Qualcomm Balances Chip Shortage Pressures With Automotive And IoT Expansion

QUALCOMM Incorporated QCOM | 126.80 | -0.38% |

- Qualcomm is reporting significant operational headwinds as a global memory chip shortage constrains smartphone production and handset revenue forecasts.

- Management and industry analysts describe broad supply chain challenges, with key OEMs, particularly in China, cutting chipset inventories.

- The company is pursuing diversification, completing acquisitions and expanding its presence in automotive and IoT to counter handset market pressure.

- These developments are influencing Qualcomm’s outlook through 2026 and shaping how investors assess NasdaqGS:QCOM today.

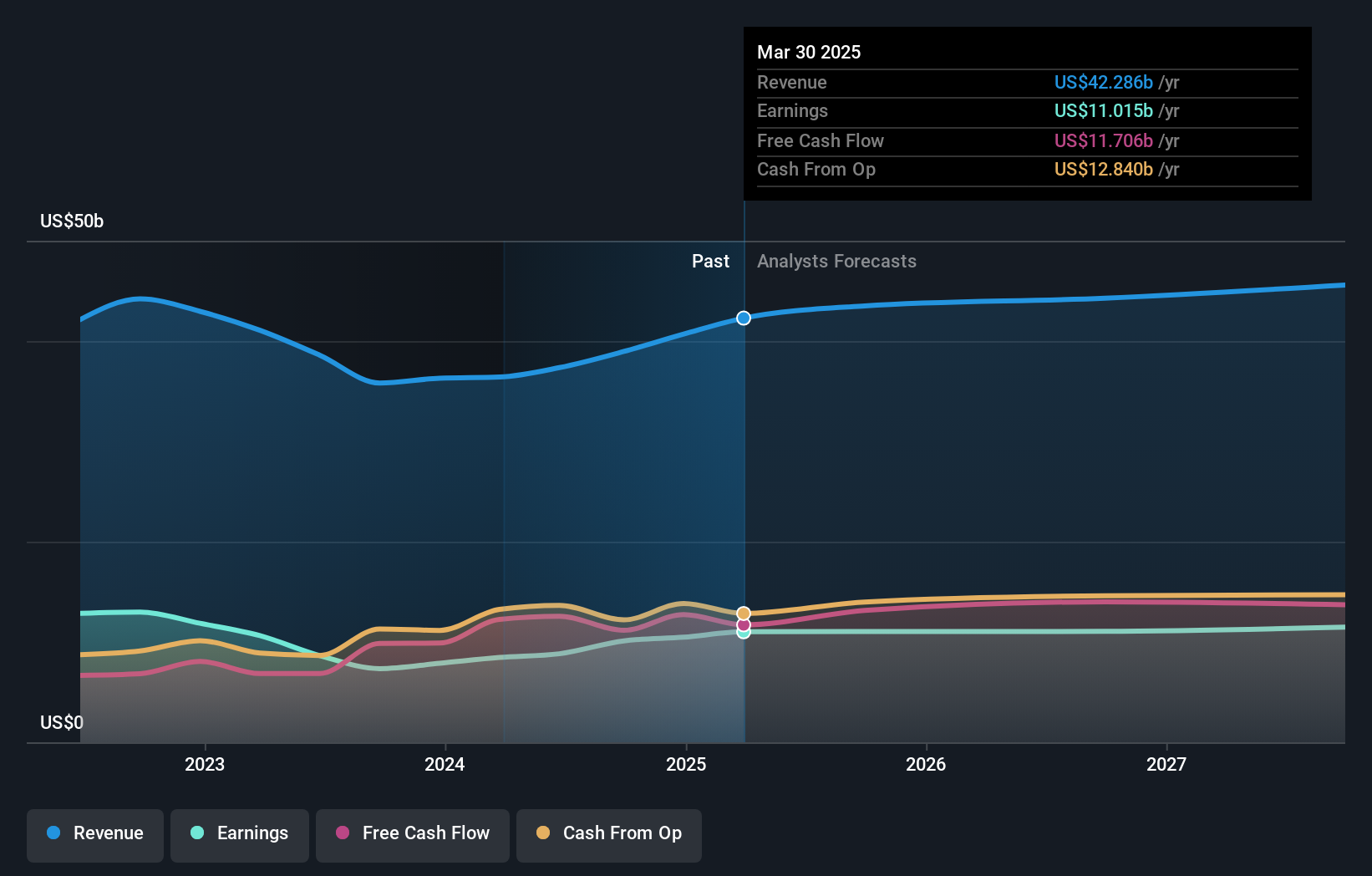

Qualcomm, trading on the NasdaqGS under ticker QCOM, sits at the center of smartphone and connectivity supply chains. A global memory chip shortage therefore directly affects its core handset segment. The shares currently trade at $140.09, with a 21.2% decline over the past 30 days and a 19.0% decline year to date, reflecting market concern around these operational constraints. Over 3 years, the stock shows a 13.3% return, which gives longer term holders a different perspective than those focused on recent volatility.

For investors, the key tension is between pressure on handset revenue guidance and Qualcomm’s efforts to build more exposure to automotive and IoT through completed acquisitions. The chip shortage and reduced OEM inventories, especially in China, raise questions about how long handset headwinds could weigh on results, including through 2026. At the same time, the broader portfolio the company is assembling may change how much its future depends on the smartphone cycle.

Stay updated on the most important news stories for QUALCOMM by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on QUALCOMM.

For you as an investor, the key takeaway is that Qualcomm is trying to reshape its business model while dealing with a handset-specific shock. The memory chip shortage is pressuring Android smartphone volumes, particularly in China, which several analysts link to weaker guidance and a tougher backdrop through 2026. That matters because handsets still account for the bulk of Qualcomm’s chip revenue, so lower unit shipments and higher memory costs can dilute earnings power even when reported quarterly revenue, such as US$12,252m in Q1 2026, holds up. At the same time, Qualcomm is leaning into acquisitions like Alphawave Semi and Ventana Micro Systems, as well as growing automotive and IoT, to rely less on phones over time and compete more broadly with peers such as MediaTek, Broadcom and Nvidia. The appointment of Brett Simpson as head of investor relations also suggests Qualcomm wants to sharpen how it explains this shift. This can influence how the market weighs short term handset stress against the longer term expansion into data center, automotive and industrial uses.

