Realty Income (O) Valuation Check After GIC Partnership Notes Offering Strong Q3 And Dividend Growth

Realty Income Corporation O | 63.96 | +0.24% |

Recent updates around Realty Income (O) have centered on several concrete moves, including a real estate partnership with Singapore’s GIC, an $862.5 million convertible notes offering, solid Q3 results, and ongoing monthly dividend increases.

The recent partnership with GIC, the $862.5m convertible notes issuance and Realty Income’s Q3 update have arrived alongside firming share price momentum, with a 30 day share price return of 8.87% and a 1 year total shareholder return of 27.42% suggesting improving sentiment over both the short and longer term.

If this income story has you thinking about where else capital could work for you, it might be worth scanning our 25 power grid technology and infrastructure stocks as a fresh set of infrastructure ideas to research next.

With a recent 52 week high, a 5.1% yield and a model that has raised dividends for 113 straight quarters, is Realty Income still trading at a discount, or are investors already paying up for future growth?

Most Popular Narrative: 2.1% Overvalued

Realty Income last closed at $65.66, a touch above the most followed fair value estimate of $64.31, which is built on detailed growth and margin assumptions.

Embedded rental escalators, very long lease durations (~15 years on recent acquisitions), and data driven asset management provide high visibility into predictable, compounding rental income for the long term, which should support continued stable net operating income and consistent dividend growth.

Curious how steady rent escalators, longer leases, and richer margins are stitched together into that fair value? The narrative leans on specific revenue growth, earnings expansion, and a premium future earnings multiple. Want to see which assumptions really carry the weight in that $64.31 figure?

Result: Fair Value of $64.31 (OVERVALUED)

However, that fair value story can be knocked off course if rising competition for net lease assets squeezes acquisition spreads, or if heavier European exposure introduces more earnings volatility.

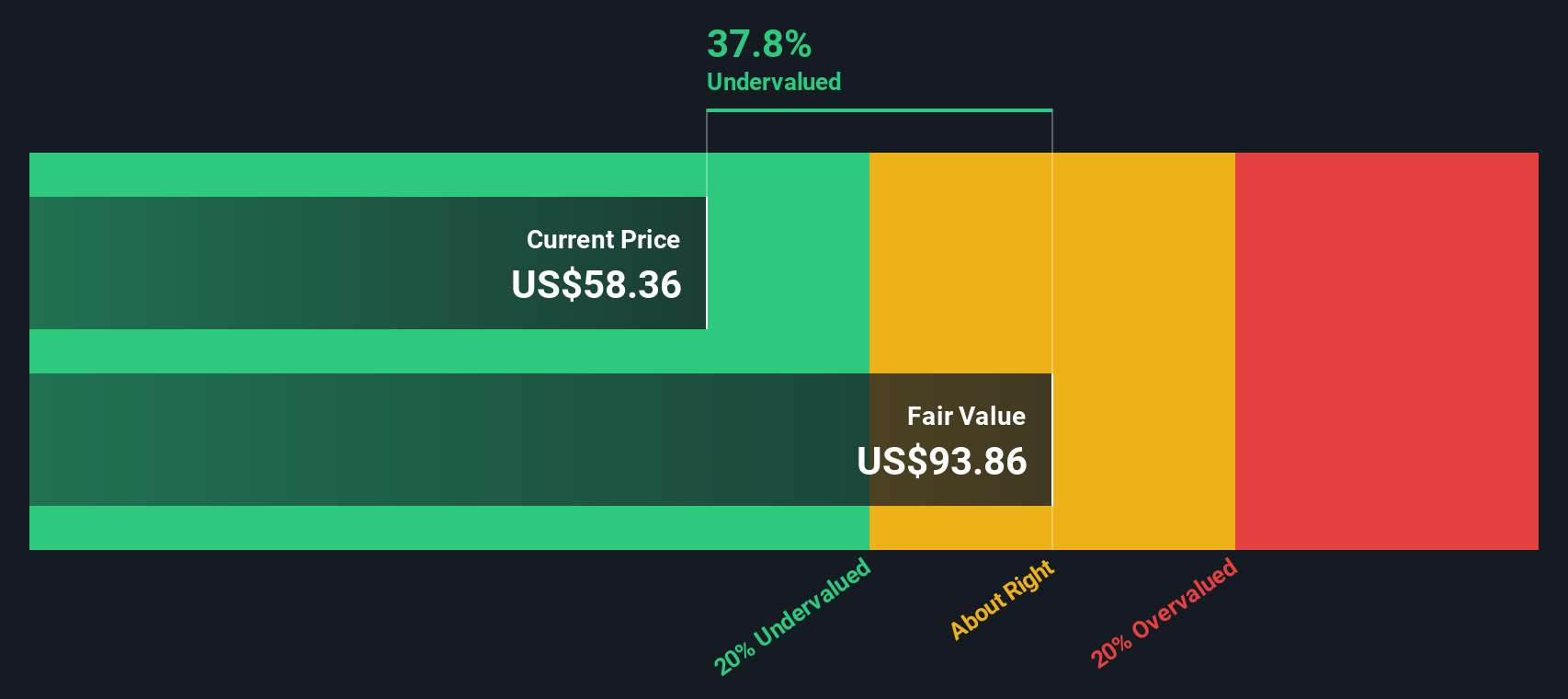

Another View: Big Discount On Cash Flows

While the most followed fair value estimate of $64.31 suggests Realty Income is around 2.1% overvalued, our DCF model points in the opposite direction. On that view, the shares trade about 34.7% below an estimated fair value of $100.61, which is a wide gap for income focused real estate.

If both models are working off reasonable assumptions, the question for you is simple: which set of expectations about growth, margins, and required return feels more realistic?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Realty Income for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Realty Income Narrative

If you are not fully on board with these assumptions, or you simply prefer to test the numbers yourself, you can build a custom view in minutes, then Do it your way

A great starting point for your Realty Income research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one income name, you could miss other opportunities that better match your goals, risk comfort, and timeline, so keep widening your lens.

- Target stronger payouts with resilient cash generators by checking out our 13 dividend fortresses that might suit investors who want income to feel more predictable.

- Hunt for potential mispricings by scanning the screener containing 23 high quality undiscovered gems and give yourself a shot at ideas the broader market may not be watching yet.

- Prioritize capital preservation first by reviewing our 85 resilient stocks with low risk scores which focuses on companies that score more defensively on a range of risk factors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.