Philip Morris International (NYSE:PM) Valuation After FDA Progress On ZYN Modified Risk Review

Philip Morris International Inc. PM | 158.10 | +0.49% |

Why the FDA’s ZYN review matters for Philip Morris International stock

Philip Morris International (PM) has moved into focus after presenting scientific evidence to the FDA in support of classifying its ZYN nicotine pouches as a Modified Risk Tobacco Product. This is a regulatory step with meaningful implications for its smoke free portfolio.

That FDA review comes at a time when momentum in Philip Morris International’s shares has been positive, with a 9.13% 1 month share price return and a 17.32% 3 month share price return, supporting a 39.52% 1 year total shareholder return.

If this kind of regulatory driven story has your attention, it may be a good moment to broaden your research and look at pharma stocks with solid dividends as potential income ideas beyond tobacco.

With Philip Morris International shares having risen strongly over the past year and trading only about 3% below the average analyst price target, the key question is whether the roughly 20% intrinsic discount suggests undervaluation or whether the market already reflects expectations for future growth.

Most Popular Narrative: 3.9% Undervalued

Philip Morris International’s most followed valuation story pegs fair value at $182.94 versus a last close of $175.76, putting a modest gap between price and narrative.

The accelerating global adoption of smoke-free alternatives, driven by increasing health awareness and regulatory moves away from combustibles, is fueling strong double-digit volume and margin growth in PMI's IQOS, ZYN, and VEEV platforms. This secular shift enables the company to capture new consumer segments, expand its addressable market, and structurally boost net revenues and operating margins over time.

Curious how an earnings path built on smoke free products, richer margins, and a firm discount rate stacks up to today’s price? The full narrative lays out the revenue mix shift, profitability assumptions, and future earnings multiple that underpin that $182.94 figure without the market necessarily agreeing yet.

Result: Fair Value of $182.94 (UNDERVALUED)

However, there are still meaningful watch points, including tighter nicotine regulation that could affect smoke-free growth, as well as currency swings that impact reported earnings and margins.

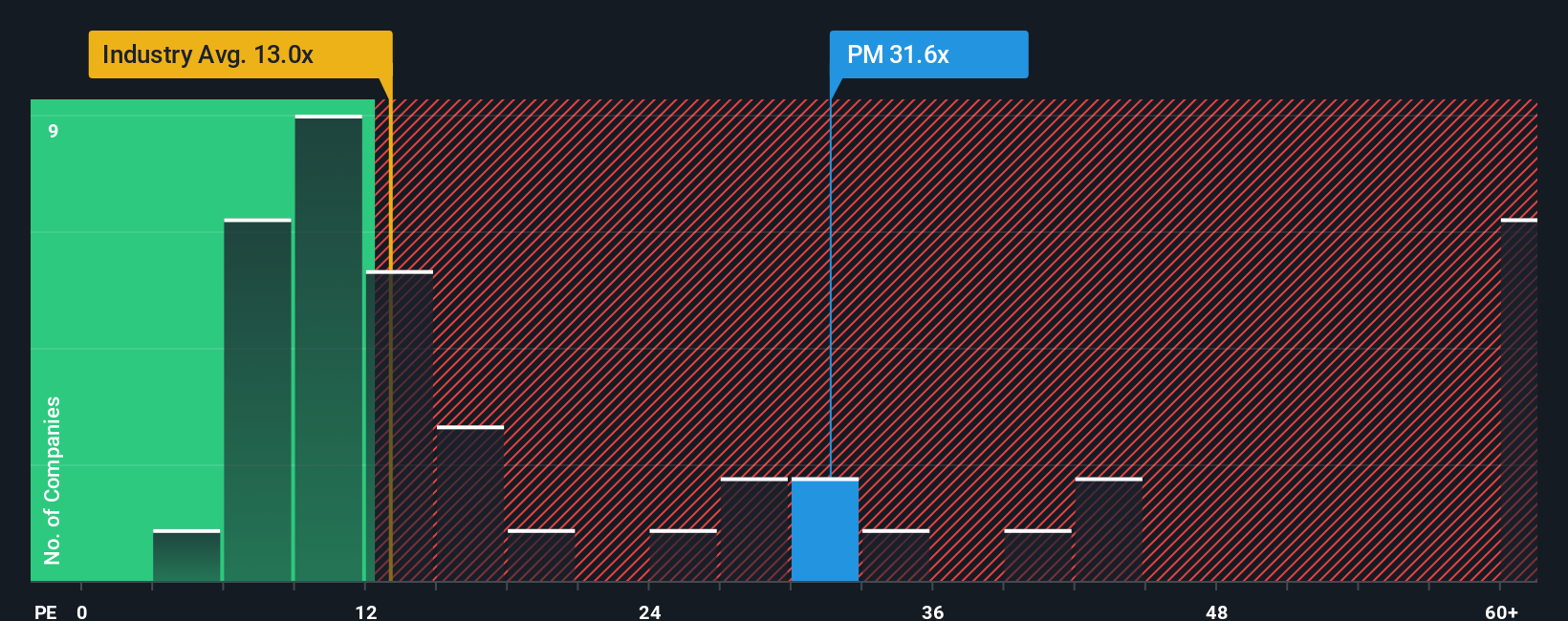

Another View: Rich P/E Raises Different Questions

Our DCF work tags Philip Morris International as undervalued, yet the current P/E of 31.8x is higher than the fair ratio of 26.3x, the global tobacco average of 13.2x, and the 25.6x peer average. That premium can look like confidence or valuation risk. Which side do you think it represents?

Build Your Own Philip Morris International Narrative

If the story here does not quite match your view, or you would rather test the assumptions yourself, you can build a custom thesis in minutes: Do it your way.

A great starting point for your Philip Morris International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready to hunt for more investment ideas?

If Philip Morris International has sharpened your thinking, do not stop here. Use the Screener to quickly surface fresh ideas that fit your own checklist.

- Target potential value with these 884 undervalued stocks based on cash flows that highlight companies the market may be pricing conservatively relative to their cash flows.

- Zero in on income opportunities through these 13 dividend stocks with yields > 3% that focus on businesses offering yields above 3%.

- Chase higher growth potential with these 23 AI penny stocks that center on companies developing or deploying artificial intelligence in meaningful ways.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.