Ralph Lauren (RL) Stock Looks Rich On Cash Flow But Strong On Earnings

Ralph Lauren Corporation Class A RL | 0.00 |

Ralph Lauren stock has delivered a very strong 5 year run, yet current valuation checks suggest the shares are trading at a premium to what its intrinsic value models and market multiples imply.

- Ralph Lauren has returned about 285.4% over the past 5 years, which puts recent gains front and center when judging whether the current price still offers an attractive entry point.

- Recent revenue momentum and brand investment can support optimistic expectations, but there are concerns about the stock screening as overvalued on a Discounted Cash Flow (DCF) view and market multiples, which leaves less room if growth or margins disappoint.

- On Simply Wall St’s broader valuation checks Ralph Lauren scores 1 out of 6, which leans expensive rather than like a clear bargain.

The issue now is whether Ralph Lauren’s current share price already reflects this strong multi year performance, or if the intrinsic value estimate suggests investors are paying too much for that track record.

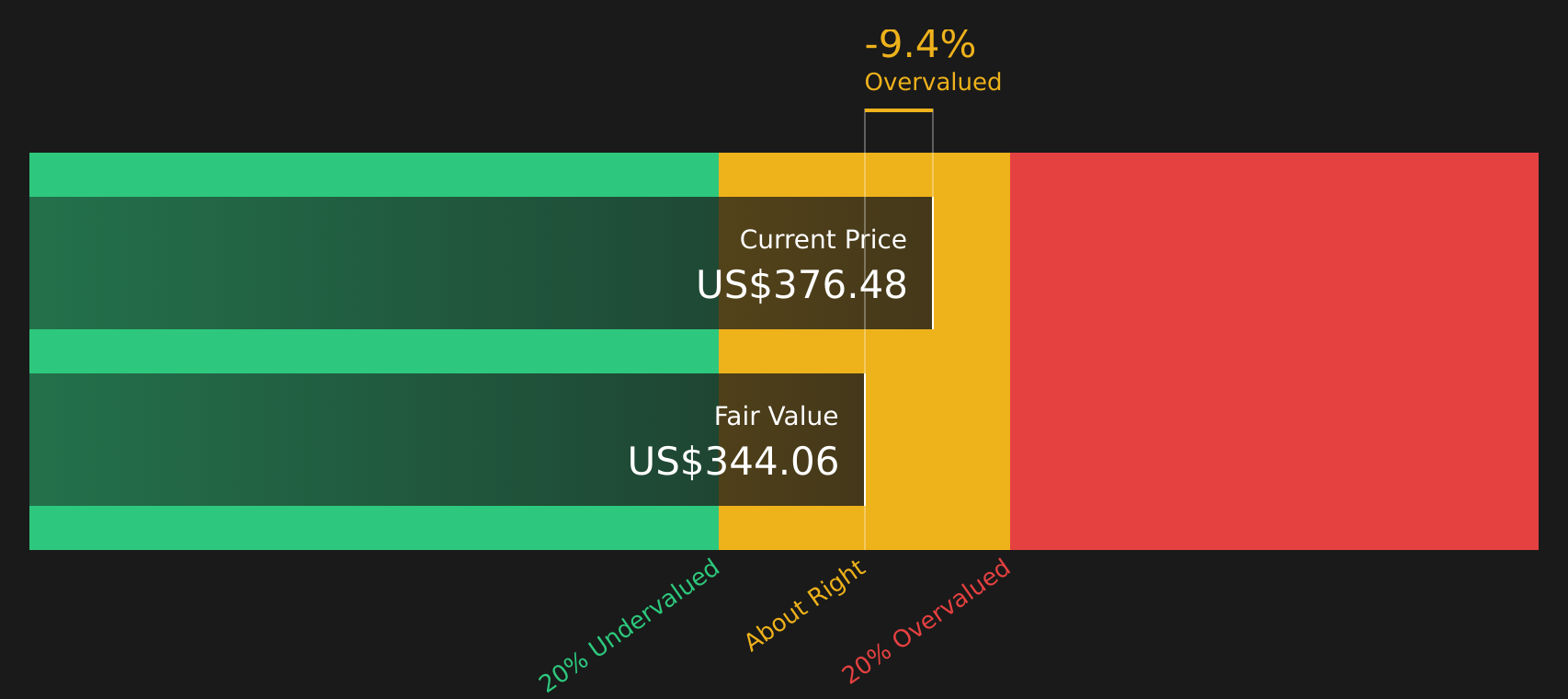

Has Ralph Lauren Run Too Far on Cash Flow?

The Discounted Cash Flow (DCF) method values Ralph Lauren by projecting future cash the business can return to shareholders and discounting it back to today. Ralph Lauren currently generates about $860.8 million in free cash flow over the latest twelve months.

On this basis, the 2 Stage Free Cash Flow to Equity model points to an estimated intrinsic value around $337 per share. That figure sits below the current market price and implies the stock screens as about 19.1% overvalued. The recent milestone of passing $8b in annual revenue may help explain why the share price trades ahead of this cash flow based estimate, with reported execution already reflected in what investors are willing to pay today.

Put together, this DCF analysis indicates that Ralph Lauren stock appears overvalued relative to its estimated intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests Ralph Lauren may be overvalued by 19.1%. Discover 43 high quality undervalued stocks or create your own screener to find better value opportunities.

Has Ralph Lauren Run Too Far on Earnings?

P/E is a useful lens for Ralph Lauren because earnings are a key focus for luxury investors comparing brands. Ralph Lauren currently trades on a P/E of about 25.4x, compared with an industry average of roughly 22.1x and a broader peer group around 28.6x, so the stock sits at a premium to the wider luxury sector but not at the very top of its peer range.

