Photronics (PLAB) Is Down 6.0% After Russell Index Additions and Insider Selling - What's Changed

Photronics, Inc. PLAB | 0.00 |

- In late June 2026, index provider FTSE Russell added Photronics, Inc. (NasdaqGS: PLAB) to multiple Russell growth and small-cap benchmarks, broadening its institutional index exposure.

- This wave of index inclusions coincides with weaker recent earnings and increased insider selling, creating a complex backdrop for assessing Photronics’ positioning.

- We’ll now examine how these index additions, alongside insider selling, reshape Photronics’ existing investment narrative and risk-reward profile.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Photronics Investment Narrative Recap

To own Photronics, you need to believe that its photomask investments in advanced IC and high-end display capacity will translate into durable demand despite cyclical swings. The broad Russell index additions expand passive ownership, but do not materially change the near term earnings risk tied to IC softness, limited backlog visibility, and volatile design activity in Asia.

The most relevant recent development is the fiscal Q2 2026 miss on revenue and EPS, which contributed to a roughly 10% pullback ahead of the index inclusions. That earnings shortfall underlines how quickly orders can shift when fab utilization, memory constraints, or geopolitical issues disrupt design releases, keeping short term results sensitive even as Photronics builds out capacity for AMOLED and advanced-node opportunities.

Yet behind the index buzz and share price moves, the combination of heavy capital spending and uncertain IC demand is something investors should be aware of as they consider...

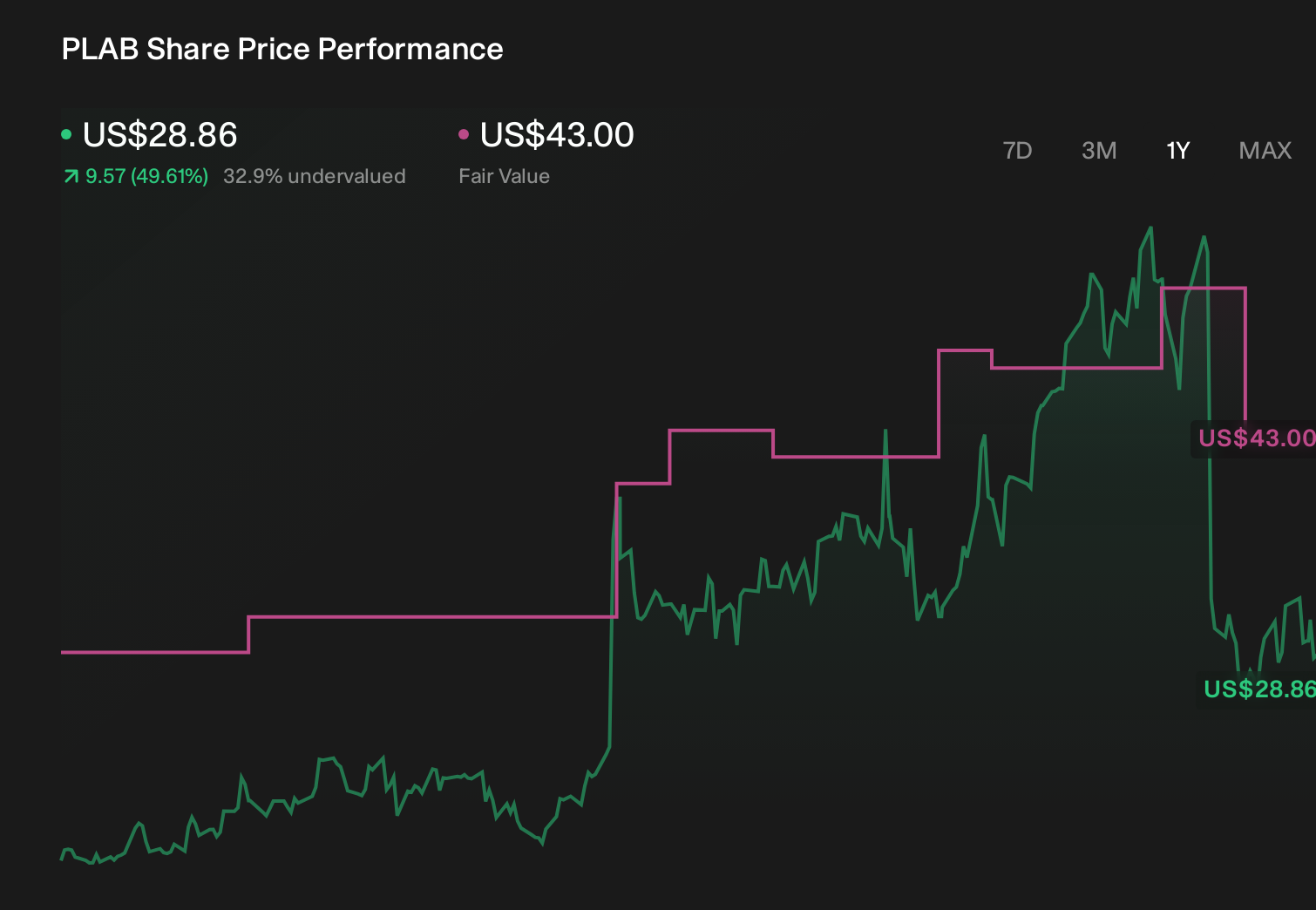

Photronics' narrative projects $930.0 million revenue and $81.2 million earnings by 2029. This requires 2.6% yearly revenue growth and a $77.9 million earnings decrease from $159.1 million today.

Uncover how Photronics' forecasts yield a $43.00 fair value, a 49% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community currently see fair value for Photronics between US$21.84 and US$43, reflecting a wide spread of individual models. Against that backdrop, the recent earnings miss and ongoing geopolitical and IC demand risks give you multiple angles to weigh before forming your own view on the company’s performance and resilience.

Explore 5 other fair value estimates on Photronics - why the stock might be worth 24% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Photronics research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.