Privia Health Group (PRVA) Stock Could Be 24.7% Undervalued After Strong Growth

Privia Health Group, Inc. PRVA | 0.00 |

Privia Health Group (PRVA) has drawn increased attention after reporting year over year revenue growth of 25.78% and net profit growth of 27.39%, alongside higher institutional ownership and a favorable technical signal.

At a share price of $23.67, Privia Health Group has a 90 day share price return of 11.44%, while the 1 year total shareholder return of 8.33% contrasts with a 3 year total shareholder return decline of 2.83% and a 5 year total shareholder return decline of 48.59%. This suggests near term momentum has picked up even as longer term holders have seen mixed results.

If Privia Health Group’s recent move has your attention, this could be a good moment to see what else is setting up in healthcare, including 40 healthcare AI stocks.

With Privia Health Group trading at $23.67 alongside a P/E of 133.51 and an indicated discount to some intrinsic and analyst estimates, the key question is whether investors are still getting in early or if future growth is already priced in.

Most Popular Narrative: 24.7% Undervalued

On the most followed narrative, Privia Health Group’s fair value sits at $31.42 against a last close of $23.67. This puts the focus on what is driving that gap rather than the recent share price bounce.

Continued investment in proprietary technology and AI-driven workflow automation increases operational efficiency, leading to reduced administrative costs and improved provider productivity, this is already contributing to rising EBITDA margins and is expected to further enhance net margins over time.

Want to see what sits behind that margin story, the growth in revenue, and the earnings profile that underpins this valuation? The narrative leans heavily on accelerating earnings, firmer profitability, and a future valuation multiple that has to compress, yet still stay well above the broader healthcare sector. Curious which specific revenue path, margin step up, and earnings level have been plugged in to justify that outcome?

Result: Fair Value of $31.42 (UNDERVALUED)

However, Privia Health Group still carries clear risks, including pressure from higher healthcare labor costs and tighter contract terms if insurer and hospital consolidation accelerates.

Another View on Privia Health Group’s Valuation

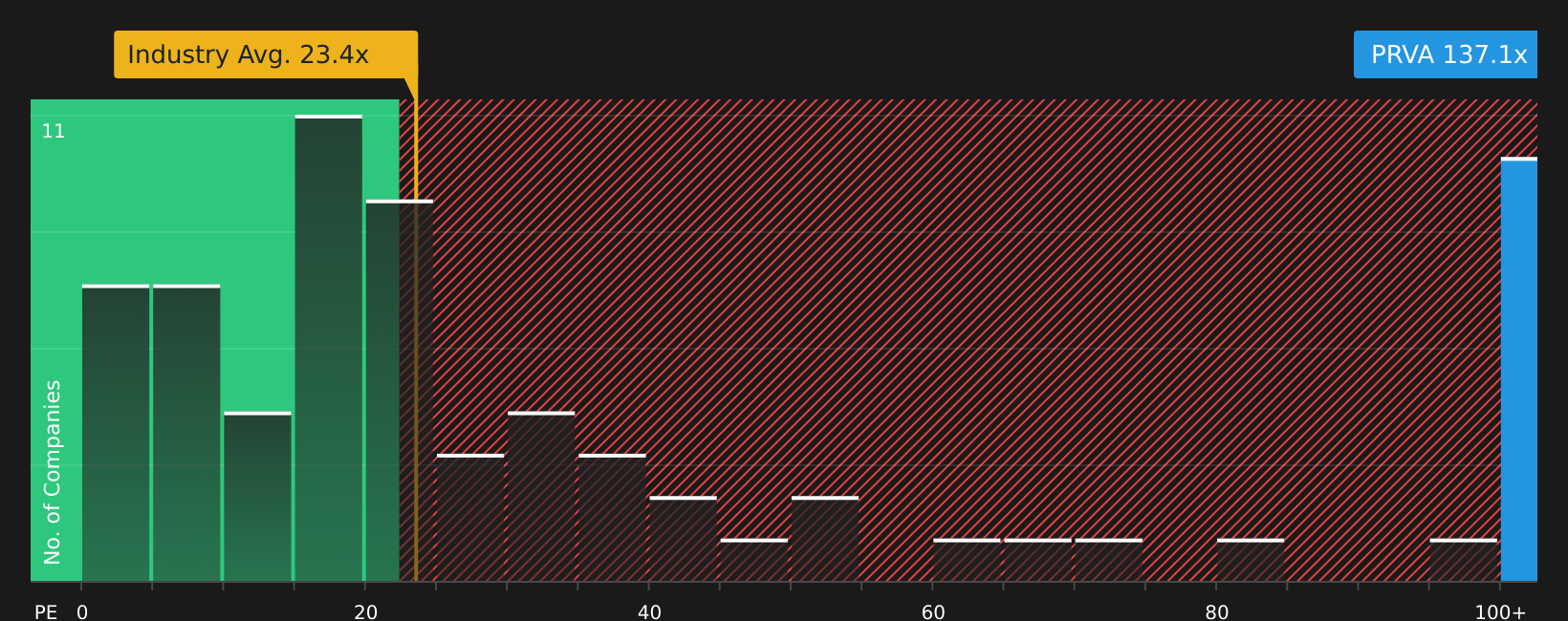

While the SWS DCF model suggests Privia Health Group is trading 45.4% below its estimated future cash flow value of $43.36, the current P/E of 137.1x tells a different story. That multiple is far above the fair ratio of 30.8x, the US Healthcare industry at 22.7x, and peers at 61.1x, which points to meaningful valuation risk if earnings or sentiment slip.

That kind of gap between a cash flow model and rich earnings multiples raises a simple question: which signal do you trust more, the implied upside from long term cash flows or the premium multiple the market is already paying today?

Next Steps

With sentiment on Privia Health Group split between meaningful risks and clear potential rewards, this is a moment to act quickly by looking through the details yourself and deciding how the balance stacks up using the 4 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Privia Health Group?

If Privia Health Group has sharpened your focus, do not stop here. Broaden your watchlist with other potential opportunities that could fit your goals and risk tolerance.

- Target higher income potential by reviewing companies in the 8 dividend fortresses that might suit a yield focused approach.

- Hunt for value by scanning the 45 high quality undervalued stocks where pricing and quality filters work together to surface possibilities.

- Prioritize stability by checking the 66 resilient stocks with low risk scores so you are not the last to spot resilient stocks with steadier profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.