Quest Diagnostics (DGX) Stock Trades Cheap On Cash Flow But Fair On Earnings

Quest Diagnostics Incorporated DGX | 0.00 |

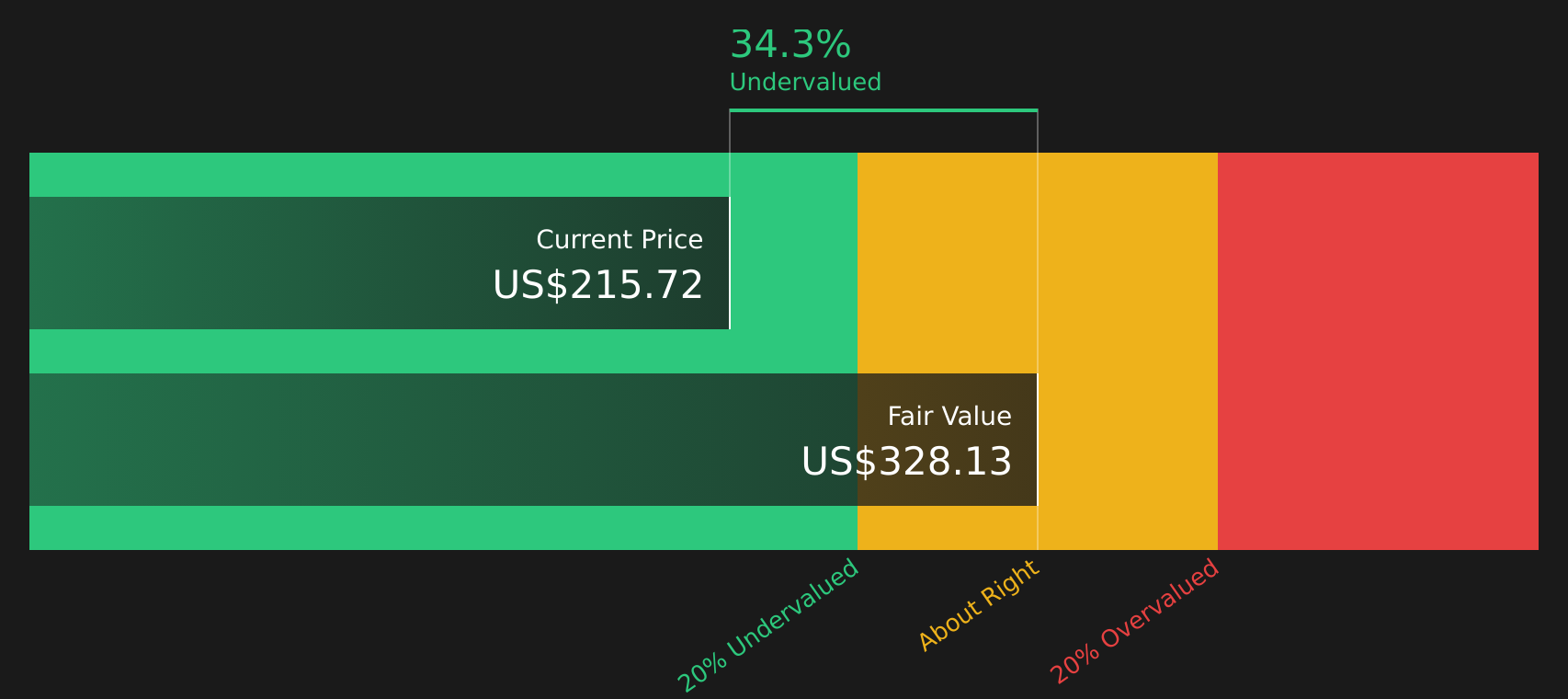

Quest Diagnostics stock has delivered a 76.9% total return over the past five years, and the latest valuation work using a Discounted Cash Flow (DCF) estimate points to the shares still trading at roughly a 33.3% discount to intrinsic value, even as earnings-based multiples look closer to fair. With the company in the headlines for new diagnostics offerings and upcoming results, investors are weighing whether that apparent discount reflects opportunity or embedded risks.

- A 76.9% five-year return suggests Quest Diagnostics has already rewarded long-term holders, so any further upside case now leans more heavily on how today’s price compares with its intrinsic value estimate.

- Growth in advanced and oncology diagnostics can support expectations for future cash flows, while concerns around debt levels and changing healthcare policy may limit how much value investors are willing to ascribe to that pipeline.

- On Simply Wall St’s checks, Quest Diagnostics scores 5 out of 6 on valuation, which means the broader set of tests leans toward the stock being priced on the cheap side rather than fully reflecting its fundamentals.

The issue now is whether Quest Diagnostics’ current share price already fairly captures its cash flow potential, or if the DCF-based discount still offers a margin of safety.

Does Quest Diagnostics Look Undervalued on Cash Flow?

The Discounted Cash Flow (DCF) model here uses projected free cash flows to estimate what Quest Diagnostics might be worth today. In this approach, Quest Diagnostics generated about $1.36b in free cash flow over the last twelve months, with the model assuming gradually growing cash flows from this base rather than aggressive expansion or sharp decline.

Those cash flow projections translate into an estimated intrinsic value of about $324 per share, which sits roughly 33.3% above the current share price and indicates that the stock appears undervalued on this measure. The recent approval of Quest Diagnostics’ Haystack MRD test and its broader oncology diagnostics focus help explain why a cash flow based estimate incorporates ongoing contributions from higher value testing, even if the market is still applying a discount.

