Prestige Deal For Stampede Culinary Partners Reshapes Earnings And Valuation Potential

Prestige Consumer Healthcare Inc PBH | 52.48 | -9.02% |

- Prestige Consumer Healthcare (NYSE:PBH) has agreed to acquire Stampede Culinary Partners for $662.5 million.

- The company expects the deal to contribute meaningfully to EBITDA and future earnings once integrated.

- The transaction adds a new business line that management sees as an additional driver of operational earnings.

For investors tracking NYSE:PBH, the acquisition comes as the stock trades around $65.55, with a 7.1% return year to date and 46.7% over five years. The shares are still showing a 25.0% decline over the past year, so this move may draw attention from investors watching how management is using capital to reshape the business mix.

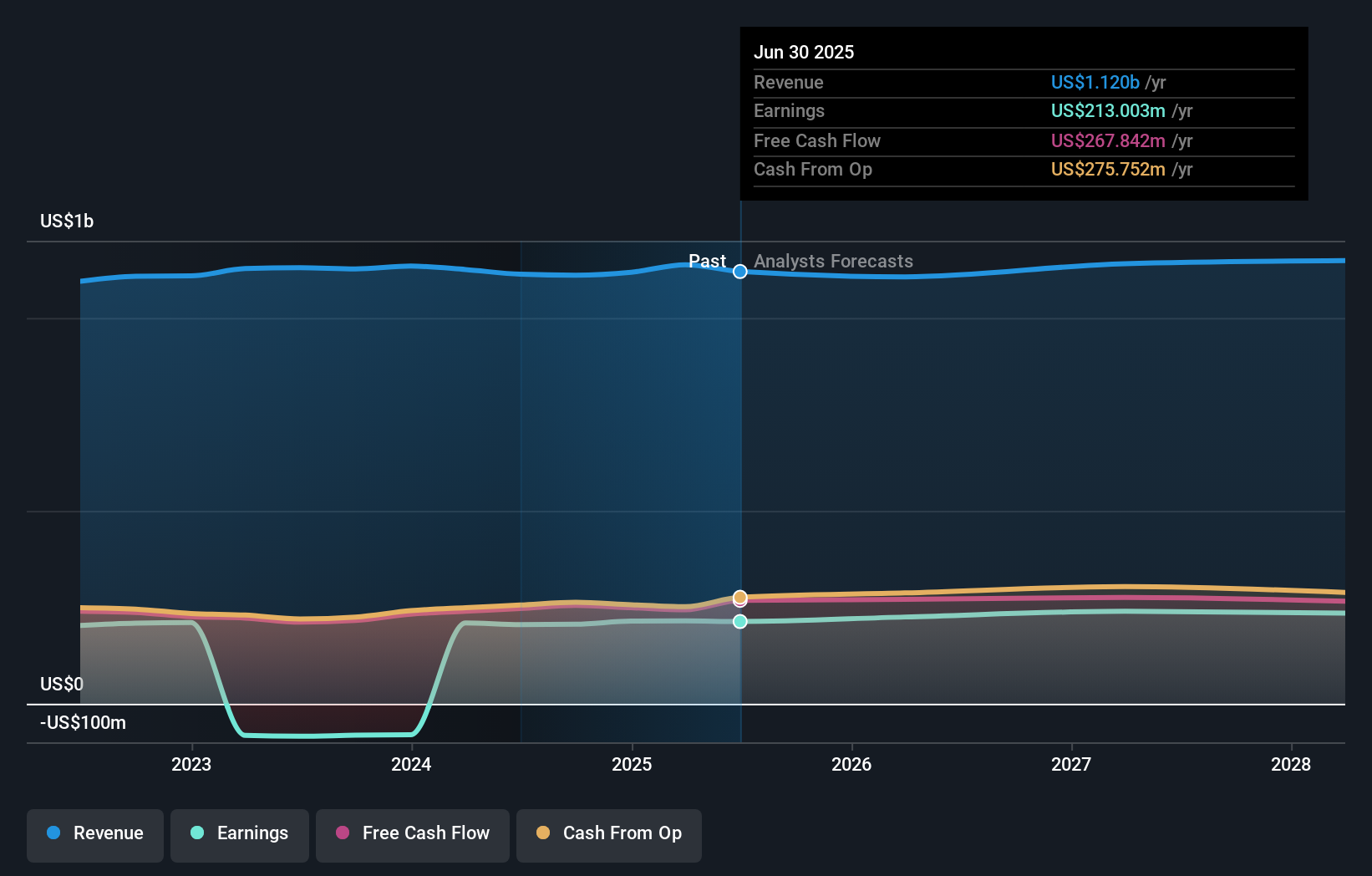

The headline message from Prestige Consumer Healthcare is that Stampede Culinary Partners is expected to materially contribute to EBITDA and earnings per share as efficiencies are realized over time. For investors, the key questions now revolve around integration progress, actual margin impact and how this new earnings stream fits alongside the company’s existing healthcare brands.

Stay updated on the most important news stories for Prestige Consumer Healthcare by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Prestige Consumer Healthcare.

Quick Assessment

- ✅ Price vs Analyst Target: At US$65.55 versus a consensus target of US$77.83, PBH trades about 16% below analyst expectations.

- ✅ Simply Wall St Valuation: Shares are flagged as undervalued, trading around 49.3% below an estimated fair value.

- ✅ Recent Momentum: The 30 day return of roughly 4.4% suggests the market has been slightly more positive recently.

Check out Simply Wall St's in depth valuation analysis for Prestige Consumer Healthcare.

Key Considerations

- 📊 The US$662.5m Stampede Culinary Partners deal adds a new earnings stream that could change how you think about PBH beyond its core OTC healthcare brands.

- 📊 Watch integration progress, EBITDA contribution versus guidance, P/E relative to the industry average of about 21, and any updates on debt used to fund the purchase.

- ⚠️ The company already carries a high level of debt, so investors may want to monitor leverage, interest costs and management’s plans for balance sheet discipline after the acquisition.

Dig Deeper

For the full picture including more risks and rewards, check out the complete Prestige Consumer Healthcare analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.