Qualcomm Weighs Memory Shock As Data Center And RISC V Bets Grow

QUALCOMM Incorporated QCOM | 126.80 | -0.38% |

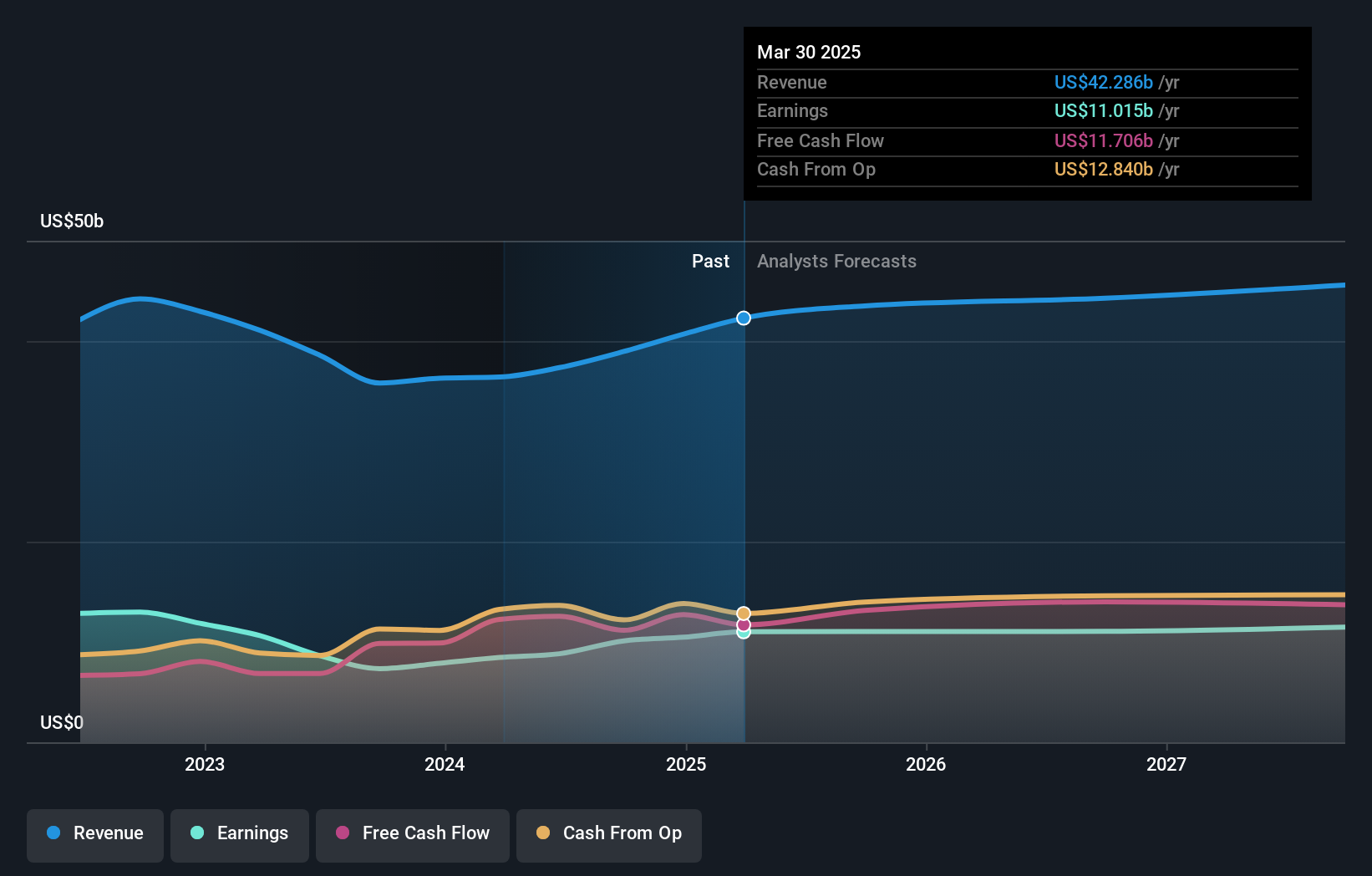

- Qualcomm (NasdaqGS:QCOM) is facing significant pressure on its core smartphone business from an industry wide memory chip shortage that is constraining handset production.

- The company recently reported quarterly results that came in ahead of expectations, but issued softer guidance as memory supply issues weigh on revenue visibility for the next few quarters.

- Qualcomm has agreed to acquire Alphawave Semi to build out its data center presence and Ventana Micro Systems to expand its RISC-V CPU capabilities.

- These moves highlight a key turning point as Qualcomm contends with semiconductor supply headwinds while working to reduce its reliance on smartphones over time.

Qualcomm, best known for its smartphone chipsets and wireless technologies, is now contending with a memory shortage that is limiting how many premium handsets its customers can ship. That constraint feeds directly into demand for Qualcomm’s core products, even as end user appetite for high end devices remains firm. In this context, the company is focusing more on data center and RISC-V CPU markets through the Alphawave Semi and Ventana Micro Systems deals.

For you as an investor, the combination of supply constraints and new acquisitions points to a more complex story for NasdaqGS:QCOM over the next few quarters. The memory shortage could keep results under pressure for some time, while the data center and RISC-V initiatives may take years to fully appear in reported numbers. How these moving parts settle is likely to influence how concentrated or diversified Qualcomm’s earnings base becomes relative to smartphones.

Stay updated on the most important news stories for QUALCOMM by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on QUALCOMM.

Investor Checklist for QUALCOMM

Quick Assessment

- ✅ Price vs Analyst Target: At US$148.89 versus a US$187.69 analyst target, the shares sit about 21% below consensus.

- ⚖️ Simply Wall St Valuation: The stock is described as trading close to estimated fair value, so expectations already reflect much of the current outlook.

- ❌ Recent Momentum: The 30 day return of about 15.6% decline flags weak short term sentiment.

Check out Simply Wall St's in depth valuation analysis for QUALCOMM.

Key Considerations

- 📊 The memory shortage is directly affecting Qualcomm’s core smartphone revenue stream. New data center and RISC V deals are drawing more attention to diversification.

- 📊 Watch how handset shipment commentary, data center design wins, and any updates on Alphawave Semi and Ventana integration show up in revenue mix and margins.

- ⚠️ Net profit margin is 12.5% compared with 25.9% last year, so further pressure from supply constraints could keep profitability under strain.

Dig Deeper

For the full picture including more risks and rewards, check out the complete QUALCOMM analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.