Based on Simply Wall St’s fair P/E estimate of about 22.3x, which reflects Ralph Lauren’s earnings profile, size and risk characteristics, the current 25.4x is higher than the level implied by those fundamentals. That gap suggests the recent enthusiasm around the company’s execution and brand strength is already well represented in the earnings multiple investors are paying.

Overall, Ralph Lauren stock screens as overvalued on the P/E multiple relative to the level its earnings fundamentals would typically justify.

The Ralph Lauren Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Ralph Lauren valuation puzzle leaves off by spelling out which combinations of future growth, margins and earnings would need to occur for the stock to be worth materially more or less than today’s price. These narratives are available on the company’s Community page. Each narrative ties a fair value estimate to a particular set of potential catalysts and risks, so you can track over time which storyline looks closest to reality.

Community views on Ralph Lauren sit far apart, with one camp focused on brand and margin strength and the other on competition and valuation risk.

Bull case: roughly fairly valued

"Premium brand positioning and reduced reliance on discounting continue to increase average unit retail (AUR) by 14% in the quarter, illustrating strengthened pricing power and value perception among consumers who desire quality and authenticity..."

Bear case: 27% overvalued

"The ongoing rise of digital-native and direct-to-consumer brands is intensifying competition and diminishing traditional brand loyalty, which threatens Ralph Lauren's ability to sustain revenue growth and limits pricing power as younger consumers increasingly gravitate towards newer labels with stronger online engagement..."

Do you think there's more to the story for Ralph Lauren? Head over to our Community to see what others are saying!

The Bottom Line

For Ralph Lauren, both the Discounted Cash Flow (DCF) intrinsic value estimate and the P/E multiple point to the stock screening as overvalued, with the DCF implying the current price sits meaningfully above its cash flow based fair value. That does not rule out further gains; however, it does mean the margin for error on growth and profitability looks thinner than it did in the past. From here, the key question is whether Ralph Lauren can sustain the brand strength and earnings profile that bulls expect, or whether any wobble in revenue or margins forces a rethink of how much you are willing to pay for the stock.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.