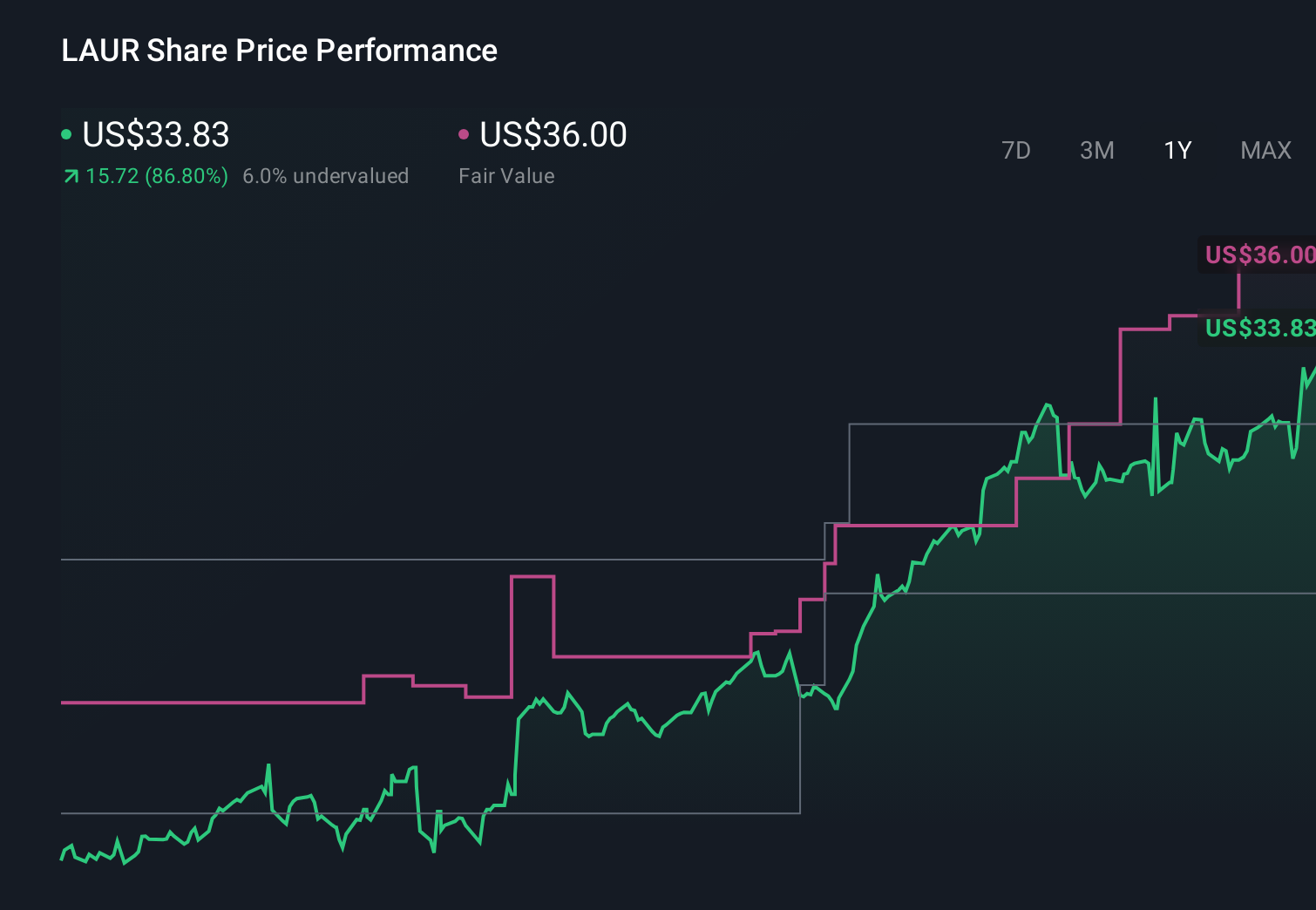

Raised EPS Guidance And Enrollment Growth Might Change The Case For Investing In Laureate Education (LAUR)

Laureate Education, Inc. LAUR | 0.00 |

- In late April 2026, Laureate Education, Inc. reported first‑quarter revenue of US$272.6 million, up from US$236.2 million a year earlier, alongside a wider net loss of US$21.6 million as growth investments and academic calendar timing weighed on profitability.

- Despite reporting a quarterly loss, Laureate highlighted 9% growth in new enrollments to 507,700 students, raised its full‑year adjusted EPS guidance, and completed US$105 million of share buybacks, underlining management’s confidence in the company’s enrollment‑led growth plan in Mexico and Peru.

- We’ll now examine how Laureate’s raised full‑year adjusted EPS guidance and robust enrollment gains might reshape its existing investment narrative.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Laureate Education Investment Narrative Recap

To own Laureate, you need to believe its Mexico and Peru focus, plus growing online programs, can translate strong enrollment into durable earnings, despite currency, regulatory, and competitive pressures. The key near term catalyst remains execution on 2026 guidance and enrollment targets; Q1’s revenue beat and 9% new enrollment growth support that, while the widened loss underlines the biggest current risk: heavy capital spending and fixed costs if enrollment or pricing soften.

Among recent developments, the most relevant here is Laureate’s decision to raise full year 2026 adjusted EPS guidance to US$2.00–US$2.08 per share while reaffirming revenue and adjusted EBITDA targets. That move, alongside US$105.0 million of Q1 share buybacks, reinforces the enrollment led growth story but also tightens the margin for error if academic calendar timing, cost inflation, or campus investments do not translate into stronger profitability later this year.

Yet the biggest concern investors should be aware of is how much capital Laureate is committing to new campuses just as...

Laureate Education's narrative projects $2.0 billion revenue and $343.9 million earnings by 2028. This requires 8.4% yearly revenue growth and an earnings increase of about $89.7 million from $254.2 million today.

Uncover how Laureate Education's forecasts yield a $39.58 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Before this Q1 update, the most optimistic analysts expected revenues near US$1.9 billion and earnings around US$331 million by 2028, so if you think digital expansion and working adult programs will overcome demographic and regulatory risks faster than consensus, your view will sit closer to that more bullish narrative, which could change meaningfully after these latest enrollment and margin trends.

Explore 3 other fair value estimates on Laureate Education - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Laureate Education research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Laureate Education research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Laureate Education's overall financial health at a glance.

No Opportunity In Laureate Education?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.