Paysign (PAYS) Is Up 67.6% After Strong 2026 Margin Guidance And Revenue Outlook - Has The Bull Case Changed?

Paysign, Inc. PAYS | 0.00 |

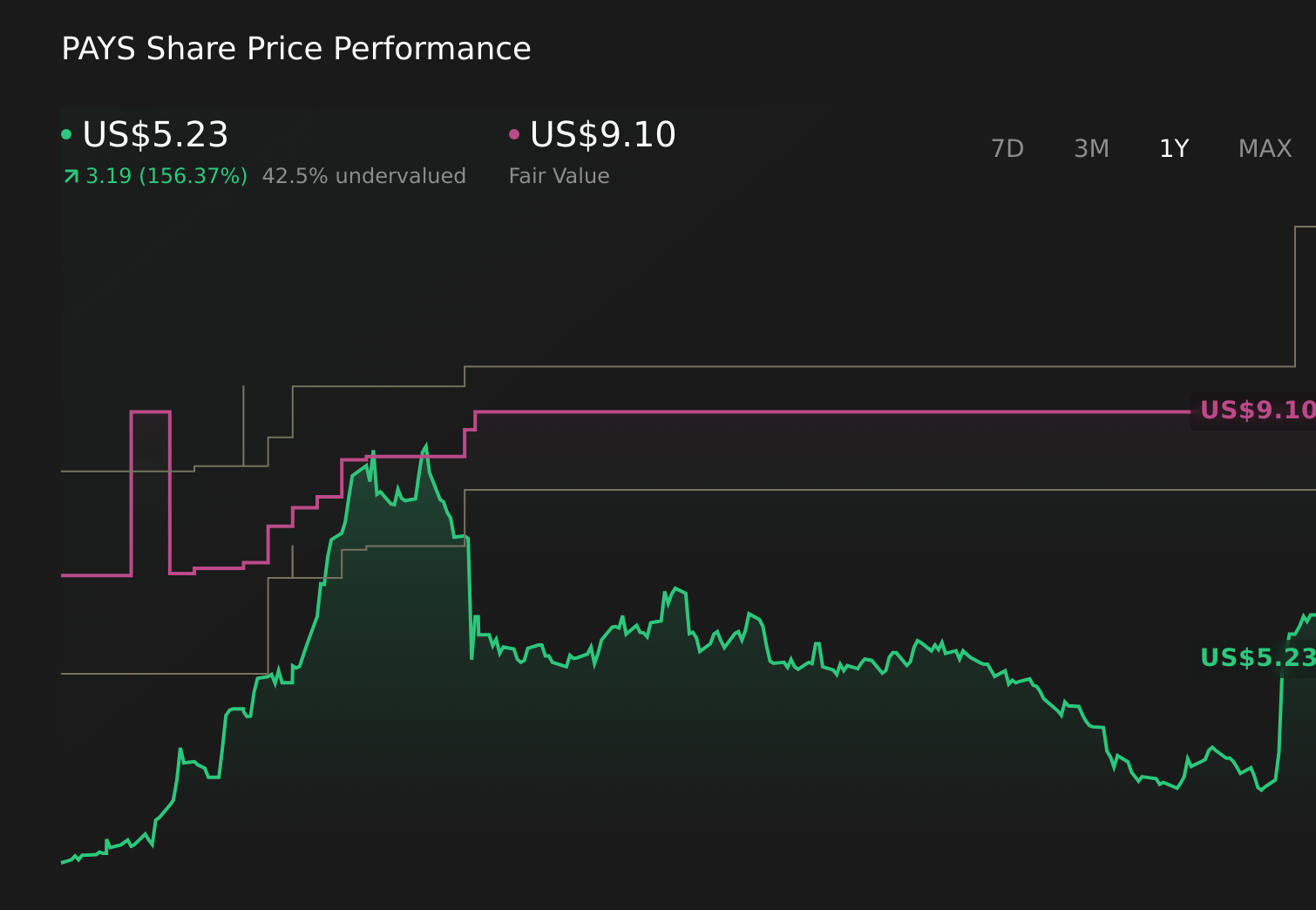

- In March 2026, Paysign, Inc. reported fourth-quarter 2025 revenue of US$22.76 million and full-year 2025 revenue of US$82.03 million, alongside 2026 guidance calling for first-quarter revenue of US$27.0–27.5 million, operating margins of 20–22%, and net margins of 17–19%.

- The company also projected 2026 revenue of US$106.5–110.5 million split roughly evenly between plasma and pharma, with higher gross margins driven by its patient affordability programs and net income guidance of US$13.0–16.0 million, while confirming completion of a modest US$2.0 million share repurchase plan.

- Now we’ll explore how this strong 2026 guidance, particularly the expected margin expansion, reshapes Paysign’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Paysign Investment Narrative Recap

To own Paysign, you have to believe its mix of plasma and pharma payment solutions can keep scaling while margins hold up. The key near term catalyst is execution on the 2026 outlook, particularly the step up in operating and net margins. The biggest risk remains concentration in plasma and pharma reimbursement if volumes or client wins soften. The latest guidance reinforces the margin story but does not remove that concentration risk.

The most relevant recent announcement here is the 2026 guidance itself, which calls for US$106.5–110.5 million in revenue, operating margins of 20–22% and net margins of 17–19%. That guidance leans heavily on higher margin patient affordability programs and a roughly even plasma pharma mix, directly tying the main growth catalyst to the same areas that could magnify any slowdown in client demand or industry volumes.

Yet against this upbeat margin outlook, investors should still be aware of how concentrated Paysign remains in plasma and pharma reimbursement, and how...

Paysign's narrative projects $124.4 million revenue and $15.5 million earnings by 2028. This requires 22.0% yearly revenue growth and a $8.7 million earnings increase from $6.8 million.

Uncover how Paysign's forecasts yield a $9.10 fair value, a 71% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming revenue around US$123.5 million and earnings of US$14.4 million by 2028, and focusing on heavy reliance on plasma and pharma as a key vulnerability, so this new guidance could either ease their concerns or reinforce them depending on how you think those segments will actually perform.

Explore 7 other fair value estimates on Paysign - why the stock might be worth over 2x more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Paysign research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Paysign research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paysign's overall financial health at a glance.

Seeking Other Investments?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.