NXP Semiconductors (NXPI) Has Pulled Back Sharply, Is It Still Undervalued?

NXP Semiconductors NV NXPI | 0.00 |

NXP Semiconductors (NasdaqGS:NXPI) has come into focus after recent share price moves, with the stock down 7% over the past week and 16% over the past month, yet still higher over the past year.

The recent pullback, including a 7 day share price return of down 11.57% and 1 month share price return of down 15.86%, contrasts with a stronger 90 day share price return of 44.54% and 1 year total shareholder return of 29.90%. This suggests that momentum has cooled after a strong run.

If this kind of volatility has you thinking about other opportunities in chip related infrastructure, it could be a good moment to scan the market using our 51 AI infrastructure stocks

With NXP Semiconductors now trading at $277.02 and recent returns looking mixed, the key question is whether the current price undervalues its chip portfolio and growth profile, or if the market is already pricing in future gains.

Most Popular Narrative: 8.8% Undervalued

With NXP Semiconductors last closing at $277.02 versus a most followed fair value estimate of about $303.68, the current pullback sits against a framework that treats the stock as moderately undervalued, using an 11.34% discount rate to bring future cash flows back to today.

The industrial & IoT business is seeing a broad-based cyclical recovery across all geographies, now extending beyond consumer IoT and into core industrial applications. This, combined with growing customer engagements around higher performance and Edge AI-capable MCU/MPU platforms, is setting the stage for a return to NXP's historical 8 to 12% annual growth rate in this segment, benefitting top-line performance.

Curious how a recovering industrial and IoT segment, rising margins and a future earnings profile are combined into a single fair value path? The most followed narrative leans on detailed long term revenue, earnings and profitability assumptions that are not obvious from recent share price moves or simple P/E comparisons.

Result: Fair Value of $303.68 (UNDERVALUED)

However, there are clear swing factors here, including modest end demand recovery in automotive and pressure from aggressive competitors in China that could challenge the NXP Semiconductors fair value case.

Another View on NXP Semiconductors’ Valuation

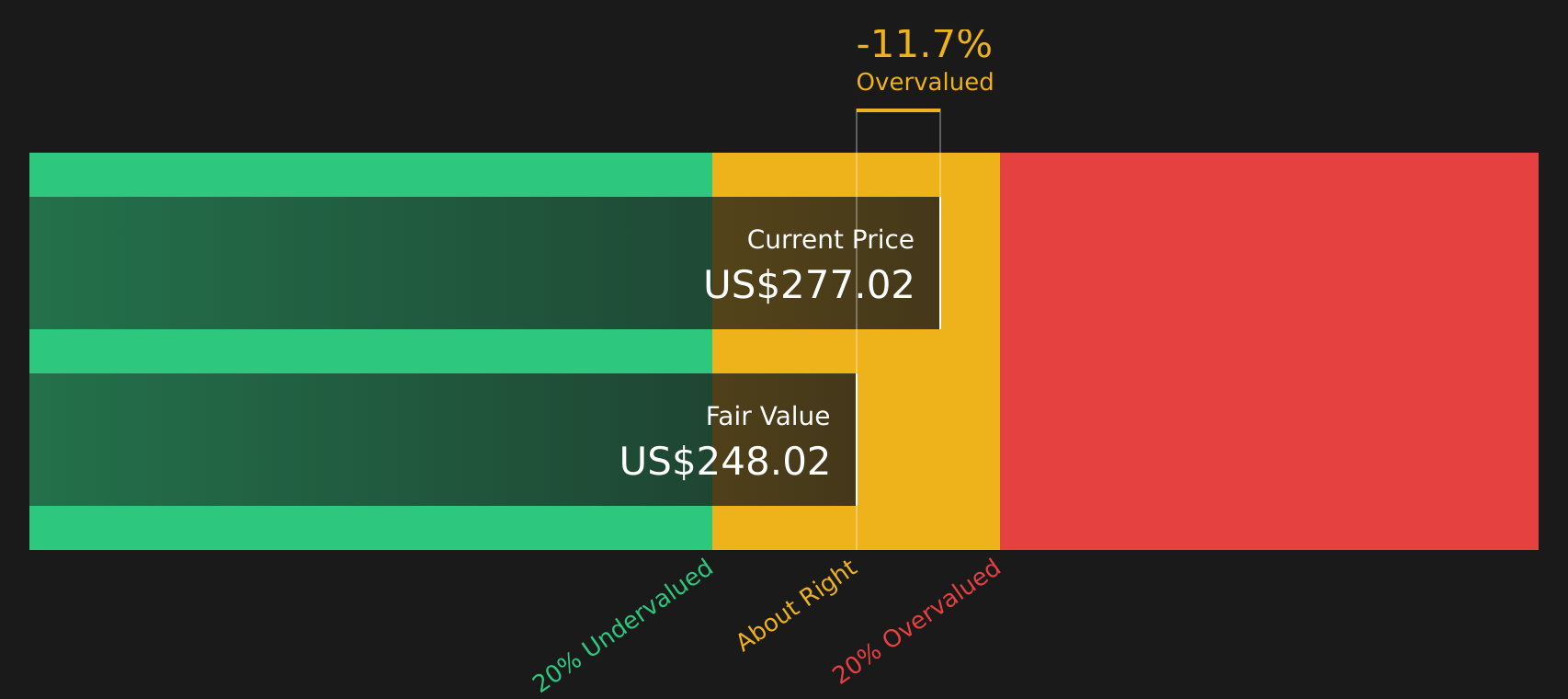

The most followed fair value narrative leans on analyst targets, but Simply Wall St’s DCF model points a little differently. On that framework, NXP Semiconductors at $277.02 is trading above an estimated future cash flow value of $250.10, which screens as overvalued rather than undervalued. That raises the question of which story you put more weight on.

For a closer look at the assumptions behind this cash flow view, including discount rate choices and growth inputs, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NXP Semiconductors for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seeing mixed signals around NXP Semiconductors and feeling uncertain? Act while the details are fresh and consider both sides by reviewing the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond NXP Semiconductors?

If NXP Semiconductors has sharpened your interest, do not stop here; cast a wider net now and keep fresh opportunities on your radar.

- Target potential bargains by scanning companies that combine quality fundamentals with attractive pricing using the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies that offer robust payouts with the 8 dividend fortresses.

- Reduce portfolio stress by focusing on companies that historically show lower overall risk profiles through the 71 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.