RB Global (RBA) Valuation Check As Fresh Buy Ratings Draw Investor Attention

RB Global, Inc. RBA | 0.00 |

Recent Buy ratings from Barclays, Bank of America Securities and other firms have pushed RB Global (RBA) into focus, as investors weigh this upbeat analyst sentiment against mixed views on the stock’s current valuation.

RB Global’s share price has edged higher in recent months, with a 90 day share price return of 3.86% and a 5 year total shareholder return of 96.77%. This suggests momentum has been building alongside the recent bullish analyst commentary and debate over whether the current valuation is stretched or still attractive.

If this mix of analyst enthusiasm and long term gains has your attention, it could be a good moment to broaden your watchlist with 20 top founder-led companies

So with analysts flagging upside to around US$127 and some models suggesting the stock trades close to or above estimated fair value, is RB Global quietly undervalued here, or is the market already pricing in its future growth?

Most Popular Narrative: 14.5% Undervalued

RB Global's most followed valuation narrative pegs fair value at about $124.20 per share, compared with the last close of $106.19. This puts a spotlight on what might be baked into those assumptions.

Expansion of the international buyer base and new alliance partnerships, along with ongoing growth in e-commerce marketplace activities, are expected to drive higher transaction volumes and revenue as more asset sales and auctions move online.

Joint ventures and acquisitions (e.g., LKQ in the U.K., J.M. Wood in the U.S., and new operations in Australia) are building a larger global footprint and improving cross-selling opportunities, supporting long-term revenue and margin growth.

Curious what kind of earnings trajectory and margin profile would need to underpin a fair value above $120, and how rich a future P/E that implies? The full narrative spells out the revenue build, margin lift and valuation multiple that have to line up for this price tag to make sense.

Result: Fair Value of $124.20 (UNDERVALUED)

However, this upside story could be knocked off course if macro pressures keep transaction volumes subdued or if integration of recent acquisitions drags on margins.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Angle: Multiples Paint a Tougher Picture

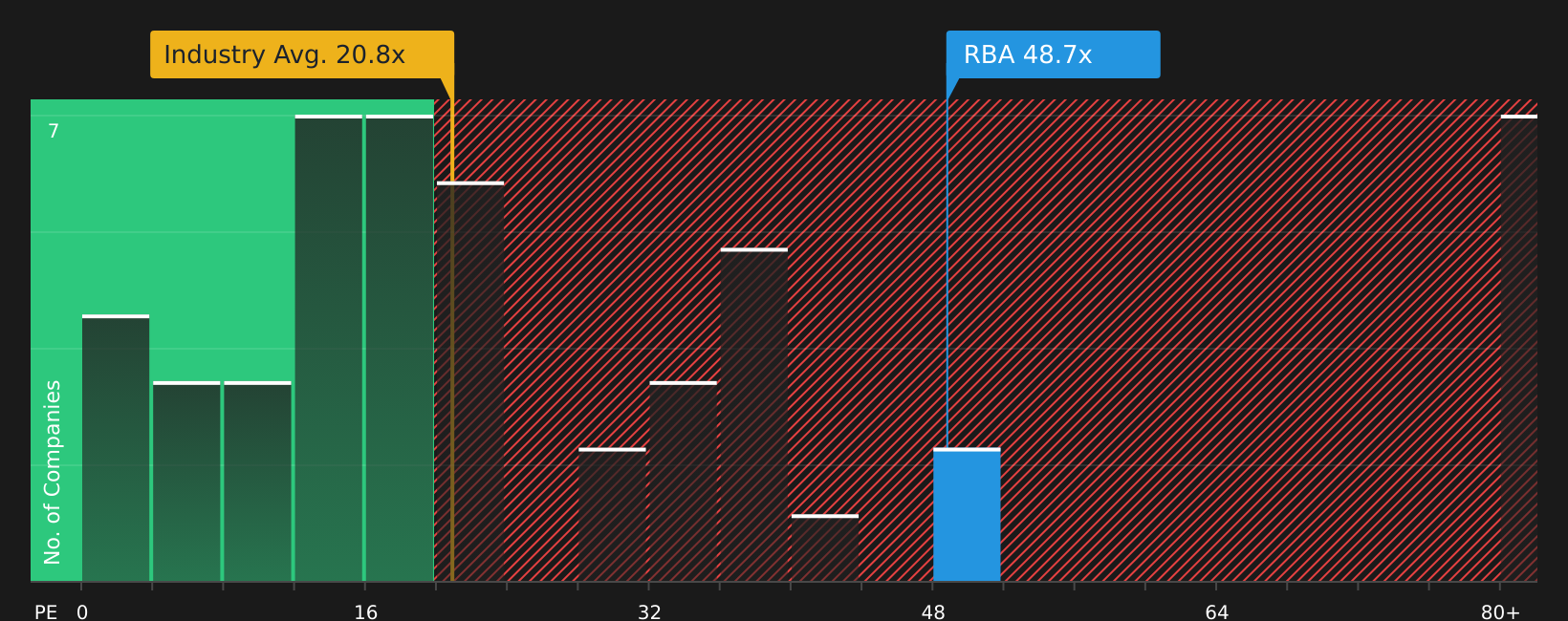

That 14.5% undervaluation story sits awkwardly beside RB Global’s current P/E of 49x, versus 20.8x for the US Commercial Services industry, 32.7x for peers, and a fair ratio of 26.6x. If the market leans back toward that fair ratio, how comfortable are you with the valuation risk?

Next Steps

With sentiment divided between upside potential and valuation risk, this is a good moment to review the numbers yourself and act on your own judgment by checking the full breakdown of 4 key rewards

Looking for more investment ideas?

If RB Global has sharpened your focus on valuation and risks, do not stop here. Broaden your opportunity set with a few targeted stock ideas tailored to different goals.

- Target potential mispricing by scanning 46 high quality undervalued stocks that pair solid business fundamentals with valuations that may still look reasonable on key metrics.

- Strengthen portfolio resilience by reviewing 63 resilient stocks with low risk scores that score well on risk factors and may help balance more aggressive positions.

- Spot tomorrow’s potential standouts early by checking the screener containing 21 high quality undiscovered gems before the wider market pays attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.