Polaris (PII) Joins Russell Growth Indices, Is The Stock Still Cheap?

Polaris Inc. PII | 0.00 |

Polaris reclassified across Russell growth and value indices

Polaris (PII) just went through a broad reclassification across the Russell index family, leaving several value benchmarks and joining multiple growth oriented indices. This shift can reshape how many investors gain exposure to the stock.

Polaris shares recently traded at US$64.33, with a 1 day share price return of 1.92% and a 90 day share price return of 19.71%, while the 1 year total shareholder return of 46.34% contrasts with weaker 3 and 5 year outcomes. This suggests near term momentum has improved even as longer term returns remain under pressure.

With index trackers adjusting around this growth reclassification, it can be a good moment to see which other stocks are catching investor attention through the 20 top founder-led companies

For Polaris, this index swing sits at the intersection of a modestly growing revenue base, a recent net loss, and sharp short term share gains. Are investors now paying a growth style price for that mix of fundamentals?

Most Popular Narrative: 5.4% Undervalued

On the most followed narrative, Polaris has a fair value of $68.00 versus the last close at $64.33, putting the stock on a modest implied discount and framing how growth expectations, margins and risk are being balanced.

Polaris is focused on a strategic approach to mitigate the impact of tariffs through supply chain adjustments and cost control initiatives, which could potentially preserve net margins and improve earnings over time.

Polaris has mobilized a tariff mitigation strategy to offset expected $320-$370 million gross tariff costs, which aims to reduce the financial impact and improve earnings by maintaining operational efficiencies and preserving liquidity.

Curious what has to happen for Polaris to justify that fair value label? Revenue, earnings and margins are all wired into this story, along with a specific future earnings multiple that underpins the $68.00 figure, but the exact mix may surprise you.

Result: Fair Value of $68.00 (UNDERVALUED)

However, the Polaris narrative still faces pressure from uncertain tariff outcomes and weaker demand conditions, either of which could quickly change how analysts view the stock.

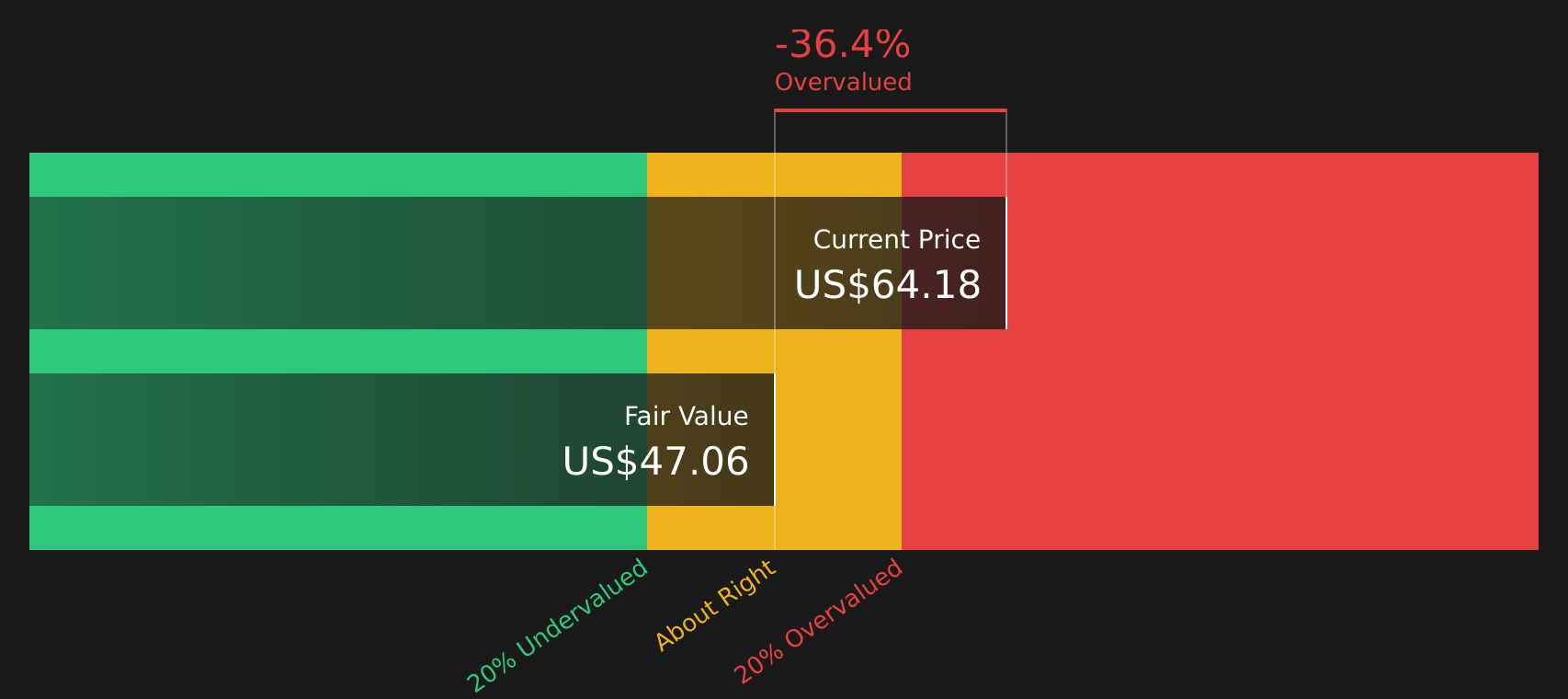

Another View on Polaris Using the SWS DCF Model

Those fair value narratives put Polaris at $68.00, but the SWS DCF model tells a different story, with an estimate of $46.90 for future cash flow value against the current $64.33 share price. That points to Polaris trading well above that cash flow based mark. The key question is which anchor you consider more relevant.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Polaris for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this combination of signals on Polaris seems unclear, that is the point. Use the data to pressure test your own view with the 2 key rewards and 2 important warning signs.

Looking for more Polaris investment ideas?

Before moving on from Polaris, use this moment of fresh insight to broaden your watchlist with a few focused stock idea sets built from clear, transparent criteria.

- Target resilient cash generators by scanning companies that pass a solid balance sheet and fundamentals stocks screener (47 results) to see which businesses pair financial strength with consistent fundamentals.

- Hunt for potential mispricings by checking the screener containing 18 high quality undiscovered gems and spot quality stocks that many investors may be overlooking right now.

- Strengthen your downside protection by reviewing 74 resilient stocks with low risk scores so you are not the one chasing volatility while others quietly build steadier positions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.