Radware (RDWR) Valuation in Focus After Exposing Major ChatGPT Security Flaw

Radware Ltd. RDWR | 0.00 |

If you’re following cybersecurity stocks, Radware (RDWR) has just landed squarely in the spotlight. The company uncovered and disclosed a game-changing security flaw known as ‘ShadowLeak’ in OpenAI’s widely-used ChatGPT Deep Research agent. What makes this so important is the vulnerability’s severity, as it lets attackers extract sensitive data from OpenAI servers without needing anyone to click, open, or even view a message. Radware not only brought this to light but also gave OpenAI time to patch up, strengthening its reputation as a watchful and responsible force in the ever-evolving cybersecurity space.

This high-profile discovery comes after a year of mostly upward traction for Radware’s shares. The stock has climbed 27% over the past twelve months and is up nearly 23% year-to-date, reflecting investor optimism about its prospects. While there was a brief stumble during the past 3 months, momentum looks revitalized in the short run, buoyed by this recent headline and Radware’s steady revenue growth, with a 7% annual increase. Even as the ShadowLeak vulnerability steals headlines, it fits a pattern of Radware stepping ahead to address new AI-generated risks, suggesting lasting relevance in a competitive sector.

With this surge of attention around the ShadowLeak discovery, the question now is whether Radware’s share price still holds value for new buyers or if investors are already anticipating bigger growth ahead.

Price-to-Earnings of 82.7x: Is it justified?

Radware currently trades at a price-to-earnings (P/E) ratio of 82.7, which is significantly higher than both its peer average of 25.4 and the US Software industry average of 35.3. This elevated P/E ratio indicates that the market is factoring in strong future growth or seeing some unique advantage in Radware’s business compared to its competitors.

The P/E ratio is a key valuation multiple that measures how much investors are willing to pay for each dollar of a company’s earnings. In the technology and cybersecurity sector, P/E ratios can reflect high expectations for profitability and expansion, given the rapid pace of innovation. However, a much higher P/E compared to peers may signal that shares are expensive and could be vulnerable if growth expectations are not met.

With Radware’s P/E notably above industry norms, investors should consider whether this premium is justified by future earnings potential or if the price is ahead of fundamentals.

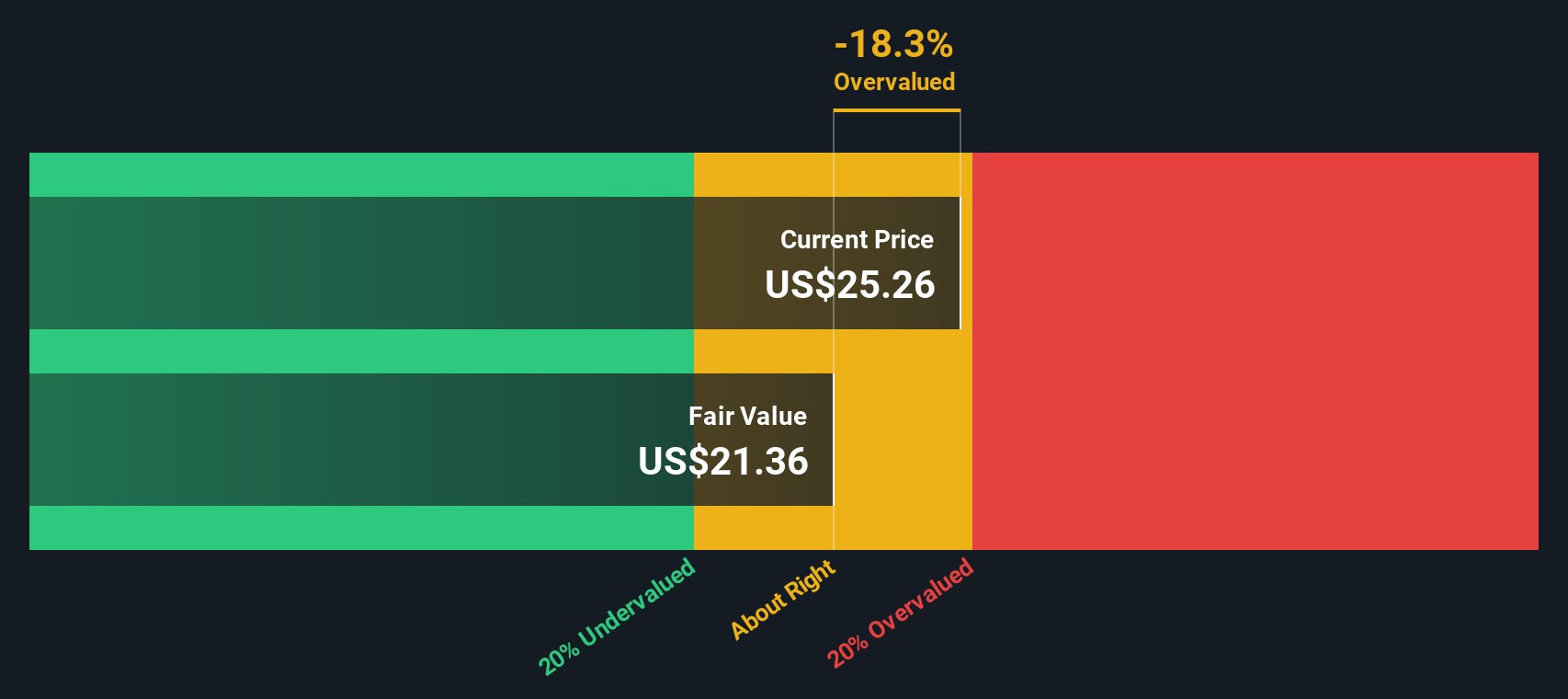

Result: Fair Value of $21.26 (OVERVALUED)

See our latest analysis for Radware.However, Radware’s high valuation could face pressure if revenue growth stalls or if new security breakthroughs by competitors change investor sentiment.

Find out about the key risks to this Radware narrative.Another View: SWS DCF Model Tells a Similar Story

Taking a different angle, our SWS DCF model also points to Radware trading above its underlying value. When both approaches agree, it triggers an obvious question: is the market too optimistic or seeing something others miss?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Radware Narrative

If you see things differently or want to look deeper into the numbers yourself, it’s easy to build your own view in just a few minutes. Do it your way

A great starting point for your Radware research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Why limit yourself to just one stock? The market offers a wide range of opportunities, and you can spot unique winners with Simply Wall Street’s powerful Screener. Don't let the next big move pass you by.

- Find potential bargains by searching for undervalued companies that may be trading for less than their true worth using our undervalued stocks based on cash flows.

- Follow the momentum in artificial intelligence trends by discovering top AI-driven innovators with our AI penny stocks.

- Discover consistent income opportunities by targeting companies with attractive yields via our dividend stocks with yields > 3%, helping you set up for steady returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.