Peoples Bancorp (PEBO) Could Be 4% Overvalued Following Margin Pressure And Softer Sales

Peoples Bancorp Inc. PEBO | 0.00 |

Recent commentary on Peoples Bancorp (PEBO) focuses on softer sales growth and a declining net interest margin, which together suggest that its expanding loan book is generating less profitable incremental earnings for shareholders.

At a share price of $38.71, Peoples Bancorp has seen its short term momentum build, with a 1 month share price return of 10.16% and a 90 day share price return of 15.00%. This is set against a 1 year total shareholder return of 28.63% and a 3 year total shareholder return of 72.63%, as investors weigh softer margins alongside a stronger recent share price performance.

If you are weighing Peoples Bancorp against other opportunities in the sector, it may be a good time to broaden your search and review the 20 top founder-led companies

After a sharp move in Peoples Bancorp to $38.71, the stock now sits slightly above the average analyst target, yet at a steep discount to some intrinsic value estimates. So where does fair value really look anchored before you factor in the risks?

Most Popular Narrative: 3.7% Overvalued

On the most followed narrative, Peoples Bancorp screens slightly above its fair value estimate of $37.33 at the current $38.71 share price. This puts more weight on how the forecast plays out than on any large valuation gap today.

Healthy pipelines for loan and deposit growth, competitive pricing discipline, and active capital management (including opportunistic share repurchases and a strategic approach to acquisitions) support long-term revenue and book value growth, while taking advantage of regulatory trends that benefit well-capitalized, efficiently run community banks.

Curious what justifies paying slightly above a $37.33 fair value for Peoples Bancorp? The narrative emphasizes compounding revenue, firmer margins, and a lower future earnings multiple than many peers. The focus is on how these three levers interact over time.

Result: Fair Value of $37.33 (OVERVALUED)

However, the Peoples Bancorp narrative could be challenged if credit costs in the leasing portfolio remain elevated or if funding pressures from retail CDs continue to squeeze margins.

Another View: Peoples Bancorp Through a Cash Flow Lens

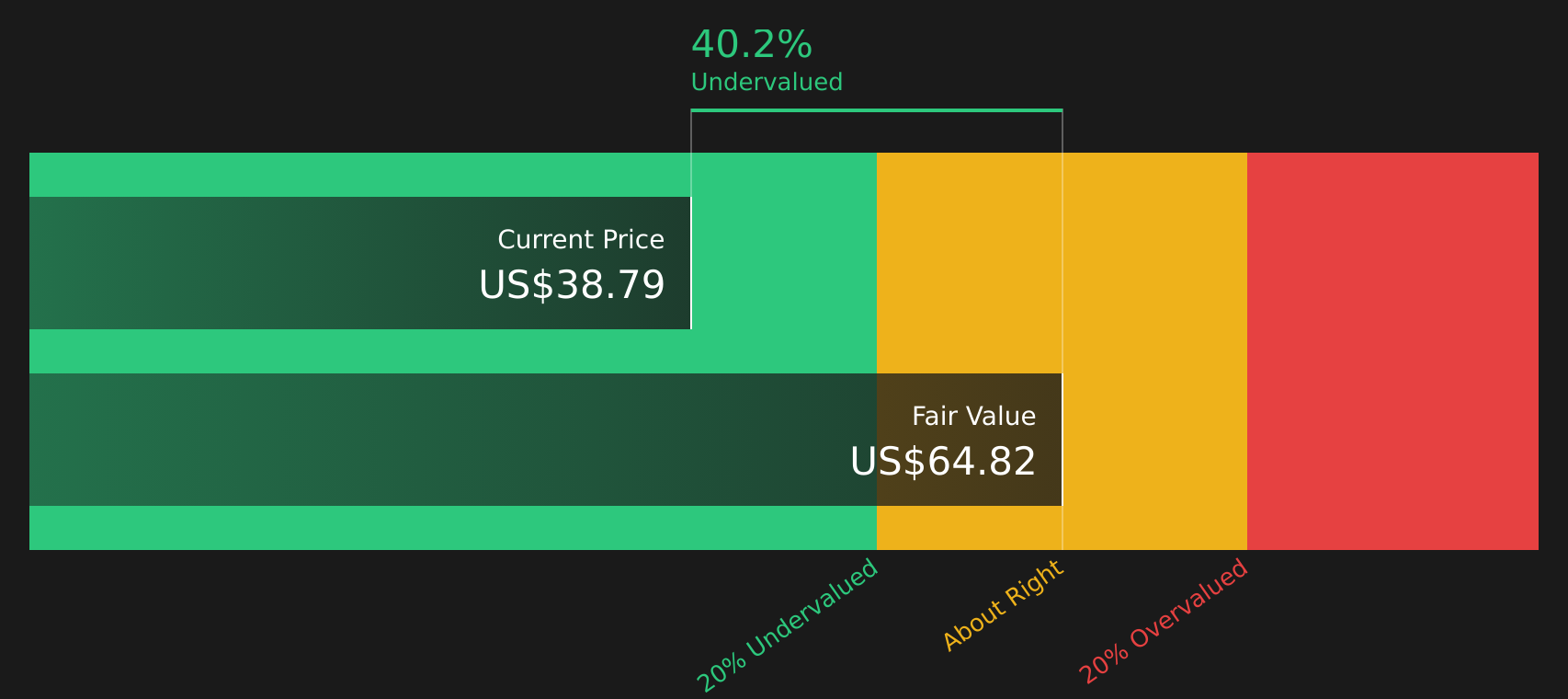

The analyst narrative places Peoples Bancorp near a $37.33 fair value based on earnings and multiples, yet the Simply Wall St DCF model points in a different direction. On that framework, the stock at $38.71 sits well below an estimated future cash flow value of $64.82, which presents a much more generous picture of potential upside. The tension for you is which set of assumptions feels more realistic for a bank with softer margins but ongoing earnings growth forecasts.

To understand how those assumptions translate into that higher figure, it helps to walk through the moving parts in the SWS DCF model rather than just taking the headline number at face value. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Peoples Bancorp for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the split views on Peoples Bancorp have left you on the fence, it can be helpful to act promptly and review the numbers yourself, comparing them with the positives that investors are focused on using the 3 key rewards

Looking for more investment ideas beyond Peoples Bancorp?

If the mixed signals around Peoples Bancorp have sharpened your focus, use that momentum and line up a few other candidates worth your attention right now.

- Scan for potential value opportunities that pair quality with price using the 44 high quality undervalued stocks

- Prioritize income by zeroing in on companies designed to keep paying you, starting with the 7 dividend fortresses

- Focus on resilience first and seek out companies with steadier risk profiles through the 73 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.