ON Semiconductor (ON) Joins Russell Growth Indexes As Fair Value Stays In Focus

ON Semiconductor Corporation ON | 0.00 |

ON Semiconductor (ON) is back in focus after its addition to several Russell growth benchmarks, a shift that can draw more index-linked capital and put recent sector momentum under a brighter spotlight.

Alongside its Russell growth index inclusions, ON Semiconductor has seen a mix of signals, with the share price down 1.95% over the last day and 12.90% over 30 days, yet up 39.78% over 90 days and delivering a 60.66% 1 year total shareholder return and 173.00% 5 year total shareholder return. This points to momentum that has cooled recently after strong multi year gains.

If ON Semiconductor’s role in semiconductors has your attention, it could be a useful moment to broaden your watchlist with other AI infrastructure plays using the 52 AI infrastructure stocks

For ON Semiconductor, the recent gains, index inclusion and insider selling all point in different directions. How much of today’s price really lines up with the current business versus a swing in sentiment as enthusiasm around semis builds?

Most Popular Narrative: 8% Undervalued

ON Semiconductor's most followed narrative places fair value at $103.97 per share compared with the last close at $95.96, framing the recent pullback as a discount to those long term assumptions.

The analysts have a consensus price target of $103.97 for ON Semiconductor based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $130.0, and the most bearish reporting a price target of just $68.0.

Want to understand why this fair value sits above today's price? The core of the narrative is a sharp earnings ramp, richer margins and a future earnings multiple that needs the business to keep compounding. Curious which specific growth and profitability assumptions have to land to support that outcome?

Result: Fair Value of $103.97 (UNDERVALUED)

However, ON Semiconductor’s heavy reliance on cyclical automotive demand and ongoing manufacturing underutilization could pressure margins and challenge the optimistic earnings path described in this narrative.

Another View: SWS DCF Puts ON Semiconductor In A Different Light

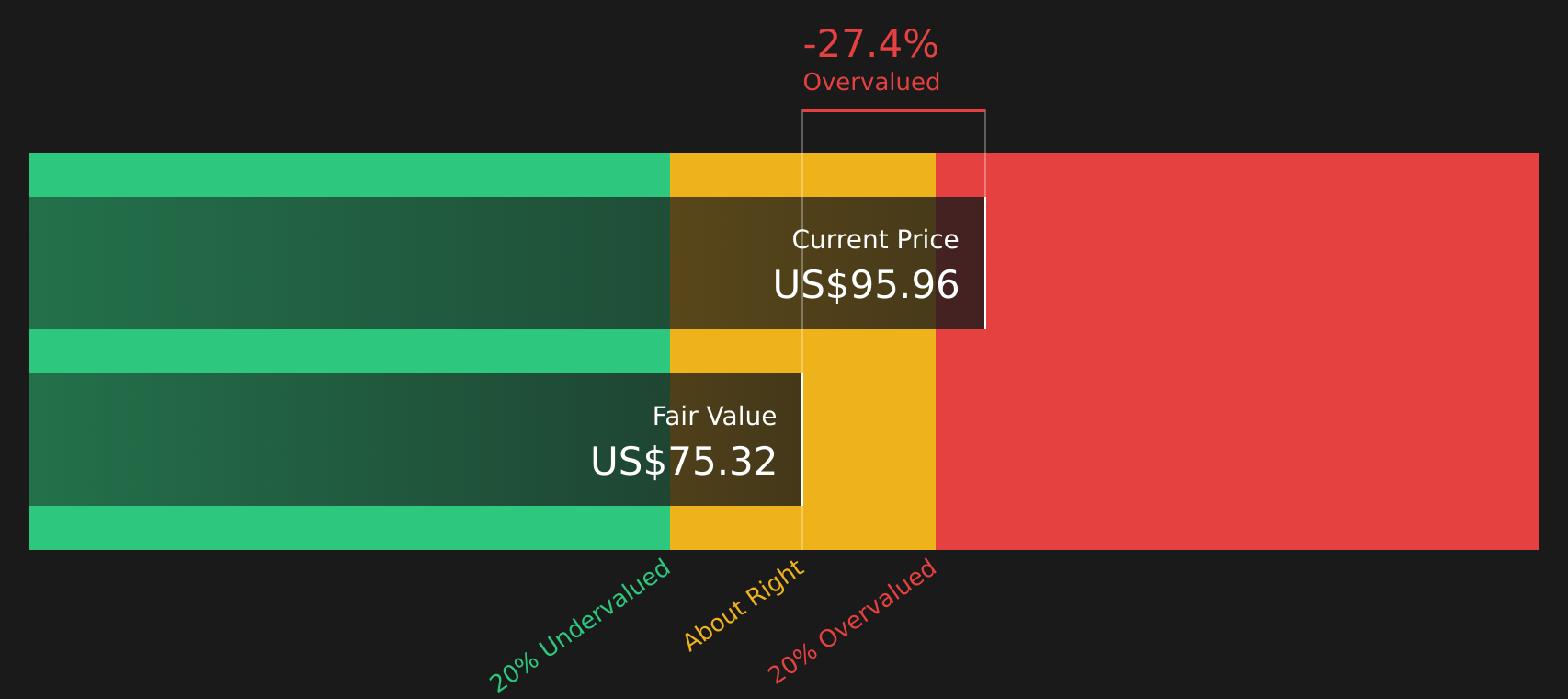

While the popular narrative has ON Semiconductor trading about 8% below a $103.97 fair value based on analyst earnings assumptions and multiples, the Simply Wall St DCF model points the other way. On this cash flow view, the stock at $95.96 sits above an estimated fair value of $75.46, so the market price builds in richer long term cash flow expectations than that model supports.

For investors comparing these two approaches, the question is whether to lean more on the earnings multiple story or on the cash flow math when weighing upside versus downside risk from here.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ON Semiconductor for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around ON Semiconductor leave you undecided, this is a good moment to review the full picture yourself and move quickly to shape your own view by weighing the 1 key reward and 3 important warning signs.

Looking for more investment ideas beyond ON Semiconductor?

If ON Semiconductor has sharpened your thinking, do not stop here. Use these focused stock ideas to widen your opportunity set before the market moves on.

- Target potential mispricings by scanning companies that combine earnings quality with attractive valuations through the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies with robust, higher yielding payouts using the 9 dividend fortresses.

- Dial down portfolio risk by filtering for businesses with resilient finances using the 76 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.