RBC Bearings Leans On Long Cycle Aerospace And Defense Growth

RBC Bearings Incorporated RBC | 571.61 | -2.62% |

- Wasatch Global Investors recently highlighted RBC Bearings (NYSE:RBC) as a core holding, citing continued strong execution and a positive outlook.

- Company management pointed to robust aerospace and defense demand, with strength from submarine, missile, and aircraft programs.

- RBC Bearings also reported an increased share of business with Airbus, indicating deeper involvement in commercial aerospace platforms.

RBC Bearings, a supplier of engineered bearings and components, sits at the crossroads of commercial and defense aerospace programs. The latest commentary links the business directly to long-cycle platforms such as submarines, missile systems, and aircraft, areas that often follow program spending rather than short term economic swings. For investors tracking NYSE:RBC, this context helps clarify where demand is coming from and which end markets are most influential.

The increased Airbus content and missile program exposure provide a clearer picture of how the company is positioned across both commercial and defense channels. For readers, the key takeaway is not just that demand exists, but which specific programs and customers are tied to it, and how that mix could shape the company’s risk profile and revenue sources over time.

Stay updated on the most important news stories for RBC Bearings by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on RBC Bearings.

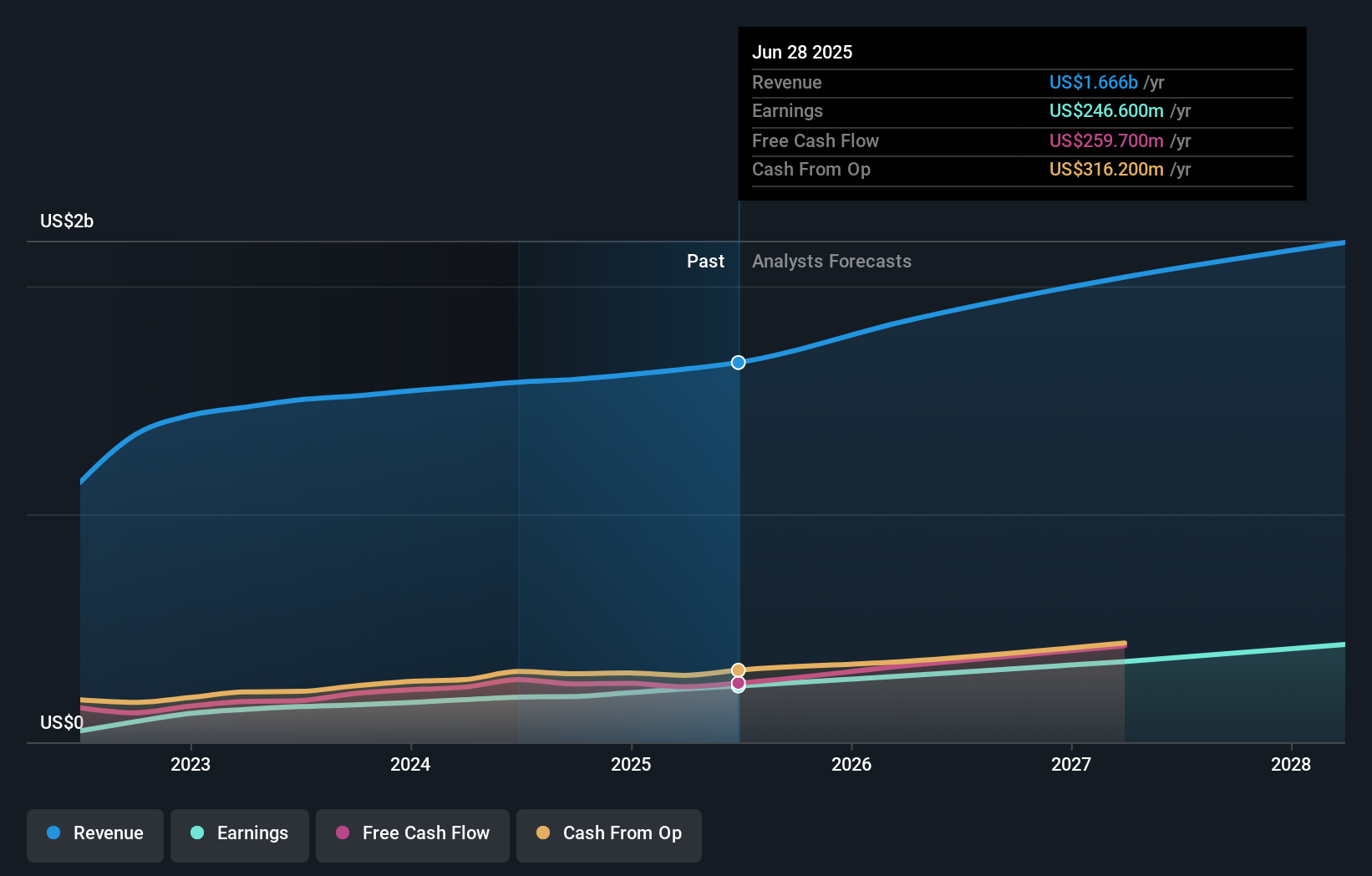

For RBC Bearings, the combination of investor endorsement and management commentary gives you a clearer read on execution rather than just sentiment. Recent results show quarterly sales of US$461.6 million and net income of US$67.4 million, alongside guidance for fourth quarter fiscal 2026 net sales of US$495.0 million to US$505.0 million. Management is tying that outlook to specific long-cycle programs in submarines, missiles, and aircraft, plus higher content on Airbus platforms. That points to growth driven more by program wins and content per platform than by short term volume swings, which can matter if you are comparing RBC to broader industrial suppliers.

How This Fits Into The RBC Bearings Narrative

- The stronger aerospace and defense demand, together with higher Airbus content, aligns with the view that long term contracts, capacity investment, and acquisitions such as VACCO are supporting revenue and margin expansion in key segments.