How This Fits Into The QUALCOMM Narrative

- The push into automotive, industrial IoT and data center through acquisitions directly supports the narrative that diversification can reduce dependence on a single handset customer base.

- Persistent memory shortages and weaker Android demand challenge the idea that premium Android execution alone can support a smooth earnings path while diversification is still small in absolute terms.

- The scale and timing of the Alphawave and Ventana contributions, as well as the impact of the new investor relations leadership, may not yet be fully captured in existing narrative assumptions about execution risk and communication with the market.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for QUALCOMM to help decide what it's worth to you.

The Risks and Rewards Investors Should Consider

- ⚠️ Heavy reliance on handsets, with analysts highlighting pressure from memory shortages and softer Android demand, leaves earnings exposed if unit volumes stay weak.

- ⚠️ Newer areas like data center and RISC V based products require ongoing investment and successful integration of recent acquisitions, which may weigh on profitability if uptake is slower than expected.

- 🎁 Completed share repurchases of about US$10.41b and continued diversification into automotive and IoT show management is actively reshaping the capital structure and revenue mix.

- 🎁 Analysts point to Qualcomm’s strong position in premium smartphones and growing exposure to non handset end markets, which some see as a potential support for longer term earnings resilience.

What To Watch Going Forward

From here, you may want to watch how quickly handset demand stabilizes in key Android markets, especially China, and whether Qualcomm’s guidance continues to reflect memory constraints. Progress on integrating Alphawave Semi and Ventana Micro Systems, as well as updates on design wins in automotive and IoT, will help you gauge how meaningful diversification is becoming compared with the core smartphone business. Analyst commentary around pricing power, mix of premium versus lower end devices, and any shifts in market share against competitors like Apple and MediaTek will also be important signals.

To ensure you're always in the loop on how the latest news impacts the investment narrative for QUALCOMM, head to the community page for QUALCOMM to never miss an update on the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.