Overlooked US Small Caps With Strong Balance Sheets Investors Are Missing

Oceaneering International, Inc. OII | 0.00 |

Inflation worries, shifting rate expectations and currency moves are keeping big institutions focused on headline risks instead of on smaller companies with solid balance sheets and consistent execution. That gap is where the High-Quality Undiscovered Gems screener comes in, surfacing small caps with strong fundamentals that many large funds are not yet paying attention to. With oil markets, central bank decisions and trade data pulling attention in different directions, this screener offers a way to concentrate on business quality rather than noise, and the article will spotlight 3 stocks from the list that stand out on those criteria.

Oceaneering International (OII)

Overview: Oceaneering International provides engineered services, subsea robotics, and specialized products to offshore energy producers, defense and aerospace programs, and industrial customers across the United States and multiple international regions.

Operations: The company generates most of its roughly US$2.8b in revenue from energy related segments led by Subsea Robotics at about US$863.5m, Offshore Projects Group at about US$586.5m, Manufactured Products at about US$577.6m, Aerospace and Defense Technologies at about US$494.0m, and Integrity Management & Digital Solutions at about US$280.5m, with the United States contributing about US$1.2b of the total.

Market Cap: US$3.9b

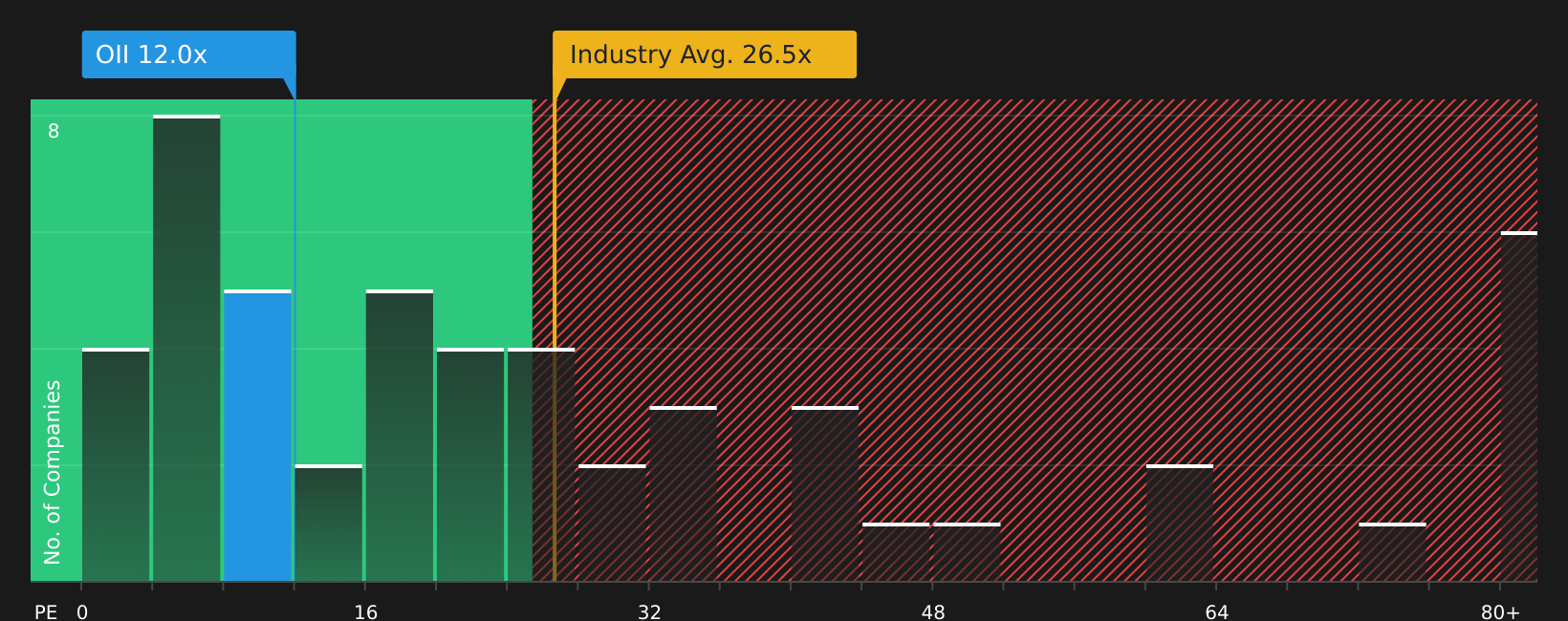

Oceaneering International brings together high quality subsea robotics, long term offshore contracts, and a growing aerospace and defense arm, which together help balance its heavy exposure to cyclical oil and gas spending. Recent earnings growth of 85.8%, high estimated ROE of 30.5%, and a P/E below both the US market and Energy Services industry indicate that the stock may still be priced more like a traditional service contractor than a diversified robotics and defense supplier. At the same time, analysts forecast a sharp earnings decline and the company is leaning more on external borrowing. Together with its execution history, index additions, and active balance sheet reshaping, this creates a company where the headline risks may not tell the full story.