- Heavier exposure to defense and a concentrated customer set could be a concern if program schedules change or major OEMs such as Airbus, Boeing, or GE adjust build rates or sourcing, which is already flagged as a risk.

- The latest emphasis on missile and submarine programs, and the integration of VACCO into those areas, adds detail on product mix and application exposure that is not fully captured in higher level descriptions of advanced bearings and motion control solutions.

Knowing what a company is worth starts with understanding its story. Check out one of the top narratives in the Simply Wall St Community for RBC Bearings to help decide what it is worth to you.

The Risks and Rewards Investors Should Consider

- ⚠️ Reliance on a relatively small group of large aerospace and defense customers, including Airbus and other major OEMs, means program delays or design changes could have an outsized impact on revenue and capacity utilization.

- ⚠️ Ongoing acquisition integration, including VACCO, and capacity expansion to serve defense and space programs may create execution risk if supply chains tighten or program volumes do not materialize as planned.

- 🎁 Earnings and revenue outcomes identified by analysts, together with the company’s recent sales and net income performance, indicate that the business is currently converting demand into higher profits.

- 🎁 Exposure to long-cycle submarine, missile, and aircraft programs, alongside commercial platforms like those at Airbus, can provide multi year visibility that some peers in industrial bearings or motion components may not have.

What To Watch Going Forward

From here, you may want to watch whether RBC Bearings converts its fourth quarter fiscal 2026 sales guidance into actual results in the US$495.0 million to US$505.0 million range, and how margins track as defense and commercial aerospace mix shifts. Management commentary on Airbus build rates, missile and submarine order trends, and VACCO integration will be important for assessing how durable current demand is compared with shorter term strength. It may also be useful to compare execution against other aerospace focused suppliers, such as Timken or Parker Hannifin, to see how RBC’s end market exposure and contract activity compare over time.

To stay informed on how the latest news affects the investment narrative for RBC Bearings, visit the community page for RBC Bearings to follow the top community narratives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.