ON Semiconductor (ON) Stock Could Be 30% Expensive Following Its $7b AI Deal

ON Semiconductor Corporation ON | 0.00 |

ON Semiconductor stock has delivered a strong 169.6% return over the past 5 years, yet current valuation checks suggest investors are now paying a premium, with both the Discounted Cash Flow (DCF) intrinsic value estimate and market multiples pointing to the shares screening as overvalued.

- Across 5 years, a 169.6% total return highlights how much of ON Semiconductor's story is already reflected in the share price.

- The planned US$7b all stock acquisition of Synaptics may support a larger addressable market in physical and edge AI. However, integration risks and the recent sharp pullback in semiconductor sentiment can weigh on how much investors are willing to pay for that potential.

- ON Semiconductor passes just 1 of 6 valuation checks, which leans toward the stock looking expensive rather than like a clear bargain.

The issue now is whether ON Semiconductor's current price leaves enough margin for error compared with its intrinsic value signals.

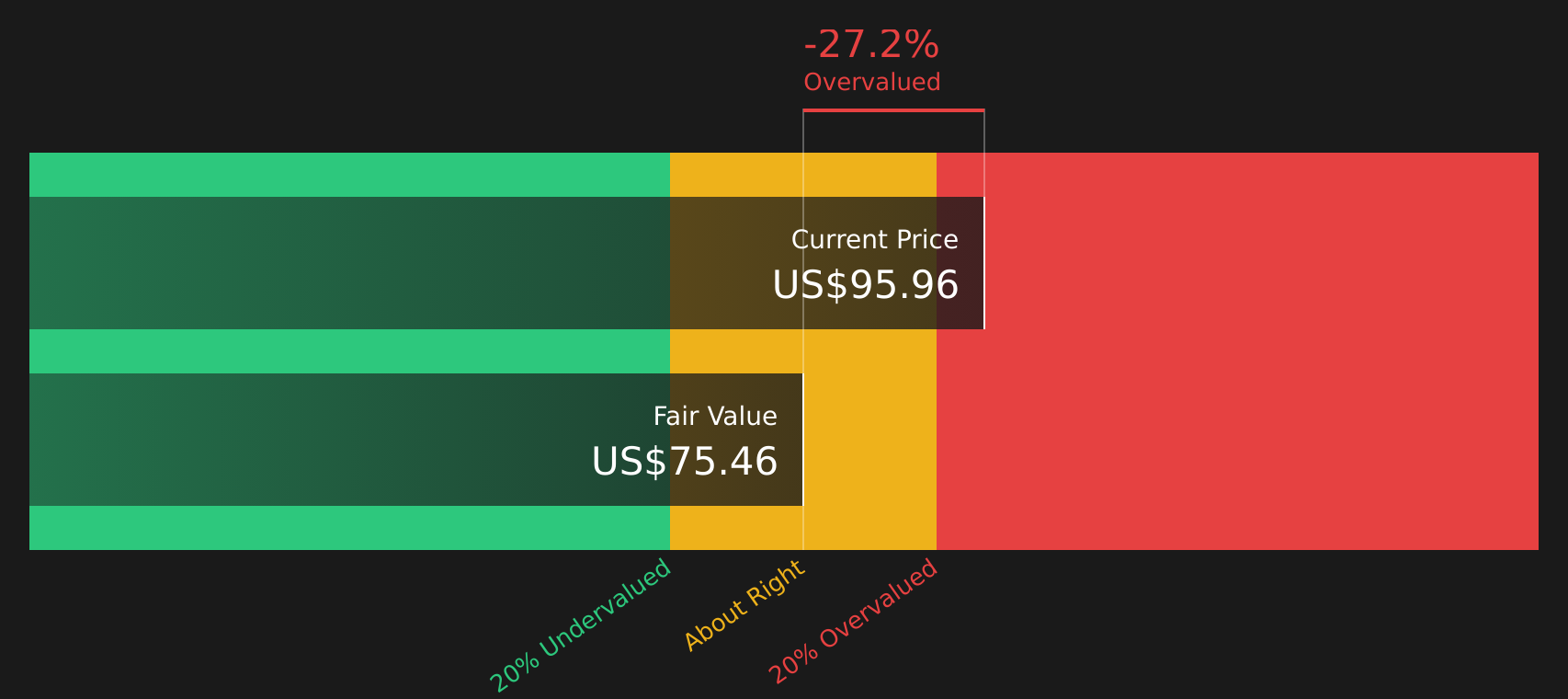

Is ON Semiconductor Getting Expensive on Cash Flow?

The Discounted Cash Flow (DCF) model estimates what ON Semiconductor could be worth based on the cash it is expected to generate for shareholders. ON Semiconductor produced about $744.7 million in free cash flow over the latest twelve months, and the model assumes these cash flows keep growing from here rather than shrinking.

On those assumptions, the DCF points to an estimated intrinsic value of about $75 per share, which is well below the current market price and implies the stock screens as overvalued by roughly 29.9%. The planned $7 billion all-stock acquisition of Synaptics adds potential for a larger AI-focused business. However, the sharp price reaction and investor scrutiny around the deal help explain why the market is already assigning a relatively high value to ON Semiconductor compared with what its cash flows currently support.

Overall, the discounted cash flow work indicates that ON Semiconductor stock currently appears overvalued relative to its intrinsic value estimate.

Our Discounted Cash Flow (DCF) analysis suggests ON Semiconductor may be overvalued by 29.9%. Discover 44 high quality undervalued stocks or create your own screener to find better value opportunities.

Does ON Semiconductor Look Pricey on Earnings?

P/E is a useful way to look at ON Semiconductor because earnings are a key focus for mature chip companies that already generate profits. ON Semiconductor currently trades on a P/E of about 66.4x, compared with a semiconductor industry average of around 62.8x and a peer group average near 79.5x, so the stock sits above the broader sector but below some closer peers.

