Optimum Communications (OPTU) Margin Collapse With US$3.47 EPS Loss Tests Bullish Turnaround Narrative

Optimum Communications, Inc. Class A OPTU | 1.37 | +3.01% |

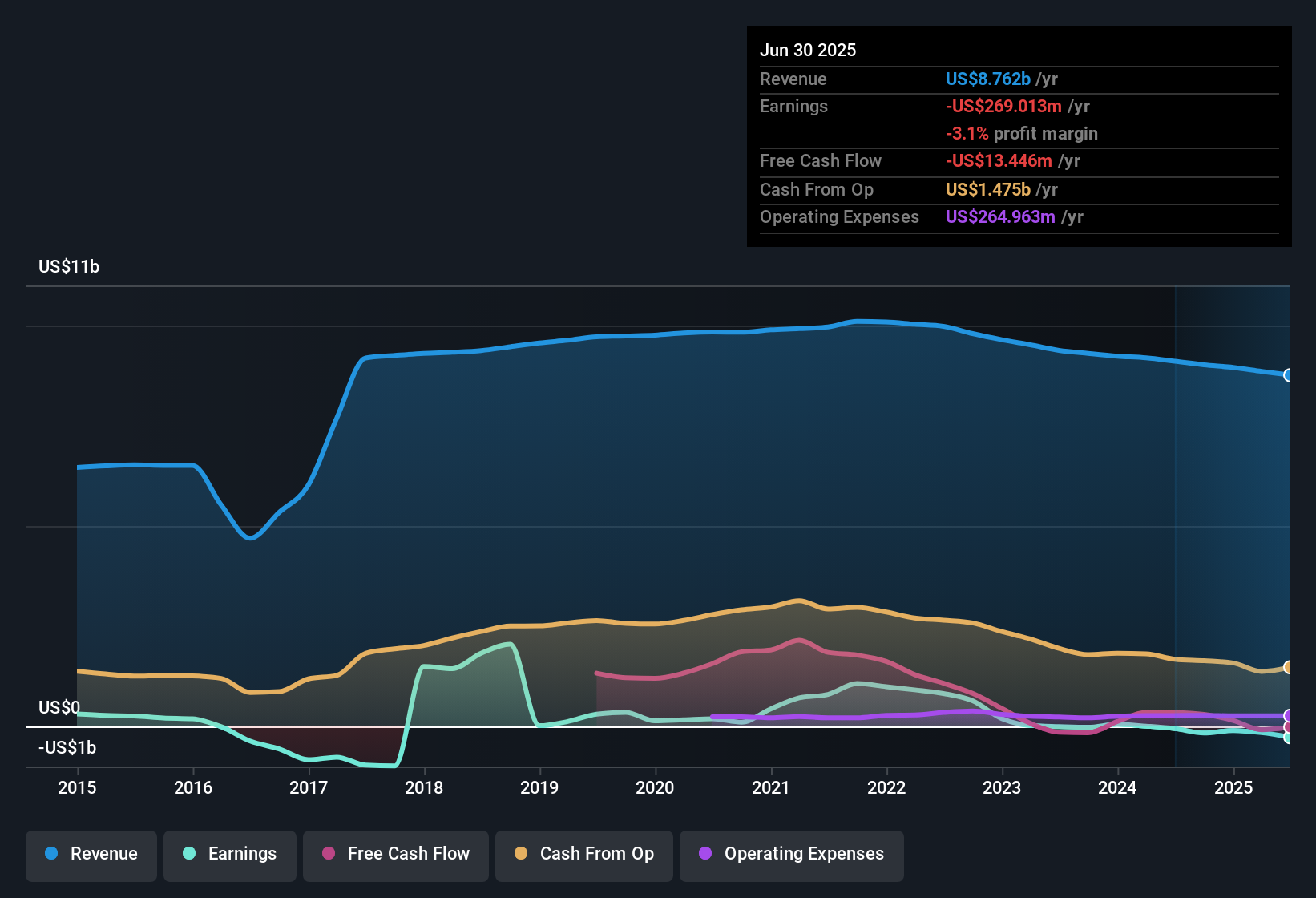

Optimum Communications (OPTU) has put out a tough FY 2025 third quarter print, with revenue of US$2.1 billion alongside a basic EPS loss of US$3.47 and net income loss of US$1,625.9 million. The company has seen quarterly revenue move from US$2,240.8 million in FY 2024 Q2 to US$2,108.1 million in FY 2025 Q3, while EPS has swung from a profit of US$0.03 per share to a loss of US$3.47, setting up a results season where investors are focused squarely on how much pressure is building on margins.

See our full analysis for Optimum Communications.With the numbers on the table, the next step is to line these results up against the current Optimum Communications narratives to see which stories hold up and which ones the latest margin picture calls into question.

Losses widen to US$1.6b on steady US$2.1b revenue base

- On about US$2.1b of Q3 revenue, Optimum booked a net loss of US$1.6b and basic EPS of US$3.47 loss, versus losses between roughly US$43 million and US$96 million in each of the five prior quarters on revenues around US$2.1b to US$2.2b.

- Consensus narrative talks up margin improvement over time. However, the last twelve months show a net loss of US$1.9b on US$8.6b of revenue, which keeps margins firmly negative even as analysts expect earnings growth and a path to profitability.

- Trailing net losses have expanded from US$56.8 million to US$1.9b over the last five reported trailing twelve month sets, while revenue has stayed near US$9b, so the gap between sales and profits is still wide.

- That sits alongside the view that earnings could grow about 69.85% per year with profitability within three years. As a result, you are comparing a very loss making recent record with an improving margin story in the models.

Multi year loss trend versus bullish turnaround story

- Over the past five years, losses are reported to have grown at about 78% per year, and on the latest trailing twelve month view earnings are US$3.98 loss per share. This is a very different picture to the bullish idea of earnings reaching US$338.7 million by around 2028.

- Bulls argue that fiber expansion, AI driven efficiency gains and higher margin add ons could support a strong earnings recovery. Yet the reported trailing net loss of US$1.9b and the recent step up in quarterly losses mean the business is starting that journey from deep in the red.

