Qualcomm Balances Chip Shortage Pressures With Expansion Beyond Smartphones

QUALCOMM Incorporated QCOM | 126.80 | -0.38% |

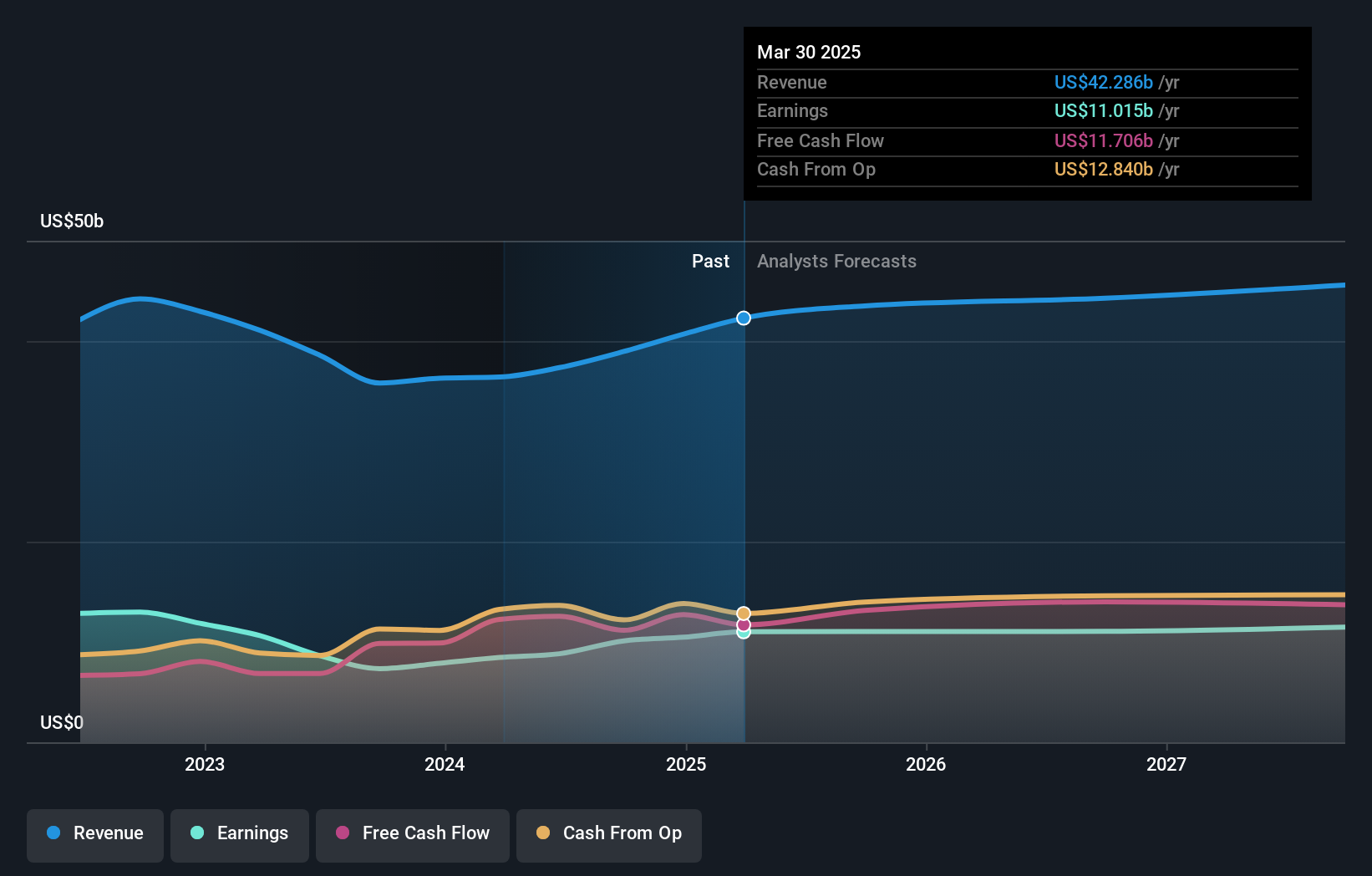

- Qualcomm (NasdaqGS:QCOM) reports record revenue and earnings but signals a cautious outlook as global memory chip shortages weigh on smartphone production.

- Supply constraints are affecting handset manufacturers even where consumer demand exists, creating near term pressure on Qualcomm's core mobile business.

- The company is accelerating diversification, announcing moves in automotive, IoT, robotics, and data centers, including acquisitions of Alphawave Semi and Ventana Micro Systems.

- Qualcomm is expanding partnerships with automakers such as Volkswagen and Hyundai to grow its presence in connected and automated vehicle platforms.

For investors watching Qualcomm, the current story is a mix of operational strain and business expansion. The smartphone segment remains central to Qualcomm's identity, yet the memory chip shortage is constraining how much of that demand can convert to shipped devices. At the same time, the company is pushing further into areas like automotive systems, IoT devices, robotics, and data center technology.

The recent acquisitions and partnership announcements suggest Qualcomm is trying to reduce its dependence on any single end market over time. As you think about NasdaqGS:QCOM, the key questions now are how long supply issues might influence handset volumes and how quickly newer areas like automotive and data centers could grow into more meaningful contributors within the broader business mix.

Stay updated on the most important news stories for QUALCOMM by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on QUALCOMM.

Quick Assessment

- ✅ Price vs Analyst Target: At US$137.34, QCOM trades about 16.7% below the US$164.85 analyst target range midpoint.

- ✅ Simply Wall St Valuation: Simply Wall St estimates the shares are trading roughly 20.2% below fair value.

- ❌ Recent Momentum: The 30 day return of about 23.8% decline signals weak short term momentum.

Check out Simply Wall St's in depth valuation analysis for QUALCOMM.

Key Considerations

- 📊 Memory chip shortages are pressuring Qualcomm's core smartphone revenues. At the same time, the company is pushing harder into automotive, IoT, robotics, and data centers.

- 📊 Watch how handset volumes, automotive design wins, and data center traction line up against the current P/E of 27.3 compared with the Semiconductor industry average of 44.0.

- ⚠️ Profit margins of 11.9% are below the industry average of 15.4%. The recent margin decline is a key point to track if shortages persist.

Dig Deeper

For the full picture including more risks and rewards, check out the complete QUALCOMM analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.