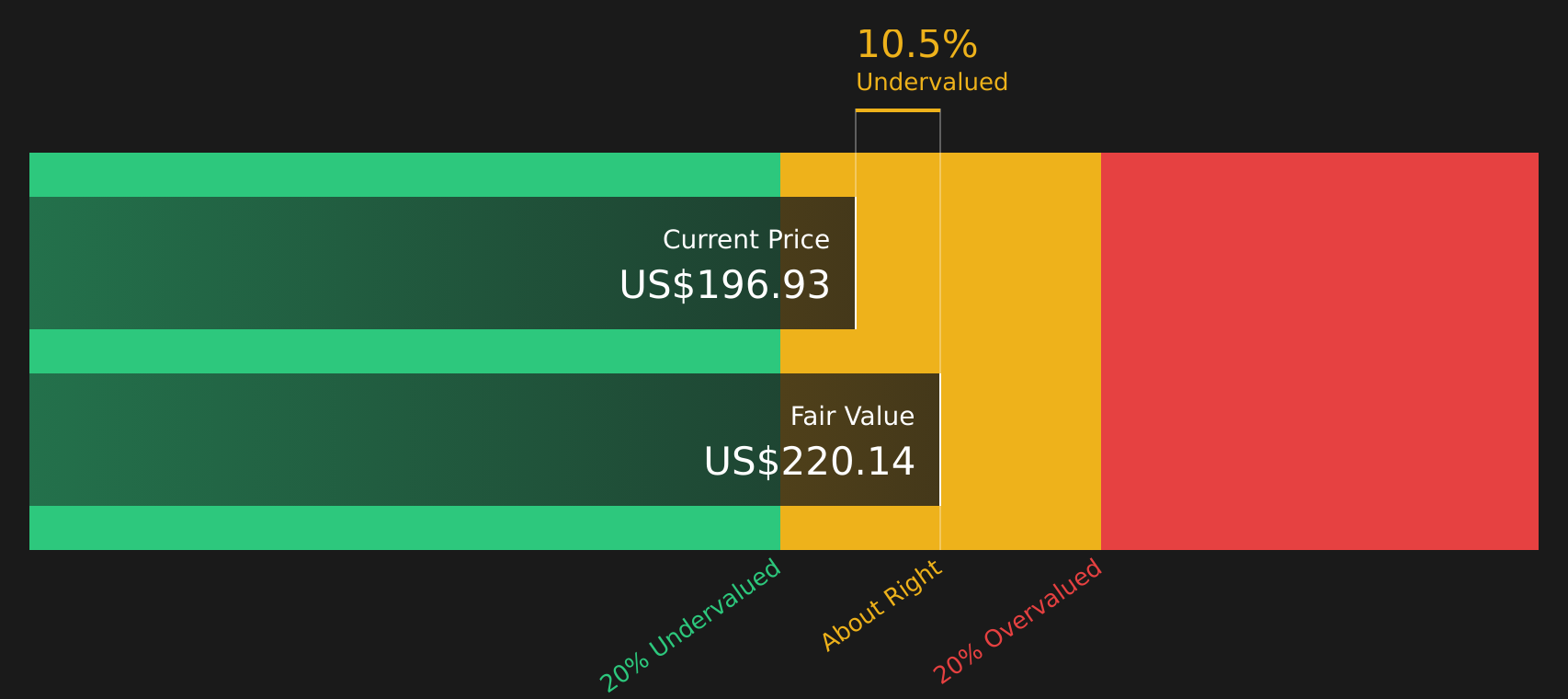

Operations: NVIDIA generates about US$25.1b from its Graphics segment and about US$228.4b from Compute & Networking, with revenue concentrated in the United States at roughly US$187.7b, followed by Taiwan and China (including Hong Kong).

Market Cap: US$4.7t

NVIDIA attracts attention because its AI data center platforms, Vera Rubin racks, DSX software stack, and broader AI factory partnerships are all tied to very high reported margins, strong earnings growth and an internal DCF estimate that stands above the current share price. At the same time, heavy reliance on external funding, significant insider selling, political scrutiny around AI and export controls, and questions over long term GPU demand concentration in data centers present risks that investors may want to consider. For readers interested in how cash flow expectations are evaluated alongside these pressures and why some investors still see potential in the stock, the full story on NVIDIA extends well beyond headline AI excitement.

