NXP Semiconductors (NXPI) Stock Looks Fairly Priced After A 61% Run

NXP Semiconductors NV NXPI | 0.00 |

NXP Semiconductors has delivered a 60.7% return over the past five years, yet its valuation picture is mixed, with a Discounted Cash Flow (DCF) estimate pointing to a share price that is roughly in line with intrinsic value while market multiples suggest the stock still screens as undervalued.

- A 60.7% five year return highlights that NXP Semiconductors has already rewarded long term holders, so any new upside case rests more on valuation and future cash flow than on catching an early move.

- Recent sector interest in automotive and AI related chips can support expectations for NXP Semiconductors, while geopolitical tensions and insider selling activity may keep some investors cautious about how much to pay for that growth.

- With a value score of 3 out of 6, NXP Semiconductors sits in the middle of the pack, pointing to a mixed picture rather than a clear bargain or clear overvaluation.

The issue now is whether NXP Semiconductors' current price, after its multi year run, still leaves enough valuation support if expectations cool.

Where Does NXP Semiconductors Sit on Cash Flow?

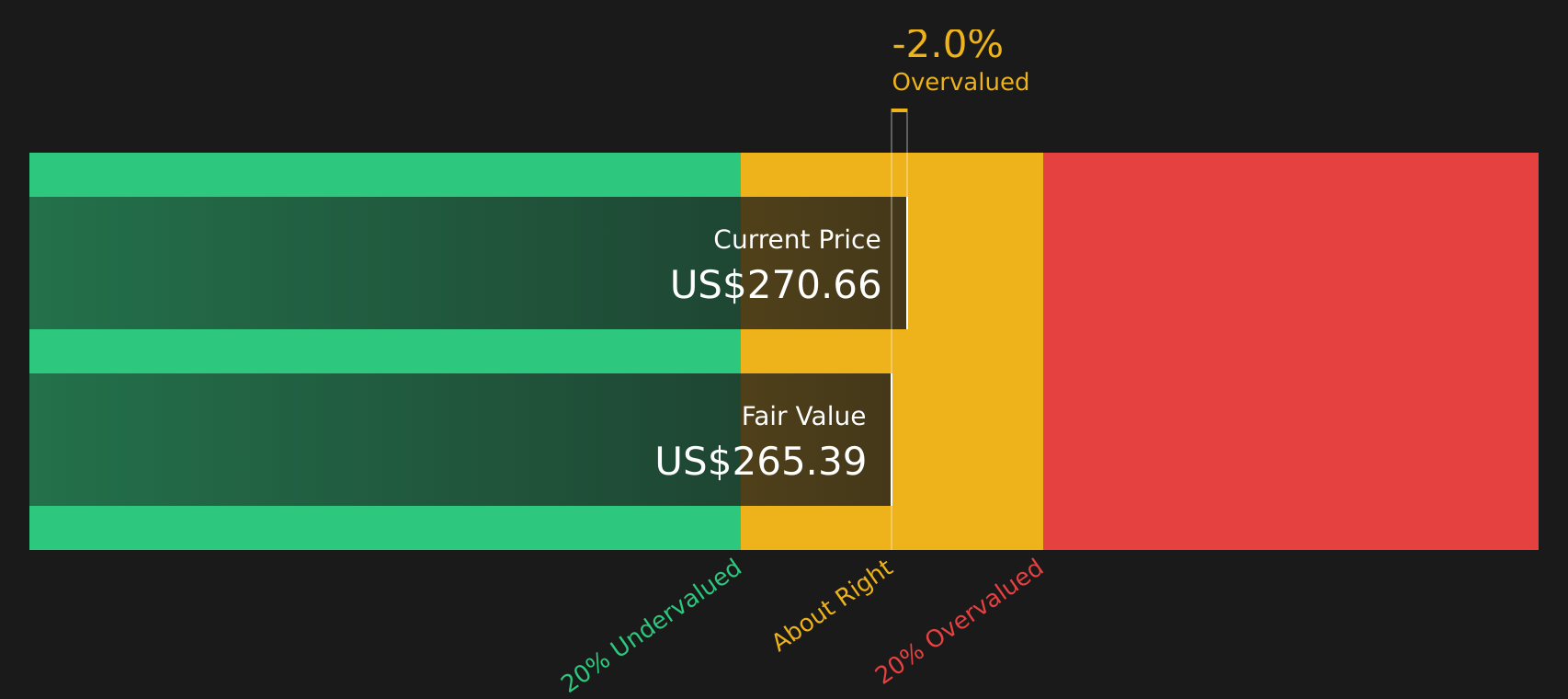

The Discounted Cash Flow (DCF) model values NXP Semiconductors by projecting future cash generation and discounting it back to today. On this view, NXP Semiconductors is treated as a business with growing but moderating free cash flow rather than an early stage high growth story.

Over the last twelve months, NXP Semiconductors generated about $2.3b in free cash flow, and the DCF assumes those cash flows continue to grow over time before settling into a slower phase. That stream of projected cash flows translates into an estimated intrinsic value of about $265 per share. This sits slightly below the current market price and implies the stock screens as roughly 7.2% overvalued on this model. The recent decline in NXP Semiconductors shares during a bout of geopolitical tension helps explain why the price is still relatively close to the DCF estimate rather than stretched far above it.

On this DCF view, NXP Semiconductors looks about fairly valued, with the current share price sitting close to its estimated intrinsic worth.

NXP Semiconductors is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Does NXP Semiconductors Look Undervalued on Earnings?

