PVH (PVH) Is Up 5.3% After Profit Beats But 2026 Revenue Outlook Stays Flat – What's Changed

PVH Corp. PVH | 0.00 |

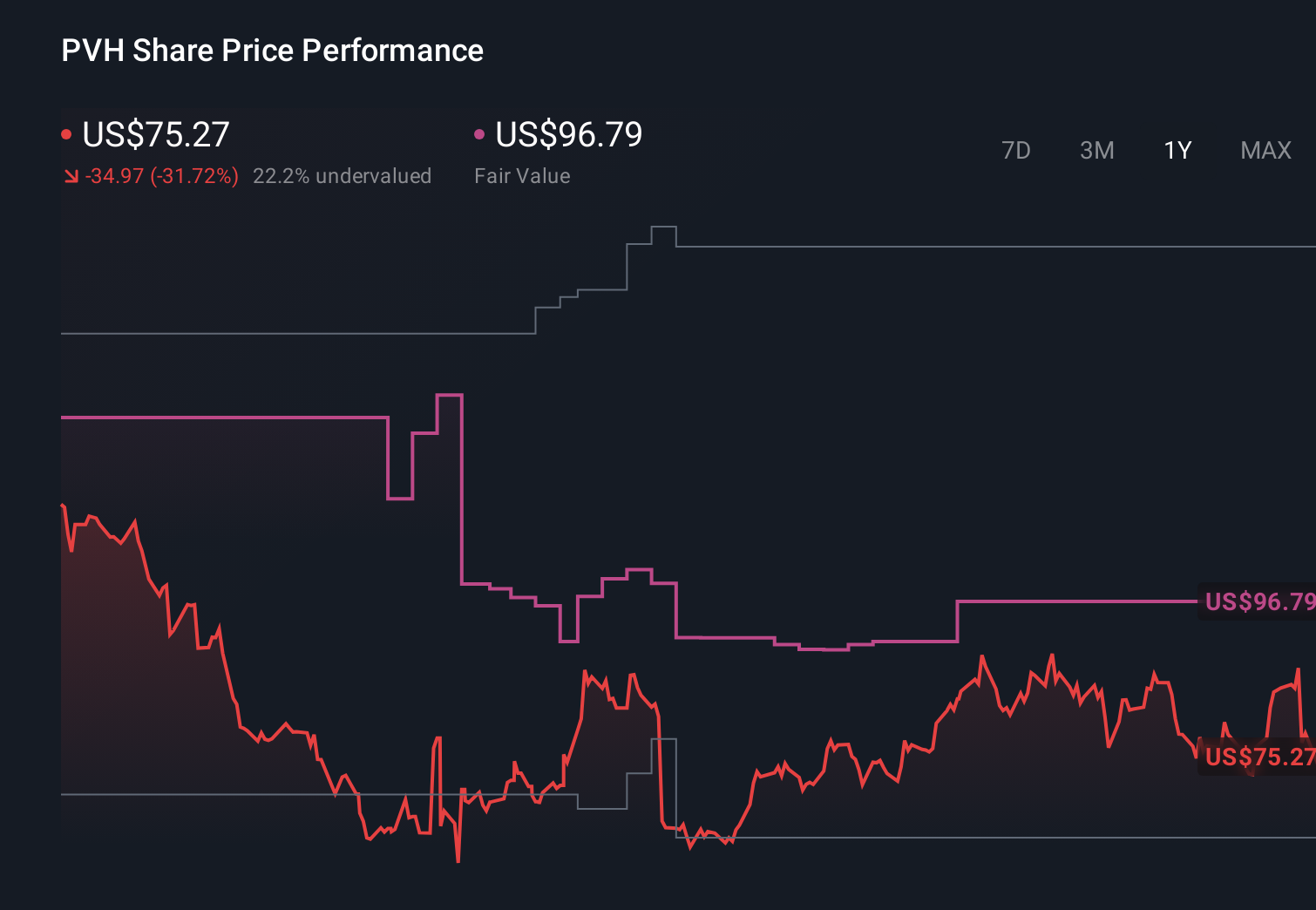

- PVH Corp. recently reported first-quarter 2026 results, with sales rising to US$2,025.1 million and net income improving to US$88 million, alongside diluted earnings per share from continuing operations of US$1.90.

- At the same time, PVH projected roughly flat full-year 2026 revenue and a 3% to 4% second-quarter revenue decline, underscoring how conflict-related pressure in EMEA is offsetting momentum in its direct-to-consumer and e-commerce channels.

- Next, we'll examine how PVH’s stronger profitability but softer 2026 revenue outlook affects the existing investment narrative around its core brands.

Find 44 companies with promising cash flow potential yet trading below their fair value.

PVH Investment Narrative Recap

To own PVH today, you need to believe its Calvin Klein and Tommy Hilfiger franchises can translate brand strength into steadier earnings, even if revenue is flat for a while. The latest quarter shows better profitability, but the softer 2026 revenue outlook makes near term demand in EMEA the key catalyst and key risk. Management’s guidance implies that conflict related weakness is the main drag, and while it is meaningful, it does not yet overturn the broader brand led thesis.

Against this backdrop, the most relevant announcement is PVH’s updated 2026 guidance, which calls for flat full year revenue and a 3% to 4% decline in the second quarter. This tempers earlier expectations of slight growth and matters for anyone focused on PVH’s push into higher margin direct to consumer and e commerce, because it highlights how quickly regional shocks can offset progress in those channels and delay the pay off from its PVH+ efficiency efforts.

But while near term demand risks in EMEA are front of mind, investors should also be aware of growing pressure from online native competitors and...

PVH's narrative projects $9.6 billion revenue and $734.4 million earnings by 2029. This requires 2.1% yearly revenue growth and about a $576 million earnings increase from $158.1 million today.

Uncover how PVH's forecasts yield a $93.08 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts take a much harsher view than consensus, warning that online native competitors could steadily erode PVH’s core wholesale business even though they still model revenue at about US$9.3 billion and earnings near US$766 million by 2029. Given PVH now guides to flat 2026 sales, you may find it useful to compare this pessimistic scenario with your own expectations and see whether the latest results shift your view of what is realistic.

Explore 3 other fair value estimates on PVH - why the stock might be worth just $93.08!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your PVH research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free PVH research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PVH's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.