Ouster (OUST) Stock Valuation After Rev8 Manufacturing Expansion And New BlueCity Lidar Launch

Ouster, Inc. OUST | 0.00 |

Ouster (OUST) has put its Rev8 digital lidar platform at the center of several recent moves, including an expanded manufacturing partnership, a new BlueCity traffic solution, and fresh robotics collaborations that spotlight its multi-sector ambitions.

These product launches and manufacturing moves have arrived alongside strong trading momentum, with a 1-day share price return of 13.52% and a 90-day share price return of 111.22%. The 1-year total shareholder return stands at 126.92%, pointing to strong recent gains after a much weaker 5-year total shareholder return, which is still down 64.95%.

If lidar and robotics get you thinking about where automation goes next, it is worth scanning the wider field of 33 robotics and automation stocks.

After a sharp 90-day run and a value score of 1, Ouster is trading only about 2% below an estimated intrinsic value and roughly 4% under the average analyst target. Is there still a buying opportunity here, or is future growth already priced in?

Most Popular Narrative: 13.9% Overvalued

With Ouster last closing at $45.18 and the most followed narrative pointing to a fair value around $39.67, the gap between price and model is clear and worth unpacking before looking at what is driving that view.

Ouster is tapping into the massive Intelligent Transportation Systems (ITS) market with their Blue City traffic management solution, which could drive significant revenue growth as they expand deployments across the US, Europe, and Asia. This is expected to positively impact revenue.

Want to see what kind of growth path justifies that richer price tag? The narrative leans on rapid revenue expansion, improving margins, and a punchy future earnings multiple to get there.

Result: Fair Value of $39.67 (OVERVALUED)

However, this richer narrative still runs into real hurdles, including intense lidar competition that could pressure pricing, as well as legal or tariff shocks that could unsettle costs and margins.

Another View: Cash Flows Tell a Different Story

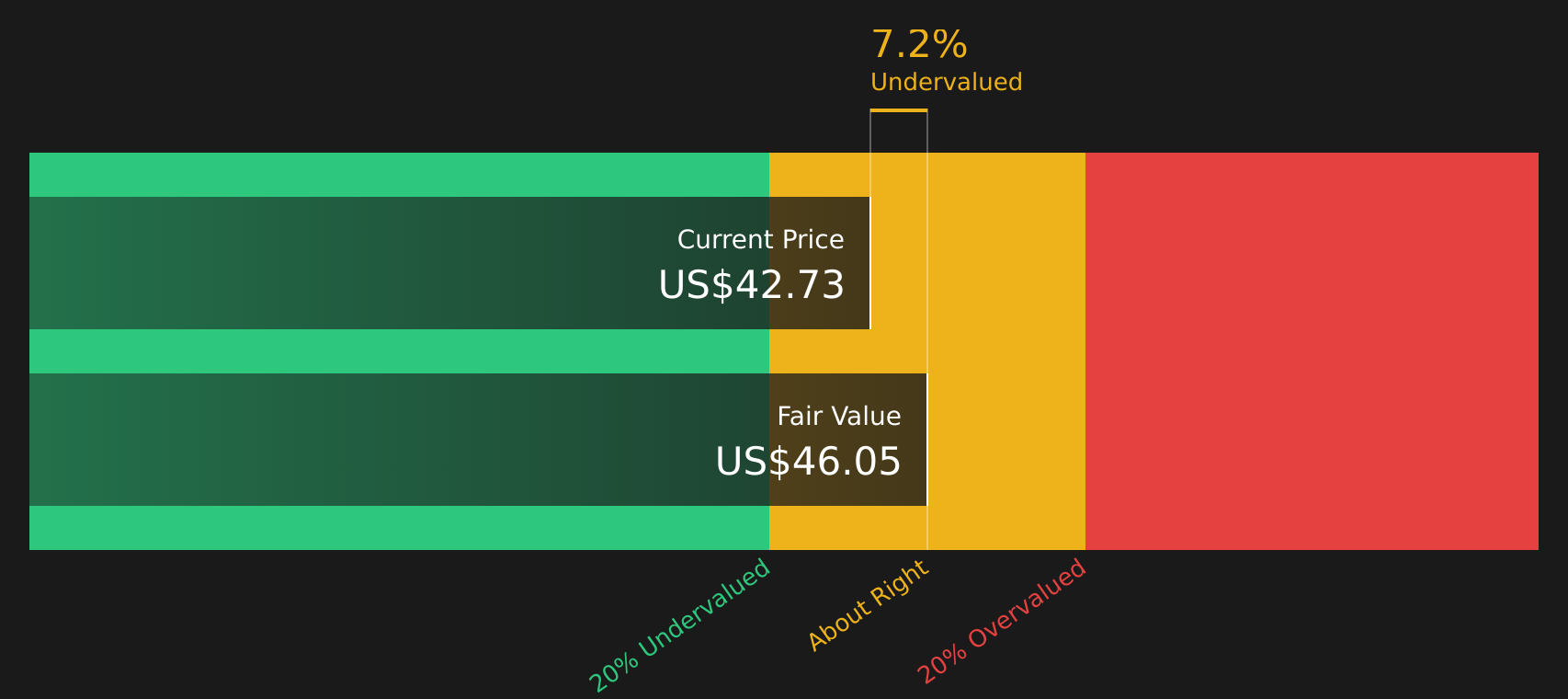

While the popular narrative flags Ouster as about 13.9% overvalued versus a $39.67 fair value, the SWS DCF model points in the other direction. On that cash flow view, Ouster at $45.18 trades roughly 2.2% below an estimated fair value of $46.21, which is a very small discount. With two models pulling in different directions, which one do you trust more for your own hurdle rate and risk tolerance?

For a closer look at how that cash flow view is built, and what would need to change in the inputs before it really pointed to a strong discount or premium, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ouster for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With the mixed signals on valuation and sentiment, do you feel the story is leaning more positive or cautious, and are you comfortable with both sides of that trade off? If you want to weigh the upside against the concerns yourself, start by checking the 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If you only focus on Ouster, you could miss out on other opportunities, so use a broader lens and let data rich stock lists spark your next move.

- Target potential value by scanning companies that combine quality fundamentals with attractive pricing through the 47 high quality undervalued stocks.

- Prioritise resilience by reviewing companies with stronger balance sheets and healthier fundamentals using the solid balance sheet and fundamentals stocks screener (48 results).

- Spot potential future standouts early by checking the screener containing 20 high quality undiscovered gems before everyone else starts paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.