NVIDIA’s substantial AI-related cash flows and high reported margins raise an important question: is the story already priced in, or is something still missing in the numbers? For a clearer view of this tension, start with the DCF valuation analysis for NVIDIA

On Holding (ONON)

Overview: On Holding is a Swiss sportswear company that designs and sells premium athletic footwear, apparel, and accessories under the On brand, serving runners and active consumers across performance running, outdoor, all-day wear, training, tennis, and youth categories through both wholesale partners and its own stores and e-commerce channels worldwide.

Operations: On Holding generates about CHF 3.1b in revenue primarily from athletic footwear, with reported geographic revenue including CHF 564.5m from Asia-Pacific.

Market Cap: US$12.2b

On Holding stands out in this cash flow focused screener because it combines a fast growing direct to consumer and e-commerce mix with premium pricing in a global sports brand that is still expanding into new categories like football. Analysts expect strong top line and earnings growth, supported by higher margin DTC sales and manufacturing approaches such as LightSpray that are intended to improve efficiency. Yet the stock trades below both Simply Wall St fair value estimates and the average analyst price target. The flip side is clear: the business leans heavily on higher prices, marketing spend, and rapid international expansion, which could pressure margins if consumer appetite or regional demand cools. That tension is central to how investors may judge On Holding’s appeal in this screener context.

On Holding’s premium pricing and rapid category expansion appear strong, but the key question is how future sales and margins are modeled. Get the full picture with the analyst forecasts for On Holding and see what the market might be missing.

Mobileye Global (MBLY)

Overview: Mobileye Global develops advanced driver assistance and autonomous driving systems, supplying cameras, chips, software, and mapping tools that help keep vehicles in lane, avoid collisions, and eventually power fully driverless cars and robotaxis for automakers and mobility platforms worldwide.

Operations: Mobileye Global generates about US$2.0b in revenue, with approximately US$2.0b from its core Mobileye segment and US$38m from Other activities.

Market Cap: US$8.1b

Mobileye Global is attracting attention because it sits at the center of the shift from basic driver assistance to higher autonomy, with automaker design wins, partnerships with platforms like Uber and Lyft, and a planned U.S. robotaxi rollout that could introduce a higher margin, recurring revenue stream on top of current ADAS sales. Forecasts point to double digit annual revenue growth and a move from heavy losses toward profitability over the next few years. A recent share buyback and raised 2026 revenue guidance signal confidence from management. The catch is execution risk: tariffs, weaker auto demand, slower customer adoption of systems like SuperVision and Chauffeur, and an already demanding P/S multiple all mean the upside story is far from risk free.

Mobileye’s push from ADAS into higher autonomy, robotaxis and recurring software revenue raises a bigger question about what is already priced in. Get the analyst forecasts for Mobileye Global and see what the current share price might be missing.

The three stocks in this article are only a starting point, and the full Undervalued Stocks Based On Cash Flows results surface 146 more companies with equally compelling cash flow stories through the Undervalued Stocks Based On Cash Flows screener. Unlock deeper insights by using Simply Wall St to filter for the specific catalysts, cash flow profiles, and valuation narratives that matter most, so you can identify ideas for your watchlist that best fit your own criteria.

Take Control of Your Investment Journey

If On Holding or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh stock ideas do not stay under the radar for long, and the strongest momentum can be caught early, before the crowd reacts and information decays. Consider acting while opportunities still appear less widely followed.

- Explore potential cash rich compounders by scanning the 18 high quality undiscovered gems that still appear under the radar for now, before momentum traders crowd the trade.

- Prepare for possible shifts in income trends by reviewing the curated 8 dividend fortresses that could help keep portfolios funded even when growth stories are dropping out of favor.

- Consider the build out of tomorrow’s infrastructure by checking the focused 52 AI infrastructure stocks featuring companies involved in the hardware and energy backbone of AI while the theme still feels early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.