RBC Bearings (RBC) Valuation Check As Upward Earnings Revisions Support Aerospace And Industrial Momentum

RBC Bearings Incorporated RBC | 548.11 | -0.70% |

RBC Bearings (RBC) has drawn fresh investor attention after earnings estimates were revised upward, along with a strong Zacks Rank that points to improving confidence in its Aerospace/Defense and Industrial operations.

The recent upward revisions to earnings estimates sit alongside a share price of $488.31, with a 90-day share price return of 27.17% and a 1-year total shareholder return of 63.88%. This suggests momentum has been building as investors reassess both growth potential in Aerospace/Defense and Industrial and the balance of risks.

If this kind of upward momentum has your attention, it could be a good moment to see which other aerospace and defense names are also gaining traction through aerospace and defense stocks.

With shares at $488.31 after a 63.88% 1-year total return and the stock trading only about 5% below the average analyst price target, investors may wonder whether there is still upside potential or whether the market is already pricing in future growth.

Most Popular Narrative: 2.5% Undervalued

RBC Bearings' most followed narrative pegs fair value at about US$500.83 per share, slightly above the last close of US$488.31, which keeps expectations finely balanced.

Ongoing capacity expansions and selective CapEx in key growth businesses (notably aerospace and defense) are aligned with rising OEM build rates and new long-term contracts, positioning the company to capture increased content per aircraft/engine and strengthen gross margins and earnings as OEM production ramps up.

Want to understand why earnings and margins sit at the heart of this valuation? The narrative leans heavily on rich revenue assumptions and a premium future P/E that is higher than many peers. Curious which specific growth and profitability hurdles those projections need to clear to back up that fair value? The full story connects those moving parts in detail.

Result: Fair Value of $500.83 (UNDERVALUED)

However, this story can change quickly if supply chain issues around specialty alloys disrupt deliveries, or if key aerospace and defense customers adjust production plans or sourcing.

Another Angle on Valuation: Premium P/E and Fair Ratio

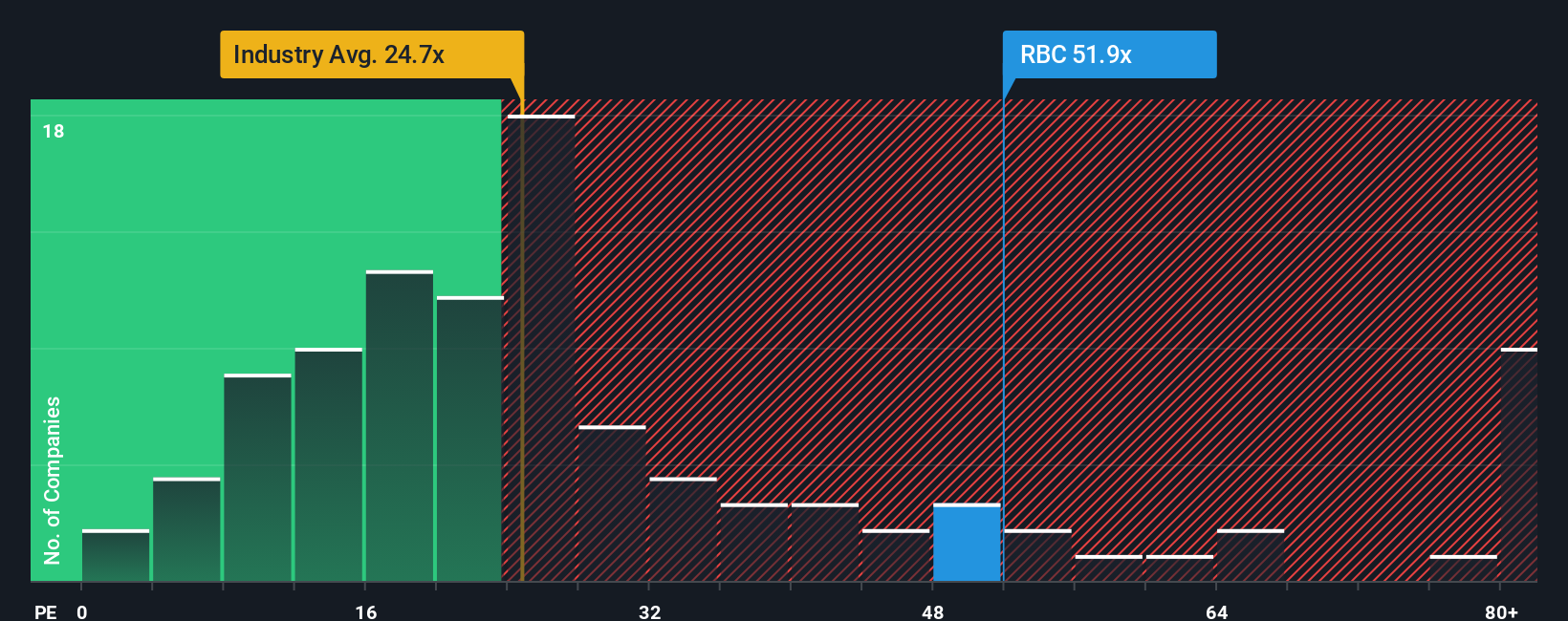

So far, the popular narrative leans on rich growth and margin assumptions to frame RBC Bearings as about 2.5% undervalued. If you step away from that story and just look at the P/E, the picture is very different.

On current numbers, RBC trades on a P/E of 59.6x. That is well above the US Machinery industry average of 26.3x and also higher than the peer group average of 29.6x. Our fair ratio for RBC sits at 30.2x, which is much closer to those benchmarks.

In practical terms, that gap means you are paying roughly double the fair ratio today. As a result, a lot of good news is already reflected in the price and the margin for error is tighter than the narrative alone suggests. The key question is whether earnings quality and growth can keep that premium intact, or if the multiple could move back toward the fair ratio over time.

Build Your Own RBC Bearings Narrative

If you see the numbers differently or want to stress test the assumptions with your own inputs, you can build a custom view in minutes by starting with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding RBC Bearings.

Looking for more investment ideas?

If RBC Bearings has you thinking more broadly about your portfolio, this is a great moment to scan other opportunities that match different goals and risk levels.

- Target potential value opportunities by checking out these 879 undervalued stocks based on cash flows built on discounted cash flow estimates.

- Spot emerging themes in technology by reviewing these 26 AI penny stocks that are tied to artificial intelligence trends.

- Strengthen your focus on income by scanning these 12 dividend stocks with yields > 3% that may suit a yield conscious approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.