Otter Tail (OTTR) Stock After PVC Litigation Settlements Is The Valuation Reset Just Getting Started

Otter Tail Corporation OTTR | 0.00 |

Otter Tail (OTTR) has agreed to settle a major portion of its PVC pipe antitrust litigation, with plans to pay US$39.5 million and US$34 million to two plaintiff classes, while one class action remains active.

The legal settlement has arrived at a time when the share price has been relatively steady, with an 8.67% year-to-date share price return and a 5-year total shareholder return of 103.10%. This suggests long-term holders have been rewarded even as shorter-term momentum has been modest.

If this kind of risk reset has you thinking about what else is out there, it could be a good moment to scan other utilities and infrastructure ideas via our 34 power grid technology and infrastructure stocks

With the stock trading near its analyst price target, steady recent returns and an ongoing legal overhang, you have to ask yourself: Is Otter Tail quietly undervalued here, or has the market already priced in its future growth?

Most Popular Narrative: 2.2% Undervalued

Otter Tail's most followed valuation narrative pegs fair value at $90.50, only slightly above the last close at $88.51. This frames a very tight valuation gap.

The anticipated phaseout of renewable energy credits and new restrictions under recent federal legislation threaten the economics of Otter Tail's future renewable projects beyond its currently secured solar and wind investments, potentially raising capital requirements and pressuring future earnings growth by reducing the after-tax returns on major rate base expansions.

Want to understand why this narrative still supports a premium to today’s price? It leans on steady revenue, slimmer margins, and a richer future earnings multiple. Curious which assumptions really move that fair value line?

Result: Fair Value of $90.50 (ABOUT RIGHT)

However, that “about right” narrative could crack if the US$1.4b capital plan struggles to win timely rate recovery, or if PVC litigation costs and outcomes differ from expectations.

Another View: P/E Ratios Paint a Different Picture

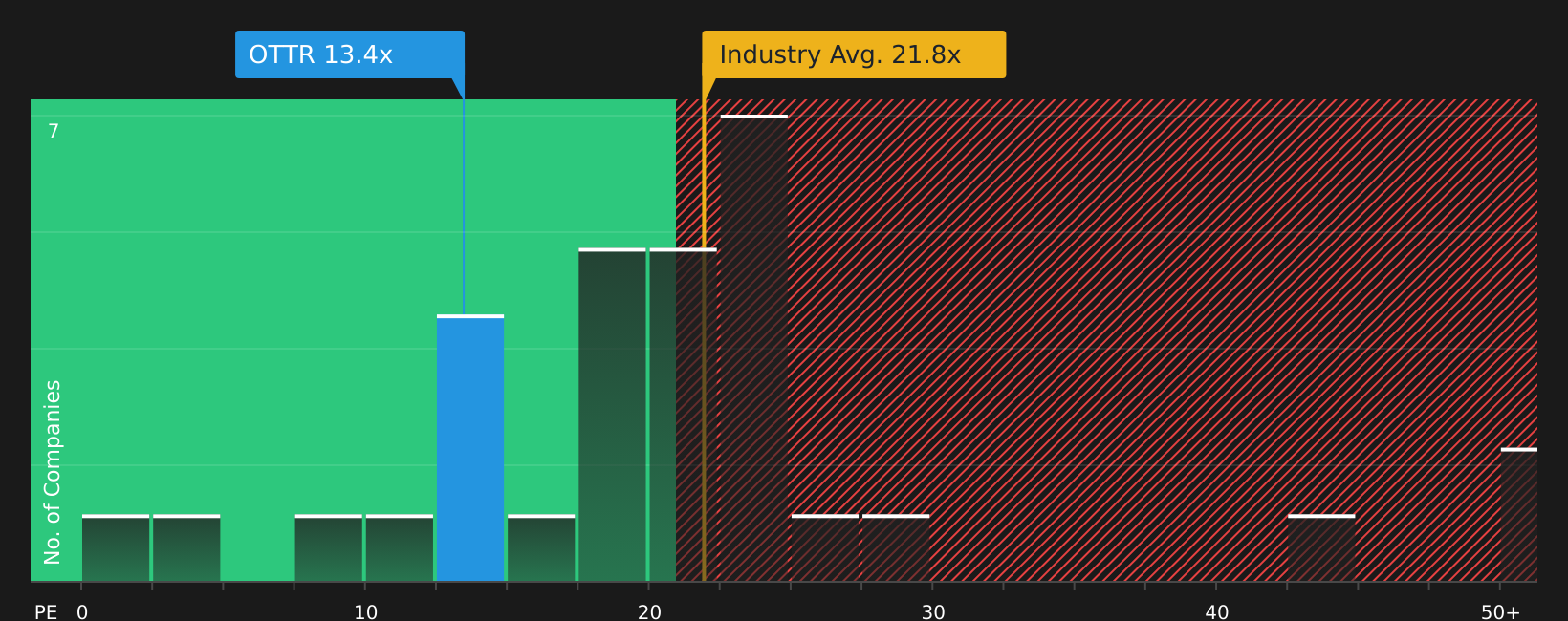

The consensus narrative treats Otter Tail as roughly fairly priced around $90.50, yet its current P/E of 13.3x looks low next to the US Electric Utilities industry at 21.7x and a 26.4x peer average, while sitting just above a 13.2x fair ratio. That gap hints at valuation risk on one side and potential opportunity on the other, so the question becomes which number you put more weight on: the model or the market?

To see how this P/E gap could matter for your thesis, especially with Otter Tail screening as good value against industry and peers, it is worth stress testing the earnings and multiple assumptions in the valuation breakdown. From there, you can ask what would need to change for the stock to move closer to that fair ratio. See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly split between risk and reward, this is the moment to look through the numbers yourself and decide what really matters for your portfolio. To see both sides laid out in one place, start with the 1 key reward and 3 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you could miss stronger income, value, or resilience elsewhere, so use screeners to widen your opportunity set fast.

- Target steady income by reviewing companies that qualify as 8 dividend fortresses and see which yields could fit your cash flow goals.

- Hunt for value by scanning the 46 high quality undervalued stocks and compare businesses that pair quality metrics with appealing prices.

- Prioritise resilience by focusing on companies in the 67 resilient stocks with low risk scores and check which ones line up with your risk tolerance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.