Qualys (QLYS) Stock Valuation Check After Recent Rebound And DCF Discount

Qualys, Inc. QLYS | 0.00 |

Qualys (QLYS) has drawn investor attention after recent price moves, with the stock up about 27% over the past month and about 21% over the past 3 months from its recent levels.

Despite the recent momentum, with a 30 day share price return of 27.36% and a 90 day share price return of 20.58%, Qualys still has a year to date share price return decline of 12.49% and a 1 year total shareholder return decline of 17.66%. Recent gains are rebuilding after a weaker stretch.

If Qualys’s recent move has you rethinking your tech exposure, it could be a good time to broaden your search with 61 profitable AI stocks that aren't just burning cash

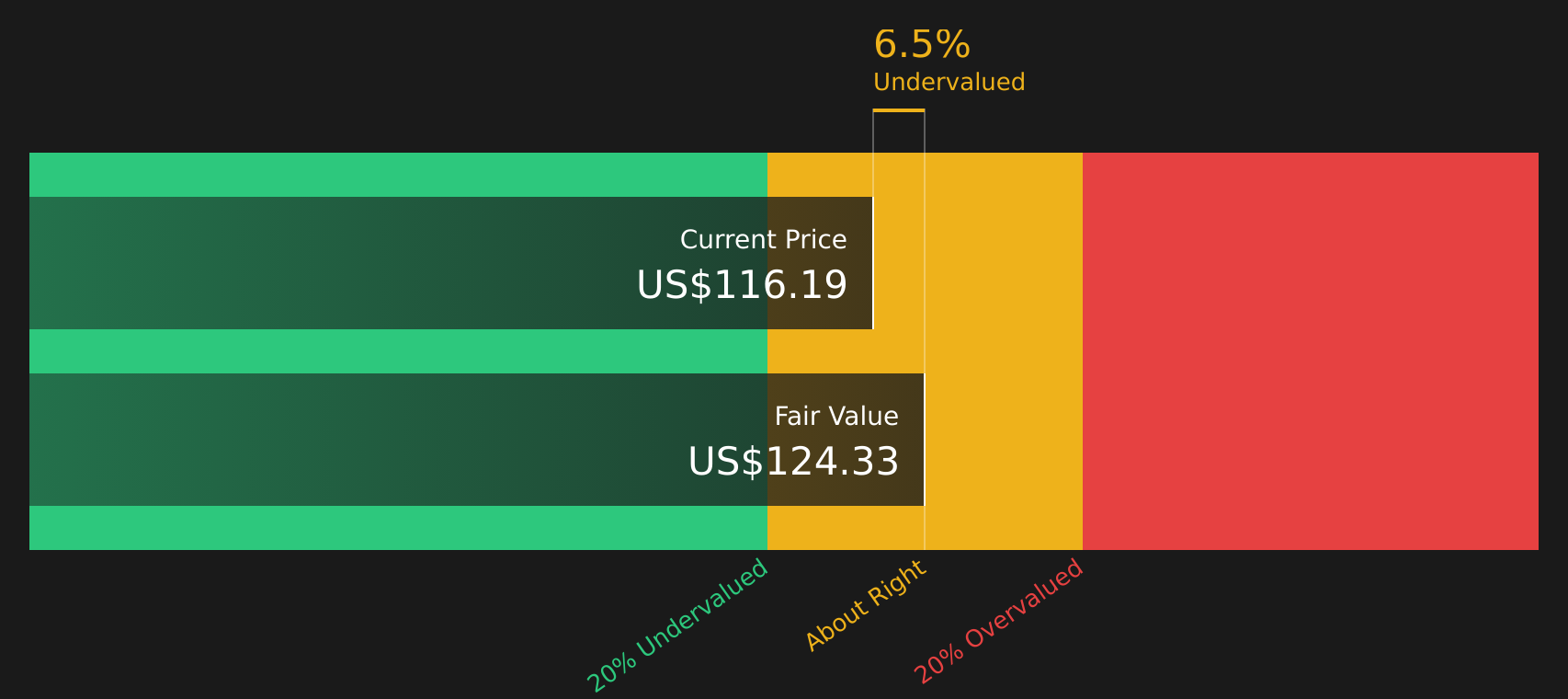

With Qualys trading around $114.65, recent gains and an intrinsic value estimate that indicates roughly a 7% discount raise a key question for you: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 7% Undervalued

With Qualys last closing at $114.65 against a narrative fair value of $107.39, the current debate centers on whether that valuation gap is justified by its long term earnings story under an 8.62% discount rate.

Adoption of Qualys' new cloud native risk operations center (ROC) and Agentic AI platform positions the company as a leading pre breach risk management provider, offering unified orchestration, automation, and remediation across both Qualys and non Qualys data; this opens incremental greenfield opportunities and is described as supporting higher ARPU and expanded TAM, which in turn is cited as a driver of durable revenue and earnings growth. Persistent digital transformation, cloud adoption, and increased regulatory scrutiny (such as GDPR and FedRAMP High compliance) are described as factors driving organizations globally to invest in proactive, unified cybersecurity solutions. Qualys' platform first approach and recent government sector wins (aided by exclusive FedRAMP High authorization) are characterized as potential drivers of faster land and expand cycles and incremental long term revenues.

Want to see what kind of revenue trajectory and profit margins would need to hold up to back that fair value? The narrative leans on steady growth, firm profitability and a future earnings multiple that would need to stay above current analyst targets. The full set of assumptions is where the real story sits.

Result: Fair Value of $107.39 (ABOUT RIGHT)

However, this story can change if AI security evolves faster than Qualys adapts, or if customers optimize Flex pricing in ways that weigh on revenue visibility and margins.

Another View: What The P/E Is Saying

The SWS DCF model suggests Qualys is trading below its future cash flow value at about a 7% discount, yet the current narrative fair value sits at $107.39, which is below the $114.65 share price. So is the market underestimating cash flows, or are the cash flow assumptions too generous?

Next Steps

If this mix of optimism and caution has you on the fence, do not wait to pressure test the thesis against the data. Start by reviewing the 4 key rewards.

Looking for more investment ideas?

If Qualys has sharpened your thinking, do not stop there. Use the Simply Wall Street Screener to uncover fresh opportunities that match your goals before others spot them.

- Target steady income potential by reviewing companies in the 9 dividend fortresses that focus on higher yields.

- Hunt for quality at a price that looks attractive with the 47 high quality undervalued stocks that filters for fundamentals first.

- Prioritize capital preservation and sleep better at night by checking out the 68 resilient stocks with low risk scores that screens for resilience.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.