Rackspace Technology (RXT) Stock Could Be 187% Overvalued After AMD AI Deal And Job Cuts

Rackspace Technology, Inc. RXT | 0.00 |

Rackspace Technology (RXT) stock is reacting to twin announcements: a definitive agreement with AMD for 30 MW of AI compute across its global data centers, and a 15% workforce reduction tied to its governed enterprise AI focus.

The Rackspace Technology share price is up 4.99% over the last day and has a 7 day share price return of 33.26%, adding to a 90 day gain of 235.68% and a very large year to date rise. The 1 year total shareholder return of 385.16% contrasts with a 5 year total shareholder return that is down 67.91%, pointing to strong recent momentum after a weak longer term record as investors reassess the company around the AMD partnership, workforce reduction and expansion in Riyadh.

If Rackspace Technology’s AI push has your attention, it may be worth seeing what else is moving in related areas through our curated screener of 48 AI infrastructure stocks

With Rackspace Technology stock already trading above the average analyst price target and recent 1-year returns very large, the key question now is whether there is still a mispricing or if the market is already pricing in future growth.

Most Popular Narrative: 187% Overvalued

Rackspace Technology is trading at $6.21 against a most followed narrative fair value estimate of $2.17, so the story behind that gap really matters.

Ongoing digital transformation and increasing complexity of hybrid/multi-cloud environments are driving strong demand for Rackspace's managed cloud services, as evidenced by double-digit year-over-year bookings growth and a shift toward larger, longer-term enterprise contracts. This is likely to support a sustained rebound in revenue and enhance revenue visibility.

Want to see what kind of revenue mix, margin lift and valuation multiple are baked into that fair value line? The assumptions behind this Rackspace Technology narrative lean heavily on recurring contracts, changing profitability and how much investors might be willing to pay for those future earnings.

Result: Fair Value of $2.17 (OVERVALUED)

However, there are still clear pressure points. Rackspace Technology reported a loss of $146.0 million, and both Public Cloud and Private Cloud revenues declined year over year.

Another View on Rackspace Technology Valuation

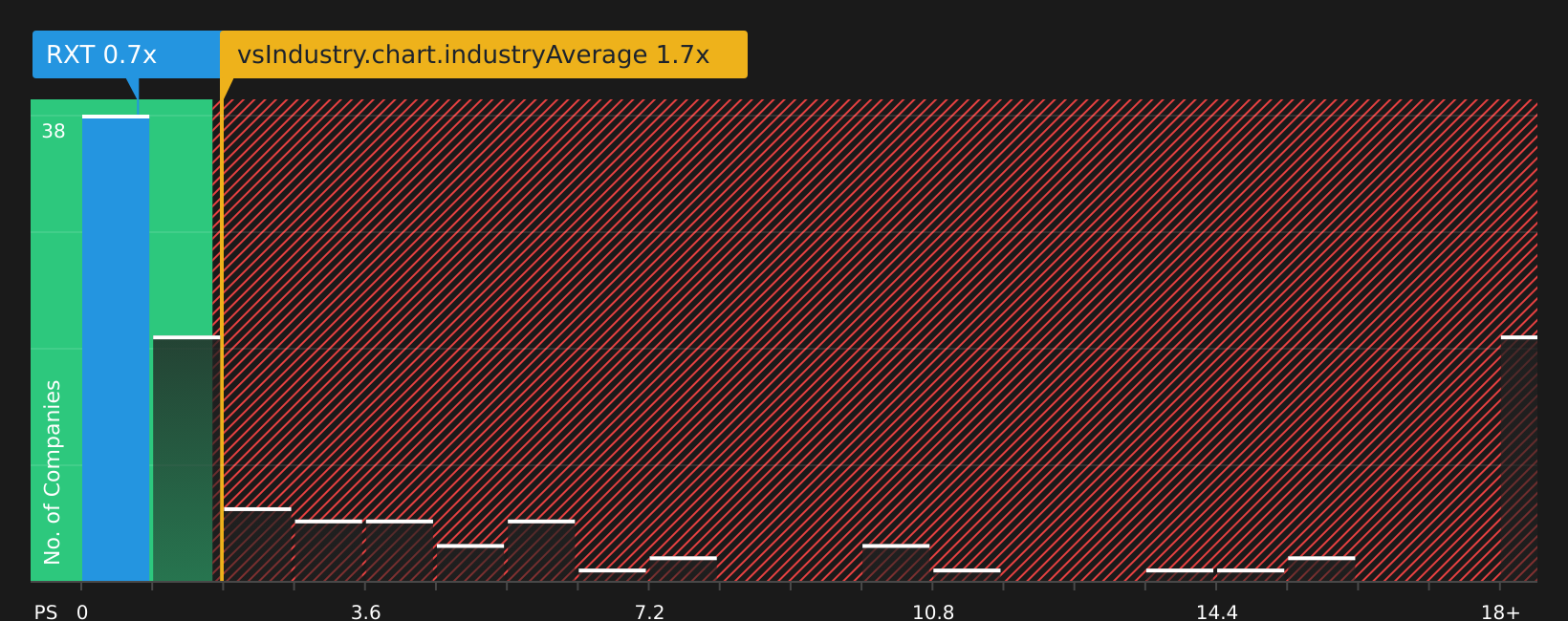

The most followed Rackspace Technology narrative points to a fair value of $2.17, which suggests the stock is 187% overvalued at $6.21. Yet on a simple P/S basis, Rackspace Technology trades at 0.6x, compared with 1.8x for the US IT industry and a fair ratio of 1.2x. That discount implies the market is pricing in real balance sheet and profitability risks, so the puzzle is whether those concerns are already fully reflected or not.

To see how those P/S gaps could matter in practice, and what they say about valuation risk versus potential upside, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this Rackspace Technology story feels mixed to you, that is the point. The stock carries one key reward and four important warning signs, 1 key reward and 4 important warning signs

Looking for more investment ideas beyond Rackspace Technology?

- Spot potential bargains early by scanning companies priced for pessimism with strong fundamentals through the 44 high quality undervalued stocks

- Prioritize resilience and sleep-better-at-night holdings by reviewing companies in the 67 resilient stocks with low risk scores

- Hunt for overlooked opportunities with quality metrics on your side using the screener containing 20 high quality undiscovered gems

If you stop with Rackspace Technology stock, you could miss out on other compelling ideas that fit your style. Keep widening your opportunity set.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.