On this DCF view, Quest Diagnostics appears undervalued, with the share price sitting well below the model’s estimate of intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests Quest Diagnostics is undervalued by 33.3%. Track this in your watchlist or portfolio, or discover 42 more high quality undervalued stocks.

Where Does Quest Diagnostics Sit on Earnings?

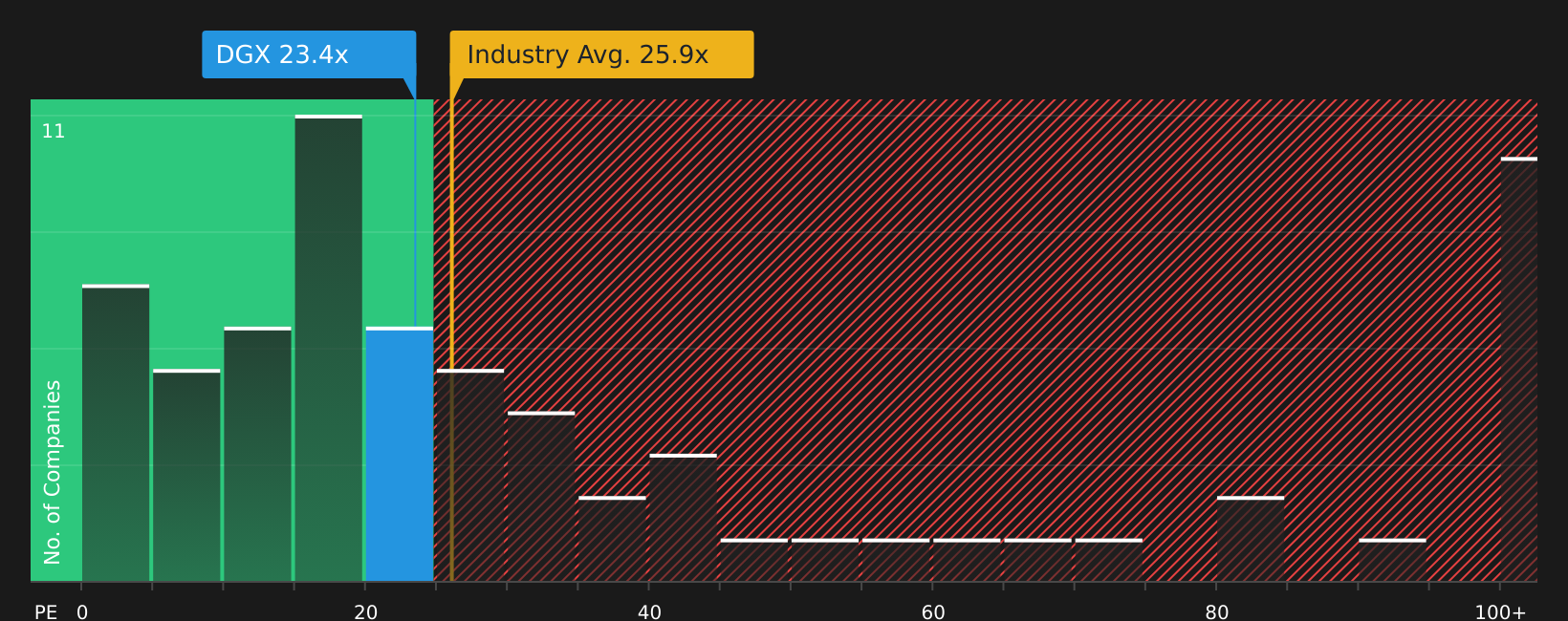

The P/E ratio is a useful way to check how Quest Diagnostics is being priced against its earnings power. Right now, Quest Diagnostics trades on a P/E of about 23.4x, which sits below both the healthcare industry average of roughly 25.6x and the peer group average of around 35.3x.

The fair P/E multiple implied by the model is about 25.2x, only slightly above where the stock is currently trading. That gap suggests the market is assigning Quest Diagnostics a valuation that is broadly in line with what the company’s earnings profile, risk mix, and industry position would justify, rather than a clear discount or premium on this metric.

Overall, Quest Diagnostics appears roughly fairly valued on its P/E multiple, with the current price sitting close to the model’s view of a reasonable earnings-based valuation.

The Quest Diagnostics Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Quest Diagnostics connect the valuation puzzle to the underlying assumptions about Quest Diagnostics' future growth, margins and earnings that would need to hold for the stock to be worth materially more or less than today's price, and they sit on the company’s Community page. Where a ratio or model offers a single figure, these narratives unpack the future that number relies on so you can monitor whether reality is tracking that path.

You can add your own Narrative on Quest Diagnostics, setting out a number driven view on whether developments like its expanded oncology and precision psychiatry partnerships support the current valuation or call for a different pricing.

Share your thesis, track how it holds up as new results and product updates emerge, and see how it sits alongside other perspectives in the Simply Wall St community.

Do you think there's more to the story for Quest Diagnostics? Head over to our Community to see what others are saying!

The Bottom Line

For Quest Diagnostics, the Discounted Cash Flow (DCF) view still points to a clear intrinsic value gap, while the P/E comparison suggests the stock is now priced about right against peers. Taken together with the broader valuation checks, the focus is on whether the market continues to underappreciate the durability and quality of Quest Diagnostics’ future cash flows. From here, the debate largely turns on how confidently you view its ability to sustain profitable growth in higher value testing without eroding returns through funding needs or execution risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.