Penske (PAG) Profit Margin Expands to 3.1%, Reinforcing Bullish Valuation Narratives

Penske Automotive Group, Inc. PAG | 149.34 | +0.12% |

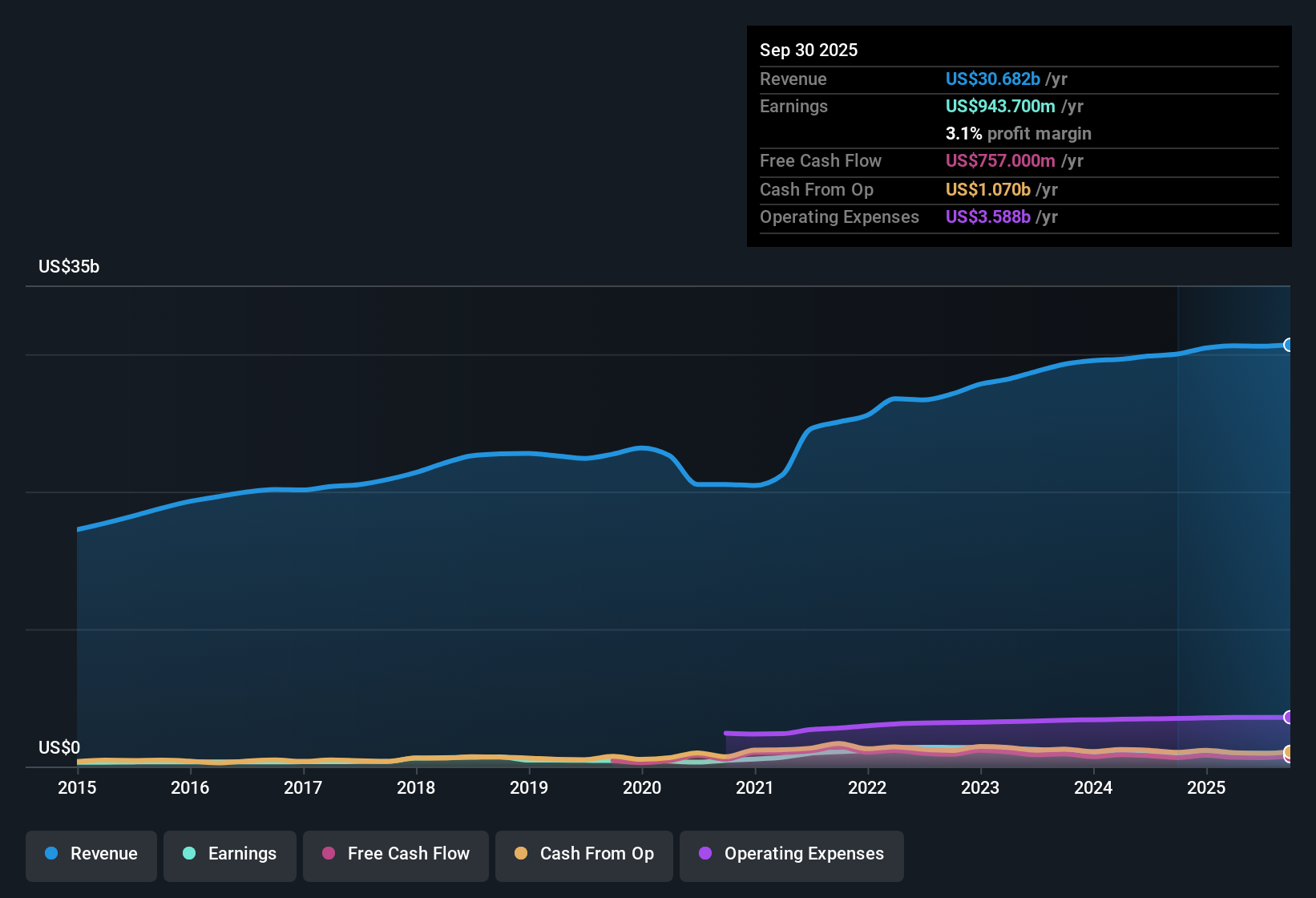

Penske Automotive Group (PAG) reported annual earnings growth of 8.1%, outpacing its five-year average of 2.3% per year, and saw its net profit margin improve from 2.9% to 3.1%. Revenue is projected to grow at 3.8% per year, lagging behind the broader US market’s rate of 10.3%. With shares trading below an estimated fair value of $169.20 and a Price-To-Earnings ratio of 11.4x compared to the industry average of 16.6x, investors are likely to see a mix of solid earnings quality and improving profitability, balanced by moderation in top-line growth and ongoing financial risks.

See our full analysis for Penske Automotive Group.The next step is to see how these recent results compare with the key market narratives investors have been tracking. Let’s break down how the numbers stack up and where the story may get challenged.

Recurring Service Revenue Drives Margin Expansion

- Service and parts revenue grew 7% while gross profit climbed 9%, highlighting recurring, higher-margin income as a key driver of overall profitability.

- Analysts' consensus view emphasizes how this growth in recurring service business, coupled with increased complexity of aging vehicles and higher warranty work, is allowing Penske to support durable profitability and net profit margin improvements.

- Consensus narrative notes that as the average vehicle age rises beyond 6 years in the U.S. and Europe, this trend creates a resilient stream of service income, supporting margins as new vehicle sales moderate.

- While the margin uplift enhances stability, analysts still expect future profit margins to taper to 2.7% from the current 3.1% over the next three years. This will test just how lasting these service tailwinds can be.

- See how analysts believe recurring service growth and margin trends may shape Penske’s long-term trajectory. 📊 Read the full Penske Automotive Group Consensus Narrative.

Premium Brand Focus Bolsters Pricing Power

- Penske’s mix is skewed toward premium and luxury brands, with average sales price rising from $41,000 in 2019 to about $61,000, supporting higher gross profit per vehicle.

- According to the consensus narrative, this focus on higher-end vehicles provides both earnings resilience and margin expansion. However, it also heightens volatility if luxury demand falters.

