Qualys (QLYS) Margins Near 30% Test Bullish Growth Narratives After FY 2025 Results

Qualys, Inc. QLYS | 83.22 83.22 | +2.24% 0.00% Pre |

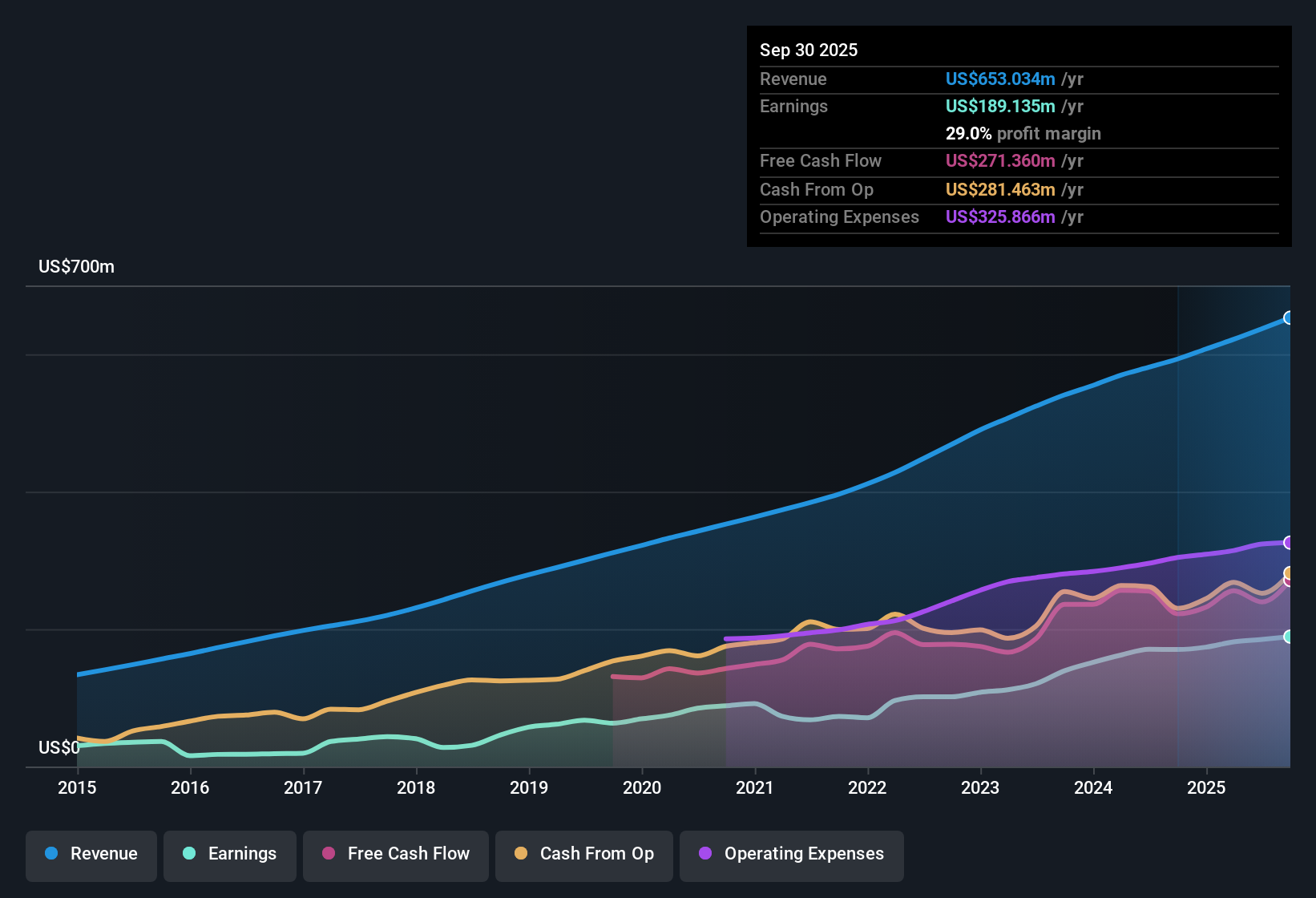

Qualys (QLYS) just wrapped up FY 2025 with Q4 total revenue of US$175.3 million and basic EPS of US$1.48, setting the tone for how the full year’s profitability story reads. Over the past six quarters, revenue has moved from US$153.9 million in Q3 2024 to US$175.3 million in Q4 2025, while quarterly basic EPS shifted from US$1.26 to US$1.48 over the same window. This gives investors a clear view of the recent trend in top line and per share earnings. With trailing twelve month net income at US$198.3 million and net margins holding close to 30%, the latest results keep the focus firmly on how durable that profit profile looks from here.

See our full analysis for Qualys.With the headline numbers on the table, the next step is to see how these results line up with the widely held narratives around Qualys, and where the data may challenge or reinforce those views.

Five year earnings growth supports the current profit story

- Over the last five years, earnings have grown at about 21.4% per year, while trailing twelve month net income sits at US$198.3 million on US$669.1 million of revenue.

- What stands out for the bullish view is how this multi year earnings expansion lines up with current profitability, as trailing basic EPS of US$5.49 and a net profit margin of 29.6% compare against last year’s 28.6% margin and help frame Qualys as a platform based cybersecurity vendor backed by recurring revenue and a broad product set.

- Supporters who point to long term demand for cyber risk management can reference the combination of US$669.1 million in trailing revenue and a 29.6% margin as evidence that the business is converting that demand into profits.

- At the same time, the fact that last year’s net income was US$173.7 million on US$607.6 million of revenue shows that the current margin level is being compared against an already profitable base, which can matter when thinking about how durable that bullish case is.

Analysts looking at this earnings run rate have built a balanced view of Qualys, and you can see how that translates into expectations in the 📊 Read the full Qualys Consensus Narrative.

Margins near 30% with slower forecast growth

- On a trailing basis, net profit margin is 29.6% versus 28.6% a year earlier, while forward looking estimates point to earnings growth of about 3.3% per year and revenue growth of about 6.5% per year compared with US market forecasts of 15.6% for earnings and 10.2% for revenue.