Oceaneering International’s mix of subsea robotics, long term offshore work and aerospace exposure makes the current P/E and earnings outlook look like only half the story, and the 2 key rewards and 2 important warning signs (1 is major!) could show what the market may be missing

Universal Insurance Holdings (UVE)

Overview: Universal Insurance Holdings is an integrated US residential insurer offering homeowners, renters, condo, and related property and liability coverage. It also provides underwriting, risk analysis, claims handling, and reinsurance management, supported by its digital agency Clovered.com and independent agent network.

Operations: Universal Insurance Holdings generates about US$1.6b in revenue from property and casualty insurance in the United States.

Market Cap: US$1.2b

Universal Insurance Holdings attracts attention because it combines high returns on equity, a 12.2% profit margin and a steady dividend with active buybacks and business outside Florida, while trading below some estimates of intrinsic value. At the same time, the company faces pressures from competitive intensity in its core Florida market, reliance on reinsurance pricing, and higher loss and expense ratios, all against a backdrop of weather and regulatory risks. For investors, the tension between recent earnings, technology driven underwriting improvements and these structural risks is a key aspect when evaluating Universal as a small cap insurer.

Universal Insurance Holdings is combining a high ROE, a 12.2% profit margin and ongoing buybacks with real questions around Florida exposure and reinsurance costs, so the 4 key rewards and 2 important warning signs (1 is major!) could be the missing piece investors are not factoring in yet

HCI Group (HCI)

Overview: HCI Group is a Tampa based property and casualty insurer that combines traditional homeowners insurance with its own technology platforms, such as Exzeo, Harmony and ClaimColony, to handle underwriting, policy administration and claims. It also runs reciprocal exchange operations and invests in commercial real estate, giving it several income streams linked to the insurance ecosystem.

Operations: HCI Group generates most of its roughly US$0.9b in revenue from Insurance Operations at about US$841.8m, supported by Exzeo at about US$226.5m, Reciprocal Exchange Operations at about US$81.3m, Real Estate at about US$16.2m and Corporate or Other at about US$24.8m, with about US$263.1m removed as reclassifications or eliminations.

Market Cap: US$2.3b

HCI Group stands out because it pairs high profitability metrics, including a 31.3% net margin and 28.1% ROE, with proprietary tech that management credits for better loss ratios and record recent earnings. At the same time, the stock involves questions around heavy Florida exposure, rising reinsurance costs and how a potential Exzeo IPO could affect its edge in underwriting and claims. Analysts report revenue growth, falling earnings and a P/E well below industry averages alongside buybacks, dividends and index inclusion. Together, these factors present a more complex picture than a simple momentum story. For investors, the question is how these strengths and fault lines line up against the quality filters in this screener and what that might mean for HCI’s future.

HCI Group’s high margins and tech driven underwriting are pulling away from its Florida risk story, and the 3 key rewards and 1 important major warning sign could reveal the twist behind that gap that investors are only starting to question

The three stocks in this article are only a starting point, as the full High-Quality Undiscovered Gems screener on Simply Wall St surfaces 15 more small caps with equally compelling risk reward setups and under followed narratives through the High-Quality Undiscovered Gems screener. Unlock more depth by using Simply Wall St to identify and analyze the exact catalysts, balance sheet traits and earnings drivers discussed here so you can filter for the ideas that best fit your own approach.

Take Control of Your Investment Journey

If Universal Insurance Holdings or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Catch On

New stock stories can move from quiet to breakout quickly, and many slip away before the crowd notices. Scan these fresh ideas while they are still under the radar for now and consider them before they become widely followed.

- Spot fast improving balance sheets and cash flows by running the list of solid balance sheet and fundamentals (47 results) so you are watching financially resilient stocks before momentum really starts to build.

- Target income opportunities with staying power by checking the 9 dividend fortresses and focusing on companies where high yields and business quality go hand in hand.

- Review the 36 power grid technology and infrastructure stocks to find operators that may benefit if grid spending gains fresh momentum as part of the next infrastructure upgrade cycle.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.