- Consensus narrative points out that ongoing pricing power and digital investment help offset sector headwinds, but dependency on high-end buyers puts Penske at risk should consumer affordability or sentiment shift, particularly in the U.K.

- Strategic investments in digital initiatives and capital discipline, such as steady dividend growth and share buybacks, reflect management’s intent to deliver stable cash flows and shareholder returns. This reinforces the bullish take on premium positioning.

Valuation Sits Between Fair Value and Peer Group

- Shares currently trade at $162.48, below both the DCF fair value of $169.20 and the analyst consensus target of $179.86, suggesting modest undervaluation against intrinsic and sell-side benchmarks.

- Per the consensus narrative, Penske’s Price-To-Earnings ratio of 11.4x stands lower than the specialty retail industry’s 16.6x average, but in line with direct peers. Analysts see the stock as fairly priced with limited upside barring a positive surprise in execution or sector momentum.

- Consensus view flags that for the stock to close the valuation gap to peer multiples and price target, investors would need confidence in long-term earnings stability even as margins are forecast to compress from 3.1% to 2.7% by 2028.

- This pricing dynamic positions Penske as a value play for those comfortable with moderate growth and ongoing sector headwinds, but leaves less room for disappointment if projected operational risks materialize.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Penske Automotive Group on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you spot a new angle in the results? Share your insight and build your narrative in just a few minutes: Do it your way.

A great starting point for your Penske Automotive Group research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

See What Else Is Out There

Penske’s reliance on recurring service growth and premium brand pricing faces headwinds from forecast margin compression and slower revenue growth compared to the market.

If you’re seeking steadier companies that consistently expand sales and profits year after year, use our stable growth stocks screener (2113 results) to find alternatives built for reliability through any cycle.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.