QuantumScape (QS) Valuation Check After Eagle Line Commercialization Milestone

QuantumScape QS | 6.86 | +6.52% |

QuantumScape (QS) is back in focus after inaugurating its Eagle Line in San Jose, a highly automated production setup built around its Cobra separator process to support sampling, testing, and future large scale manufacturing.

The Eagle Line launch comes after a sharp reset in sentiment, with QuantumScape’s 1 day share price return of 8.72% decline and 90 day share price return of 53.37% decline contrasting with a 1 year total shareholder return of 54.69%. This suggests that long term holders have still seen gains even as recent momentum has faded.

If this kind of battery technology news has your attention, it could be a good moment to see what else is shaping the sector through our screener of 22 quantum computing stocks and compare how other quantum related names are trading.

With QS down 53.37% over 90 days but still showing a 54.69% 1-year total return and trading at US$7.75 versus an average analyst target of US$9.88, is this a reset that creates an opening, or is the market already pricing in the next leg of growth?

Most Popular Narrative: 85.9% Undervalued

At a last close of $7.75 against a narrative fair value of $55, QuantumScape’s valuation gap is wide, and the bullish thesis leans heavily on how its technology could reshape high demand use cases.

The U.S. power grid, currently strained by the build-out of 1GW+ data centers, could see a radical transformation through high-performance "power walls." For AI-driven infrastructure, where uptime and safety are non-negotiable, QuantumScape ($QS) ceramic-based cells offer a level of stability that traditional lithium-ion systems struggle to match.

Curious what kind of revenue and margin profile might justify that kind of valuation gap. The narrative leans on aggressive growth beyond autos, plus an asset light, royalty heavy model. Want to see how those assumptions stack up across data centers, robotics, drones and premium EVs.

Result: Fair Value of $55 (UNDERVALUED)

However, this story can break if Eagle Line scaling stumbles or if key partners, such as Volkswagen or ceramics suppliers, slow, change, or cancel commercialization plans.

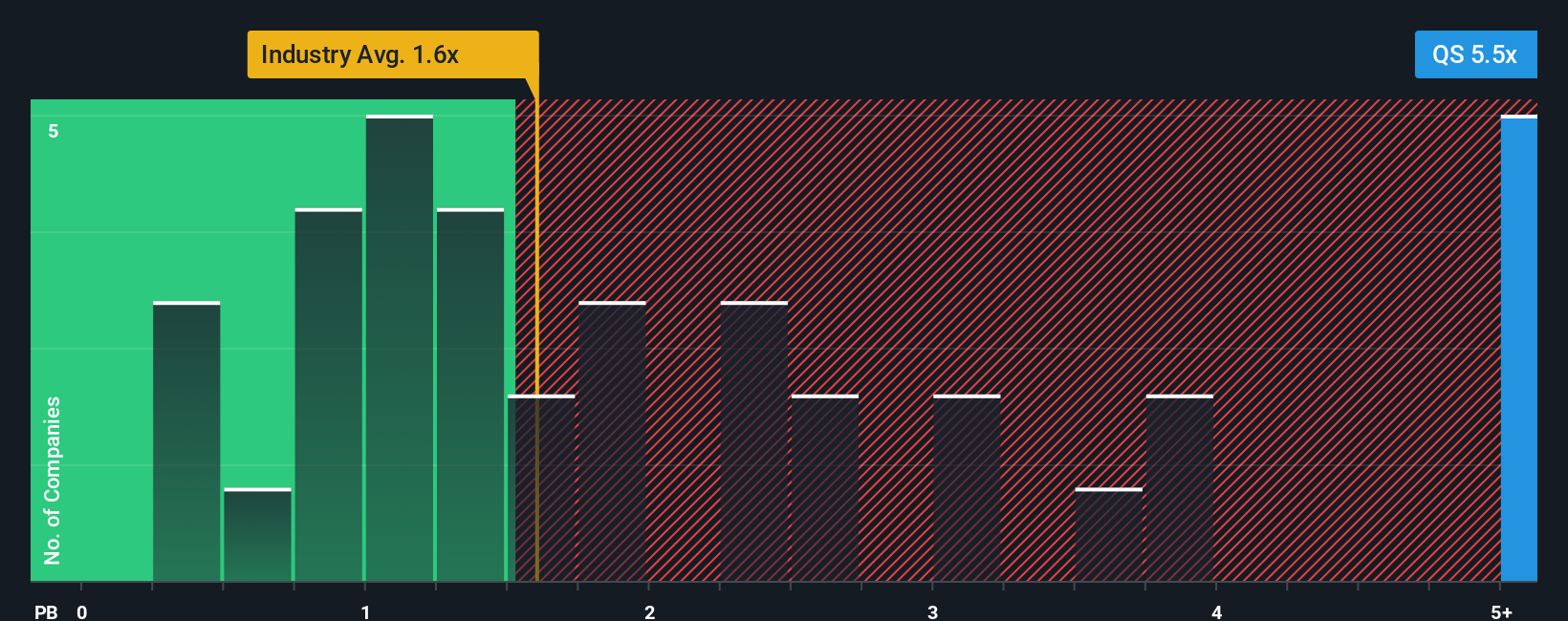

Another Take Using P/B

While the SWS DCF model points to a fair value near $53.81 and labels QS as undervalued, the current P/B of 3.8x tells a different story. That is more than double both the US Auto Components industry average of 1.7x and the peer average of 1.8x, which leans toward an expensive reading.

This kind of gap can mean the market is already paying up for future execution, so any setback on technology or commercialization could weigh heavily on the share price. On the other hand, if the royalty heavy story plays out, some investors might see the premium as justified. Which signal do you put more weight on?

Build Your Own QuantumScape Narrative

If you see the numbers differently or prefer to rely on your own analysis, you can test your thesis and build a custom view in minutes: Do it your way

A great starting point for your QuantumScape research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If QuantumScape sits in your “interesting, but I want a few more options” bucket, this is the moment to line up a broader watchlist before the next catalyst hits.

- Target potential mispricings by scanning 54 high quality undervalued stocks and focusing on companies that pair quality fundamentals with prices that may not fully reflect their underlying strength.

- Strengthen your income focus by reviewing 15 dividend fortresses and looking for companies that combine higher yields with profiles some investors view as more resilient.

- Limit unwanted surprises by checking 79 resilient stocks with low risk scores and concentrating on businesses where models and balance sheets score well on Simply Wall St’s risk framework.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.