PDF Solutions (PDFS) Is Down 18.9% After $201 Million Follow-On Offering and Guidance Reaffirmation

PDF Solutions, Inc. PDFS | 0.00 |

- Earlier this month, PDF Solutions completed a significant follow-on equity offering and closed an underwritten public share sale totaling over US$201.01 million, issuing more than 5.25 million common shares at US$44.00 each with a US$1.98 discount per share, alongside reaffirmed 2026 earnings guidance and strong first-quarter results.

- This sizeable capital raise, paired with improved profitability and revenue growth, materially alters PDF Solutions’ funding flexibility and potential path for executing its analytics-focused growth plans.

- We’ll now examine how this sizable follow-on equity raise, and the resulting balance-sheet impact, may reshape PDF Solutions’ investment narrative.

We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

PDF Solutions Investment Narrative Recap

To own PDF Solutions, you need to believe its analytics and orchestration platforms can keep gaining traction with leading chipmakers while maintaining profitability. The recent US$201.0 million follow-on equity raise strengthens the balance sheet and could support those ambitions in the near term, but it also amplifies execution risk around deploying fresh capital effectively and managing dilution, which now looks like the most immediate issue to watch rather than any single customer or region.

The reaffirmed 2026 guidance for 20% annual revenue growth and the swing to a US$4.79 million Q1 2026 net profit, on US$60.13 million of sales, frame this offering in a more constructive light. This profitability improvement may matter for how investors assess the use of new funds, especially with analytics-focused growth plans that depend on continued product adoption and margin progress.

Yet, against that improved outlook, investors should not overlook the risk that higher spending and share count could pressure returns if demand slows or large customers pull back...

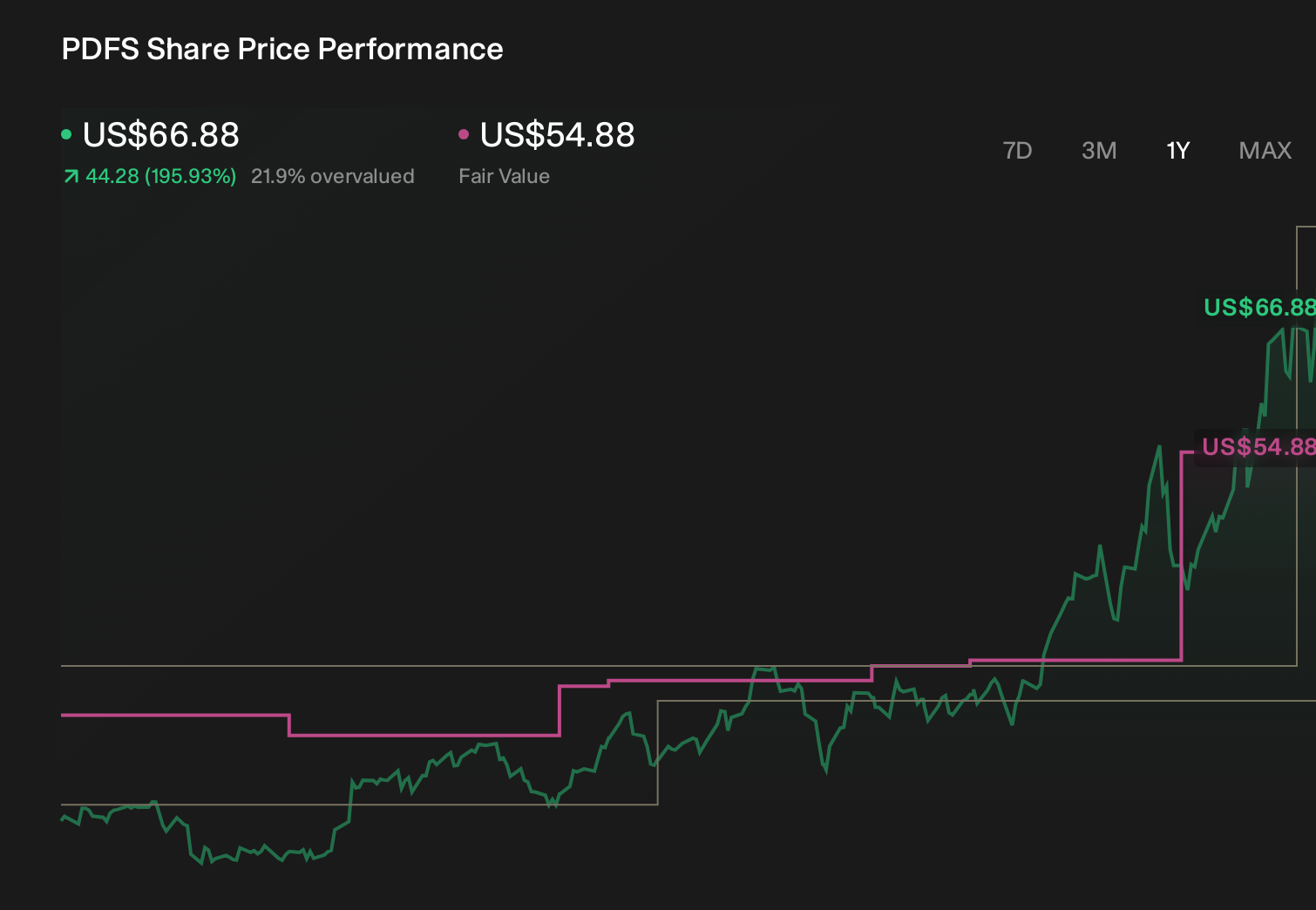

PDF Solutions' narrative projects $383.7 million revenue and $81.7 million earnings by 2029. This requires 18.4% yearly revenue growth and about a $74.5 million earnings increase from $7.2 million today.

Uncover how PDF Solutions' forecasts yield a $54.50 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenue of about US$340 million and earnings of roughly US$46 million by 2028, so after this sizable capital raise and the concentration risk around key customers, it is worth remembering that opinions differ widely and both bullish and cautious views may shift as the impact of this deal becomes clearer.

Explore 5 other fair value estimates on PDF Solutions - why the stock might be worth as much as 22% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your PDF Solutions research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free PDF Solutions research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PDF Solutions' overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.