Raised Guidance and ARKA Integration Could Be A Game Changer For CACI International (CACI)

CACI International Inc Class A CACI | 0.00 |

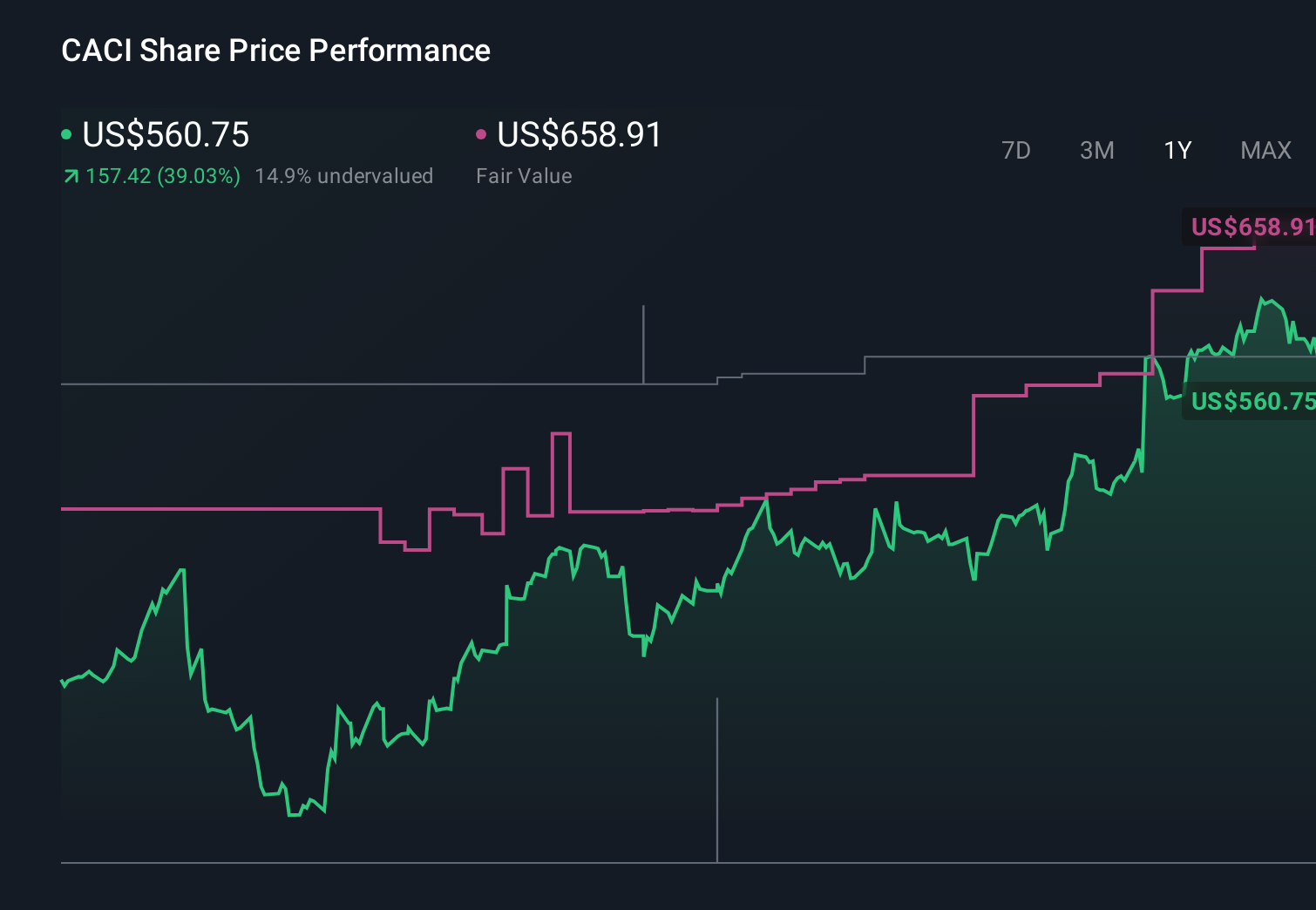

- CACI International’s recent third-quarter fiscal 2026 report showed higher sales and earnings versus a year ago, alongside updated full-year guidance calling for revenues of between US$9.50 billion and US$9.60 billion and net income of US$481 million to US$496 million.

- The company’s raised outlook, combined with new multi‑year defense contracts and the integration of ARKA’s space and AI capabilities, highlights how higher‑value technology work is increasingly shaping its business mix.

- Next, we’ll examine how CACI’s upgraded earnings guidance, underpinned by ARKA’s integration, may influence the company’s broader investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

CACI International Investment Narrative Recap

To own CACI International, you have to believe the company can keep shifting from lower‑margin services toward higher‑value technology work in areas like space, AI, and electronic warfare, while managing its heavy dependence on U.S. federal spending. The latest quarter’s higher sales and earnings, plus raised full‑year revenue guidance to US$9.50 billion–US$9.60 billion, support that thesis in the near term, but execution on ARKA integration and any disruption in defense budgets remain key swing factors.

Among the recent announcements, the five‑year, up to US$306 million task order to support the Defense Agencies Initiative’s Global Model is especially relevant. It underscores CACI’s role in long‑duration software modernization and financial systems work, which ties directly into its push toward stickier, tech‑heavy contracts. Wins like this can reinforce the upgraded earnings outlook, but they also highlight how concentrated the business remains in U.S. government programs and procurement cycles.

Yet, investors should be aware that if federal budgets tighten faster than expected, especially around defense technology programs, ...

CACI International’s narrative projects $11.9 billion revenue and $744.0 million earnings by 2029. This requires 10.0% yearly revenue growth and a $225.6 million earnings increase from $518.4 million today.

Uncover how CACI International's forecasts yield a $709.23 fair value, a 37% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts see more pressure ahead, even before this news, with 2029 revenue forecasts around US$11.8 billion and earnings of roughly US$728 million, reminding you that views on budget risk and automation can diverge sharply and that this new guidance could shift those expectations in very different directions.

Explore 3 other fair value estimates on CACI International - why the stock might be worth just $709.23!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your CACI International research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CACI International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CACI International's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.