Pursuit Attractions And Hospitality (PRSU) On Eagle Wing Tours And A Fair Value Debate

Pursuit Attractions and Hospitality, Inc. PRSU | 0.00 |

Acquisition of Eagle Wing Tours draws fresh attention to Pursuit Attractions and Hospitality

Pursuit Attractions and Hospitality (PRSU) has drawn fresh investor attention after acquiring Eagle Wing Tours in Victoria, British Columbia. The transaction adds a marine wildlife experience and provides entry into the Vancouver Island tourism market.

For context, Pursuit Attractions and Hospitality’s recent acquisition headlines come as the stock trades at US$53.17, with a 30 day share price return of 8.8% and a year to date share price return of 59.1%. The 1 year total shareholder return of 76.7% points to momentum that has built over a longer period than the latest news cycle.

If this kind of tourism driven story has your attention, it can be a useful time to widen your search with 18 top founder-led companies

Pursuit Attractions and Hospitality now owns a broader set of destination experiences and a stock that has already delivered strong recent returns, so the next step is clear: Is investors’ enthusiasm already reflected in today’s price?

Most Popular Narrative: 24% Undervalued

Compared with Pursuit Attractions and Hospitality’s last close at $53.17, the most followed narrative points to a higher fair value anchored at $70, built using an 8.8% discount rate.

Growth investments such as the Jasper SkyTram gondola replacement, Banff Gondola capacity and experience upgrades, and the reintroduction of Denali Backcountry Adventure are aimed at reinforcing these sites as anchor experiences. These initiatives can support volume growth, higher effective ticket prices and improved EBITDA.

Want to see what underpins that $70 figure? The narrative leans heavily on faster earnings, fatter margins and a future profit multiple that assumes investors keep paying up. Curious which exact profit profile and revenue path have been baked into that story?

Result: Fair Value of $70 (UNDERVALUED)

However, there are clear risks around Pursuit Attractions and Hospitality’s heavy upfront growth spending, as well as its reliance on sustained demand for high priced, bucket list trips.

Another View on Pursuit Attractions and Hospitality’s Valuation

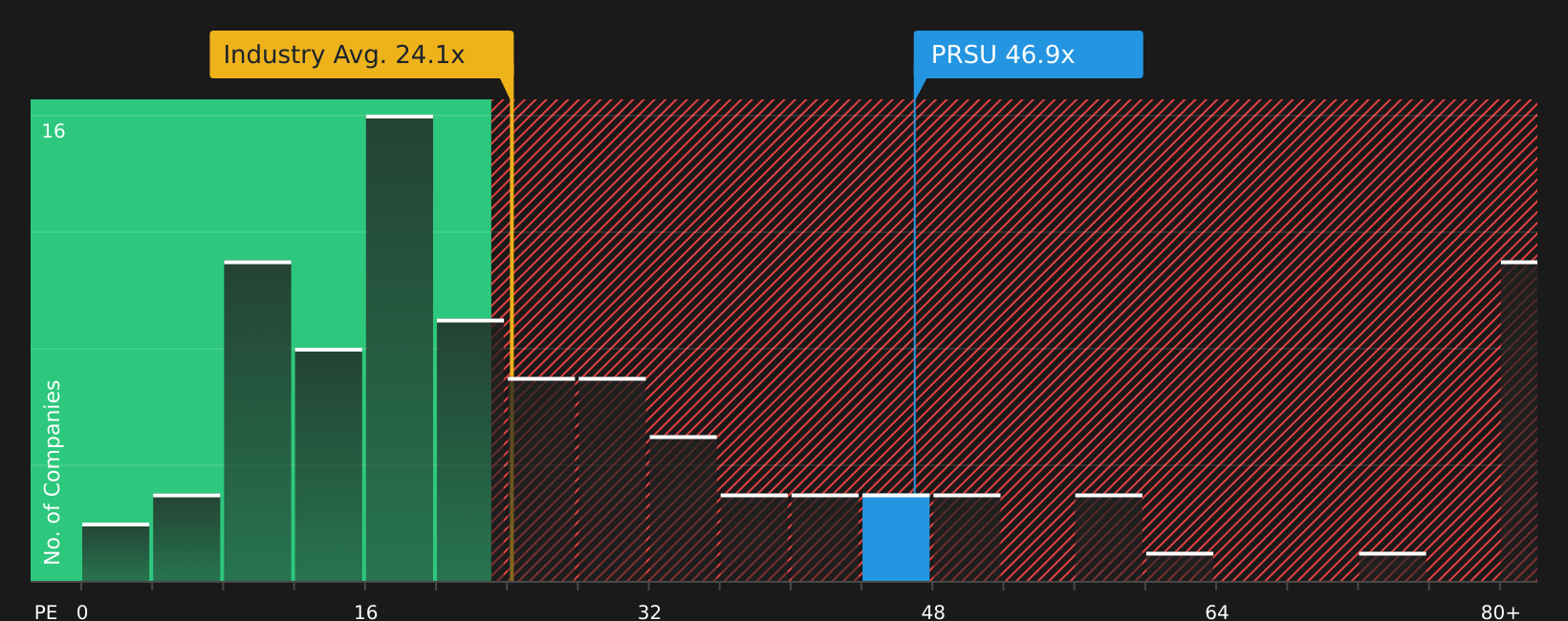

The popular $70 fair value narrative paints Pursuit Attractions and Hospitality as 24% undervalued, but the current P/E of 46.9x tells a different story. That is roughly double both the US Hospitality sector at 24.2x and peers at 22.9x, and almost twice the fair ratio of 23.9x, which points to meaningful valuation risk if expectations ease.

Want to see how those P/E gaps compare with the underlying numbers, and what levels the market might potentially converge toward over time? See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With all this optimism around Pursuit Attractions and Hospitality, it helps to move quickly from headlines to hard data and your own judgment. To see what those rewards look like in detail, review the 2 key rewards.

Looking for more investment ideas beyond Pursuit Attractions and Hospitality?

If Pursuit Attractions and Hospitality has sharpened your focus on quality, now is the moment to widen your watchlist and line up your next potential moves.

- Target dependable income by reviewing companies in the 8 dividend fortresses and see which stocks align with your cash flow goals.

- Spot potential mispricings early by scanning the screener containing 20 high quality undiscovered gems before the crowd starts paying attention.

- Prioritize resilience by focusing on companies in the 82 resilient stocks with low risk scores that may better fit a cautious, long term approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.