Powell Industries (POWL) Lands $400 Million Data Center Order On Mixed Earnings But Is It A Bargain

Powell Industries, Inc. POWL | 0.00 |

Powell Industries (POWL) is back in focus after mixed earnings that combined year-on-year revenue growth and an earnings miss with a historic data center equipment order worth more than $400 million.

The mixed earnings and mega data center win have come after a sharp run in Powell Industries, with a 1-year total shareholder return of 233.8% and a year-to-date share price return of 99.35%. However, the 30-day share price return is down 20.53%, suggesting some momentum has cooled even as investors reassess growth potential and execution risks.

If data center demand has your attention, it can be useful to see what else is benefiting from similar themes, starting with the 34 power grid technology and infrastructure stocks

Bulls point to Powell Industries’ mega data center win and long run of strong total returns, while bears focus on the earnings miss and recent pullback. Which case lines up better with where the stock trades today?

Most Popular Powell Industries Narrative: 34.9% Undervalued

At a last close of $234.25 versus a narrative fair value of $360.00, Powell Industries is framed as materially undervalued in the most followed storyline on the stock, which leans heavily on earnings power and higher future valuation multiples.

The multi year build out of U.S. LNG export facilities and related natural gas infrastructure is contributing to a pipeline of large, complex projects, supporting backlog stability, higher plant utilization and stronger gross margins.

Strategic capacity expansions in Houston and ongoing productivity investments are increasing throughput and manufacturing leverage. This may enable Powell to convert its record backlog more efficiently and support higher operating margins over time.

Want to see what sits behind that backlog story? The narrative leans on stronger margins, faster revenue expansion and a premium profit multiple to reach that fair value. The exact mix and timing of those assumptions is where it gets interesting.

Result: Fair Value of $360.00 (UNDERVALUED)

However, Powell Industries still faces execution risk if LNG related projects or grid and data center spending slow, and if recent margin levels prove hard to sustain.

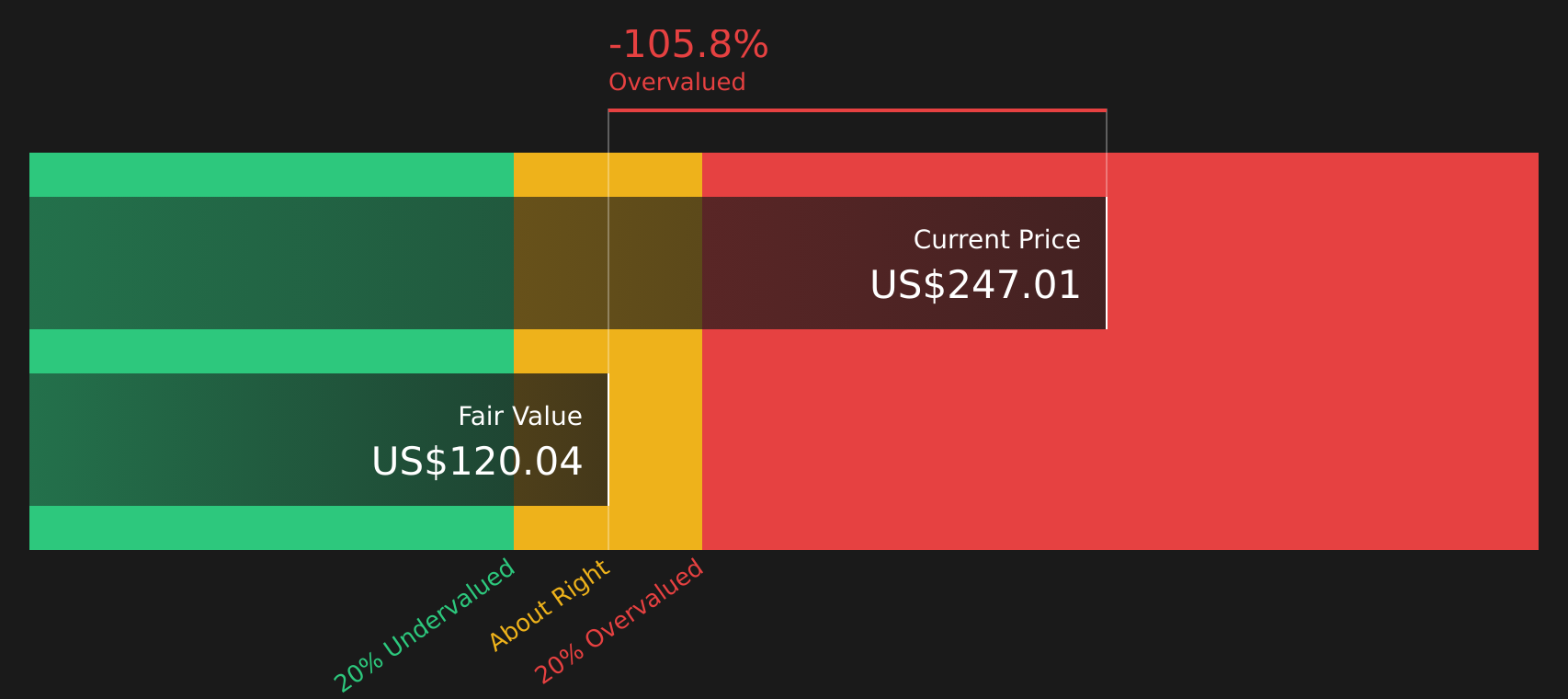

Another View on Powell Industries Valuation

While the most followed Powell Industries narrative leans on higher future earnings and a richer P/E multiple to argue the stock is 34.9% undervalued at a fair value of $360.00, the SWS DCF model points the other way and flags POWL as expensive at $234.25 versus an estimated future cash flow value of $120.27.

The gap between a bullish multiple based fair value and an overvalued DCF outcome largely comes down to how confident you are that forecast growth, margins and reinvestment can translate into long term cash flows. Which framework do you trust more when real money is on the line?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Powell Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With Powell Industries throwing up both risks and rewards in the current narratives, it makes sense to look through the numbers yourself and decide how the story stacks up for your portfolio. If you want a single place to weigh both sides quickly, start with the 3 key rewards and 1 important warning sign.

Looking for more Powell Industries style investment ideas?

If Powell Industries has sharpened your focus on quality and risk, do not stop here. Use the Simply Wall Street Screener to uncover other targeted opportunities before others get there.

- Target dependable compounding by checking out 8 dividend fortresses that focus on income strength with higher yields.

- Hunt for potential bargains by reviewing screener containing 20 high quality undiscovered gems that pair strong fundamentals with lower market attention.

- Prioritize capital protection by starting with 79 resilient stocks with low risk scores that concentrate on resilience and lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.