Polestar Automotive Holding UK (PSNY) Looks Fairly Valued As Selloff Puts Fundamentals Back In Focus

Polestar Automotive Holding UK PLC Sponsored ADR Class A PSNY | 0.00 |

Polestar Automotive Holding UK (PSNY) has drawn investor attention after a recent pullback, with the stock down 8.1% over the past day and 13.2% over the past week. This has sharpened focus on its underlying fundamentals.

Zooming out, Polestar Automotive Holding UK's recent selloff builds on earlier weakness, with the share price down over the year despite a small positive 90 day share price return and a steep 1 year total shareholder return decline of 47.66%.

If you are comparing Polestar with other opportunities in the electric and future mobility space, this could be a useful moment to scan for 29 robotics and automation stocks.

With Polestar Automotive Holding UK now trading close to the average analyst price target and carrying a low value score, investors have to ask: is the recent weakness setting up a mispriced opportunity, or is the market already factoring in future growth?

Most Popular Narrative: 40% Undervalued

At a last close of $17.43 versus a narrative fair value of $17.50, Polestar Automotive Holding UK is framed as modestly mispriced, with analysts focusing heavily on the path from fast growing revenue to potential future earnings.

Persistent high cash burn, reliance on external funding, and a lack of clear path to sustainable profitability raise the risk of further shareholder dilution through equity issuance, potentially depressing EPS and constraining future investment. Polestar's dependence on global supply chains and international manufacturing for critical components exposes the company to geopolitical risks, supply disruptions, and potentially higher compliance costs, which could erode margins and impact earnings stability.

Want to see what keeps this Polestar Automotive Holding UK story alive despite losses and dilution? The narrative leans on rapid revenue expansion, margin repair, and a future earnings multiple that needs tight execution to hold up. Curious how those moving parts connect to that fair value line in the sand?

Result: Fair Value of $17.50 (UNDERVALUED)

However, Polestar Automotive Holding UK still faces high cash burn and dependence on external funding. Intense EV competition could pressure margins and challenge the earnings narrative investors are watching.

Another View on Polestar Automotive Holding UK

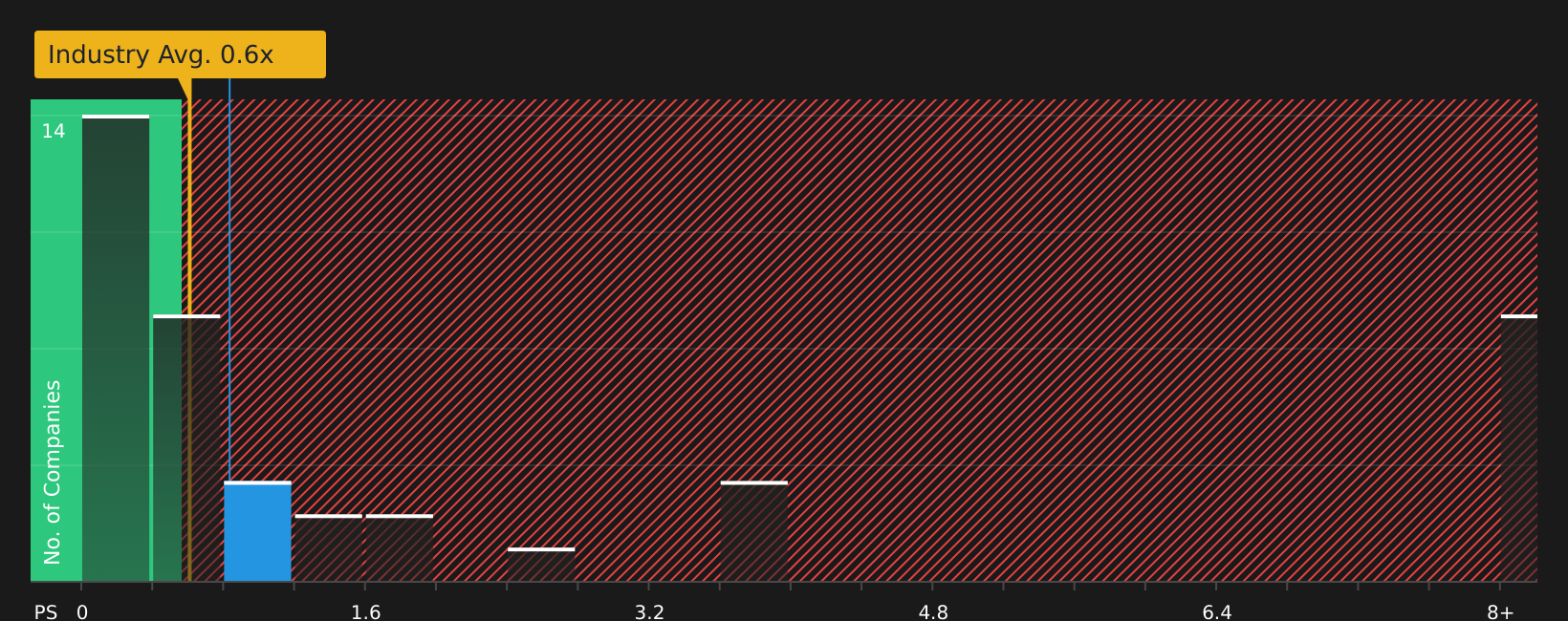

The fair value narrative for Polestar Automotive Holding UK points to a modest undervaluation, but the market is telling a different story. On a P/S of 0.8x versus 0.6x for the wider US Auto industry and 0.8x for peers, the stock screens as expensive, even though the fair ratio is 1.7x. That gap could indicate additional downside risk if sentiment shifts, or potential upside if the market moves toward that fair ratio.

Next Steps

If the mixed tone around Polestar Automotive Holding UK leaves you unsure, consider acting while sentiment is still forming by reviewing the 1 key reward and 3 important warning signs

Looking for more investment ideas beyond Polestar Automotive Holding UK?

If Polestar Automotive Holding UK has sharpened your focus on where risk and reward line up, do not stop here. Broaden your watchlist while opportunities are still on the table using focused stock screeners.

- Target potential value opportunities by scanning companies that appear mispriced on fundamentals with the 44 high quality undervalued stocks.

- Secure a steadier portfolio foundation by reviewing stocks identified as 71 resilient stocks with low risk scores.

- Spot potential up-and-comers before wider attention arrives by checking the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.