Otis Worldwide’s New Debt Offering Might Change the Case for Investing in OTIS

Otis Worldwide Corporation OTIS | 0.00 |

- In early September 2025, Otis Worldwide completed a US$500 million fixed-rate senior unsecured note offering at 5.131% due 2035, with proceeds primarily allocated for debt repayment and general corporate purposes.

- This proactive refinancing approach reflects Otis Worldwide’s emphasis on maintaining financial flexibility and optimizing its capital structure amid changing market conditions.

- We’ll explore how this major debt offering could influence Otis Worldwide’s investment narrative, especially regarding its balance sheet management and future growth plans.

These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Otis Worldwide Investment Narrative Recap

To have conviction as an Otis Worldwide shareholder, you need to believe in the company’s ability to sustain and grow high-margin recurring service revenues as modernization and urbanization trends evolve, despite headwinds in new equipment demand. The recent US$500 million note issuance provides extra balance sheet flexibility, but on its own does not materially shift the immediate catalysts or the most pressing risk, ongoing margin and revenue pressure in key markets like China and soft commercial construction in the Americas and EMEA.

Among recent announcements, Otis’s selection for the Cross Island MRT Line project in Singapore is most aligned with the catalyst of expanding new equipment and installed base outside China. This major infrastructure win speaks to Otis’s ability to capitalize on urban mobility demand in growth markets, which remains crucial to offsetting segment and regional weakness elsewhere.

Yet investors should also be aware: conversely, recurring service revenue growth could prove more at risk than assumed if building technology adoption accelerates…

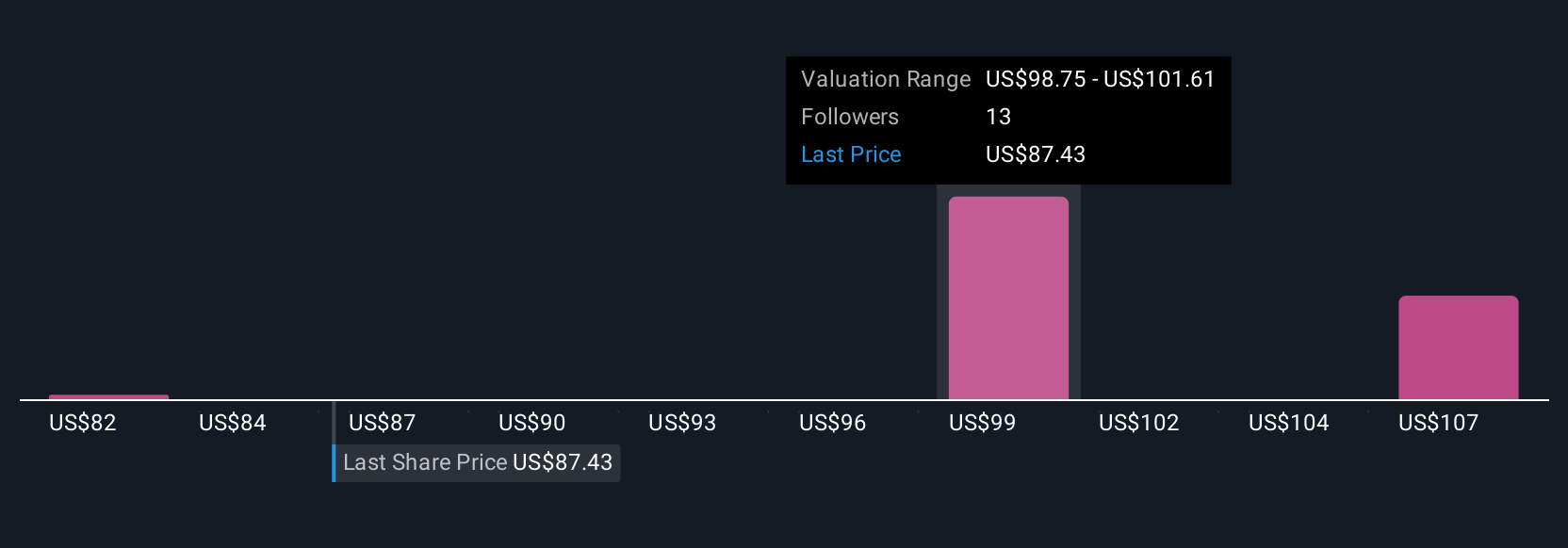

Otis Worldwide's narrative projects $16.4 billion revenue and $1.9 billion earnings by 2028. This requires 5.0% yearly revenue growth and a $0.4 billion increase in earnings from $1.5 billion currently.

Uncover how Otis Worldwide's forecasts yield a $101.31 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Four individual fair value estimates from the Simply Wall St Community range from US$81.56 to US$110.34 per share. As you weigh these diverse outlooks, consider how recurring service revenue strength could matter more if new equipment challenges persist in global markets.

Explore 4 other fair value estimates on Otis Worldwide - why the stock might be worth 6% less than the current price!

Build Your Own Otis Worldwide Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Otis Worldwide research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Otis Worldwide research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Otis Worldwide's overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.