The fair P/E ratio implied by the model, which blends ON Semiconductor's growth expectations, profitability, size and risk profile, is about 54.6x. That is meaningfully lower than the current 66.4x, suggesting investors are paying a premium to what the fundamentals alone would indicate. Combined with the DCF work, this indicates ON Semiconductor appears expensive rather than like a clear bargain on earnings.

Taken together, ON Semiconductor screens as overvalued on its P/E multiple relative to a tailored fair-value benchmark.

The ON Semiconductor Narrative: What Would Justify Today's Price?

ON Semiconductor's valuation picture raises clear questions about what kind of future the current share price is already pricing in. This is where Simply Wall St Narratives on the Community page come in as a bridge between the numbers and the story. Instead of stopping at a single ratio or model output, they set out the specific assumptions on growth, margins and earnings that those figures rest on, so you can watch how ON Semiconductor's actual progress lines up with that roadmap over time.

ON Semiconductor community views are split between a bullish scenario that sees the stock as materially undervalued and a bearish one that sees meaningful downside risk still in play.

Bull case: 33% undervalued

"ON's early-mover advantage in next-generation AI data center power architectures in partnership with XPU leaders like NVIDIA positions the company to capitalize on the exponential increase in semiconductor content per watt..."

Bear case: 15% overvalued

"Intensifying competition and potential overcapacity in power management and silicon carbide products threaten to erode prices and result in higher inventory levels..."

Do you think there's more to the story for ON Semiconductor? Head over to our Community to see what others are saying!

The Bottom Line

For ON Semiconductor, both the Discounted Cash Flow (DCF) intrinsic value estimate and the P/E based fair-value model currently point in the same direction, with the stock screening as overvalued rather than obviously cheap. The broader valuation checks are weak, so the burden of proof now sits with the future execution story rather than the price doing investors any favors upfront. The key debate from here is whether ON Semiconductor can deliver the growth, margins and cash generation that would make today's premium look justified, or whether expectations need to come down along with the valuation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.