- Critics highlight that these forecast growth rates are slower than the broader US market, and the comparison with the company’s own history sharpens that point because one year earnings growth of 14.2% sits below the 21.4% five year average, so investors weighing the bearish angle may focus on whether maintaining a roughly 30% margin can offset the gap between 3.3% expected earnings growth and the higher 15.6% market benchmark.

- For someone worried about growth, the contrast between 6.5% expected revenue growth and the 10.2% market figure is a clear number to keep in mind when deciding how much to pay for those margins.

- On the other hand, the shift from a 28.6% to 29.6% margin over the past year shows that profitability has held up alongside that slower growth profile, which is part of why the bearish view tends to revolve around future pace rather than current earnings quality.

P/E of 20x and DCF fair value gap

- At a share price of US$110.80, Qualys trades on a trailing P/E of 20x compared with 25.7x for the US Software industry and 44.2x for peers, and sits around 31.4% below a DCF fair value estimate of US$161.40, while the allowed analyst price target of US$139.32 implies a price move of roughly 26% from today’s level.

- Supporters of the bullish narrative often point to this combination of lower P/E and the gap to both DCF fair value and the US$139.32 analyst target, arguing that five year earnings growth of 21.4% and a 29.6% trailing margin provide some grounding for that upside case, while skeptics come back to the slower 3.3% and 6.5% forecast growth rates as reasons to question how quickly that gap might close.

- The roughly 31.4% difference between the current price and the US$161.40 DCF fair value is a concrete number investors can compare with their own expectations for future cash flows.

- Meanwhile, the 20x P/E against a 25.7x industry average shows that the market is assigning a discount to Qualys shares even with the company’s earnings track record, which is where individual views on those forward growth figures start to matter.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Qualys's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Qualys combines strong margins with slower forecast earnings and revenue growth than the wider US market, which can limit upside for investors focused on future pace.

If that slower growth profile gives you pause, check out our 53 high quality undervalued stocks to quickly spot other companies where current pricing may better reflect their potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.