- The bullish narrative assumes margins move from about 3.1% loss to 4.1% profit in three years, while the current trailing twelve month figures still show losses that are more than 20x larger than the worst quarterly loss before FY 2025 Q3 in your data set.

- Analysts in that optimistic camp are effectively building their case on margin improvement and not on revenue growth, because revenue is expected to decline around 1.9% per year even as earnings are projected to climb.

Cheap P/S, heavy balance sheet risks

- Optimum is trading on a P/S of about 0.1x using the provided revenue base, compared with 0.9x for the US Media industry and 3.2x for peers, and the current share price of US$1.68 sits well below the DCF fair value of about US$3.85.

- Bears focus on negative shareholders equity and weak interest coverage, and the combination of US$1.9b of trailing losses with interest payments that are not well covered by earnings is exactly the sort of balance sheet profile that can offset the appeal of a low P/S multiple.

- Even though the valuation data suggests the stock trades at a large discount to the DCF fair value of US$3.85, the same dataset flags that revenue is expected to slip about 0.7% per year, so the case does not rest on top line growth bailing out the capital structure.

- Critics highlight that a company with negative equity and ongoing losses has less room to absorb shocks, which is why some investors will weigh the apparent valuation gap against the risk that more capital might eventually be needed.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Optimum Communications on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the figures another way? Turn that view into your own narrative in just a few minutes and put your thesis on record with Do it your way

A great starting point for your Optimum Communications research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

See What Else Is Out There

Optimum Communications is wrestling with heavy losses, negative equity and weak interest coverage, even as the bullish story leans heavily on future margin improvement.

If that mix of deep losses and balance sheet strain feels like a stretch, you may want to shift your attention toward solid balance sheet and fundamentals stocks screener (45 results), where companies start from a stronger financial footing and fewer debt worries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.