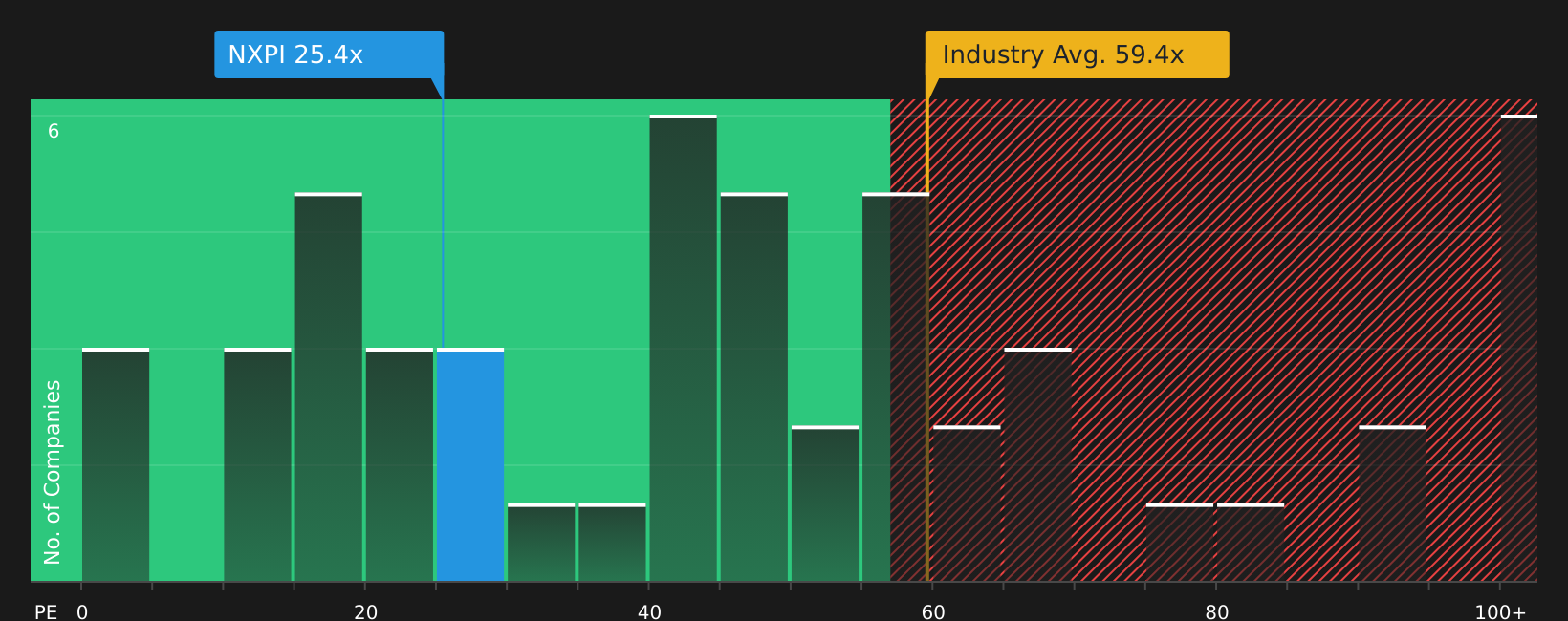

The P/E ratio is a useful lens for NXP Semiconductors because earnings are a key focus for many investors in established chip companies. NXP Semiconductors currently trades at about 27.0x earnings, which is well below the broader semiconductor industry average of around 63.4x and also below the peer group average of roughly 66.4x.

On a more tailored view that adjusts for NXP Semiconductors' size, profitability and risk profile, a fair P/E of about 38.0x is implied. This is meaningfully higher than the present 27.0x, which indicates that the stock trades at a discount to where this framework would place it, even after recent sector enthusiasm around automotive and AI related chips.

On the P/E multiple, NXP Semiconductors appears undervalued relative to both its industry and an adjusted fair value benchmark.

The NXP Semiconductors Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for NXP Semiconductors link the valuation puzzle to explicit scenarios, setting out what paths for NXP Semiconductors' revenue growth, margins and earnings could justify a meaningfully higher or lower share price than today. These narratives sit on the company’s Community page. Where a ratio or model gives a single figure, these narratives describe the future conditions that figure relies on so you can watch how reality compares.

The community views on NXP Semiconductors sit far apart, with one camp focused on auto and physical AI upside and the other on execution risk and macro pressure.

Bull case: 7% undervalued

"NXP's strong design win momentum, especially with content-rich solutions like S32 processors and radar, positions the company to realize above-market revenue growth and expanding gross margins as auto content per vehicle rises..."

Bear case: 22% overvalued

"NXP Semiconductors is facing uncertainty due to macroeconomic challenges such as tariffs, which could negatively impact future revenue and overall demand, especially considering the potential indirect effects that remain unknown..."

Do you think there's more to the story for NXP Semiconductors? Head over to our Community to see what others are saying!

The Bottom Line

For NXP Semiconductors, the Discounted Cash Flow (DCF) view points to a share price that sits close to intrinsic value, so the stock does not look obviously cheap on cash generation alone. The P/E comparison, however, still flags NXP Semiconductors as undervalued relative to peers, which reflects different expectations around growth and how the sector is being priced. With broader valuation checks landing in the middle of the range, the key question is whether earnings and cash flows from auto and AI related chips develop strongly enough to support a higher multiple, or whether current caution around execution and macro risk proves justified.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.