Polestar Automotive Holding UK (PSNY) Expands In Finland, Is The Stock Slightly Overvalued?

Polestar Automotive Holding UK PLC Sponsored ADR Class A PSNY | 0.00 |

Polestar Automotive Holding UK (PSNY) has drawn fresh attention after reporting second quarter 2026 sales volumes, alongside news of an expanded showroom partnership in Finland's largest metropolitan area.

Despite the new Helsinki showroom plan and steady first half retail volumes, Polestar Automotive Holding UK’s share price return has weakened, with the stock down 11.54% over the past week and year to date momentum still soft. The 1 year total shareholder return has fallen 46.40%, and the 3 year total shareholder return is down 87.03%.

If this kind of operational update has you thinking about where else growth stories could emerge, it may be worth scanning 18 top founder-led companies

Bulls see Polestar Automotive Holding UK building a broader EV footprint, while bears point to heavy losses and sharp share price declines. Do the current numbers suggest a recovery story or a stock still priced for caution?

Most Popular Narrative: 2.9% Overvalued

Polestar Automotive Holding UK’s most followed narrative pegs fair value at $17.50, slightly below the last close of $18.01. This frames the stock as modestly ahead of that model.

The analysts have a consensus price target of $17.5 for Polestar Automotive Holding UK based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $20.0, and the most bearish reporting a price target of just $15.0.

What sits underneath that $17.50 figure is a tight set of assumptions around rapid revenue expansion, a turn in margins, and a future earnings multiple that has to hold. The gap between today’s losses and those projected profits is wide. The core issue is how much growth and profitability this narrative requires to bridge that distance.

Result: Fair Value of $17.50 (OVERVALUED)

However, there are still clear risks to the Polestar Automotive Holding UK narrative, including ongoing heavy cash burn, reliance on external funding, and intense EV competition in key markets.

Another View: Polestar Automotive Holding UK Through the Sales Multiple Lens

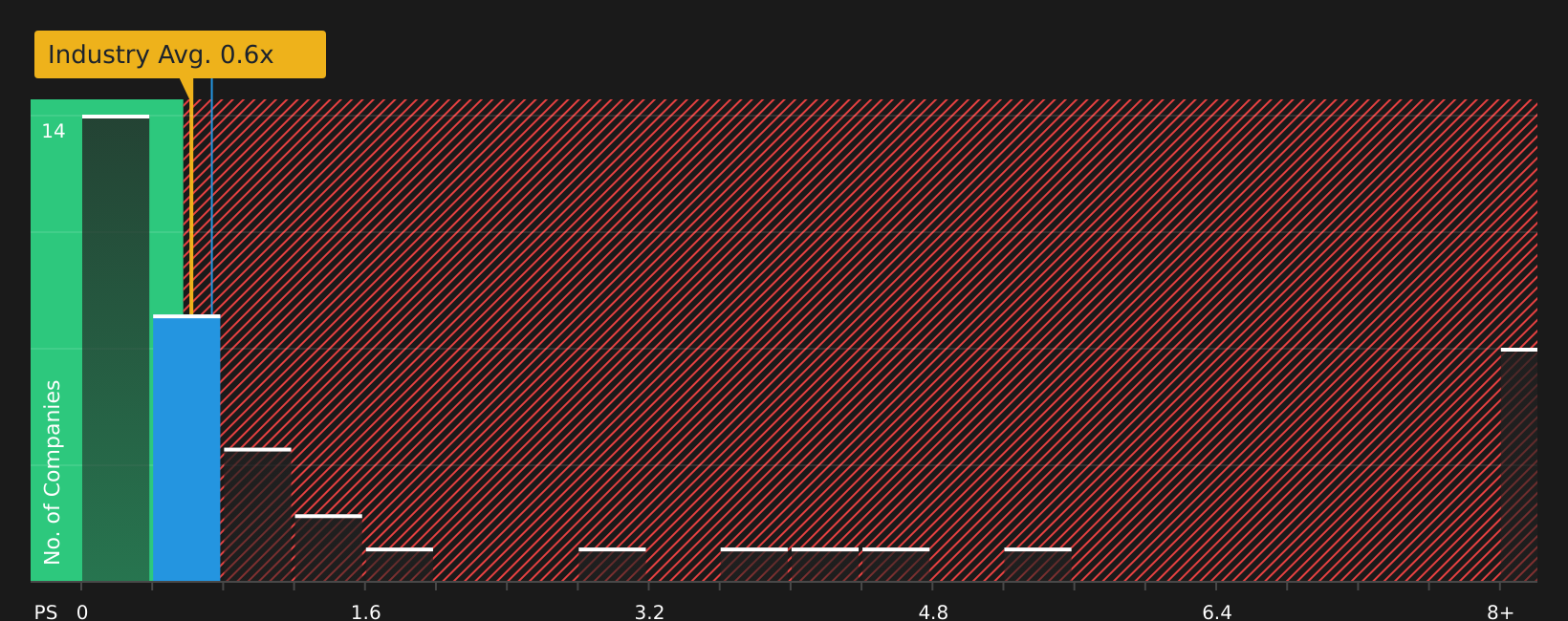

The analyst narrative frames Polestar Automotive Holding UK as 2.9% overvalued at $17.50, yet its current P/S ratio of 0.9x sits below an estimated fair ratio of 1.6x and above both the US Auto industry average of 0.6x and a 0.7x peer average. That mix of discount to fair ratio but premium to sector and peers points to a tug of war between perceived upside and valuation risk. Which side of that tug do you think reflects reality?

Next Steps

With sentiment around Polestar Automotive Holding UK clearly divided, it makes sense to move quickly, review the underlying data yourself, and weigh both sides of the story using the 1 key reward and 3 important warning signs

Looking for more investment ideas beyond Polestar Automotive Holding UK?

If Polestar Automotive Holding UK has sharpened your focus on where capital works hardest, it is worth widening your search to other structured investment ideas on Simply Wall St.

- Target stability and lower volatility by reviewing companies filtered through the 80 resilient stocks with low risk scores

- Hunt for potential mispriced opportunities by scanning the 46 high quality undervalued stocks

- Zero in on strong fundamentals and healthier balance sheets using the solid balance sheet and fundamentals stocks screener (47 results)

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.